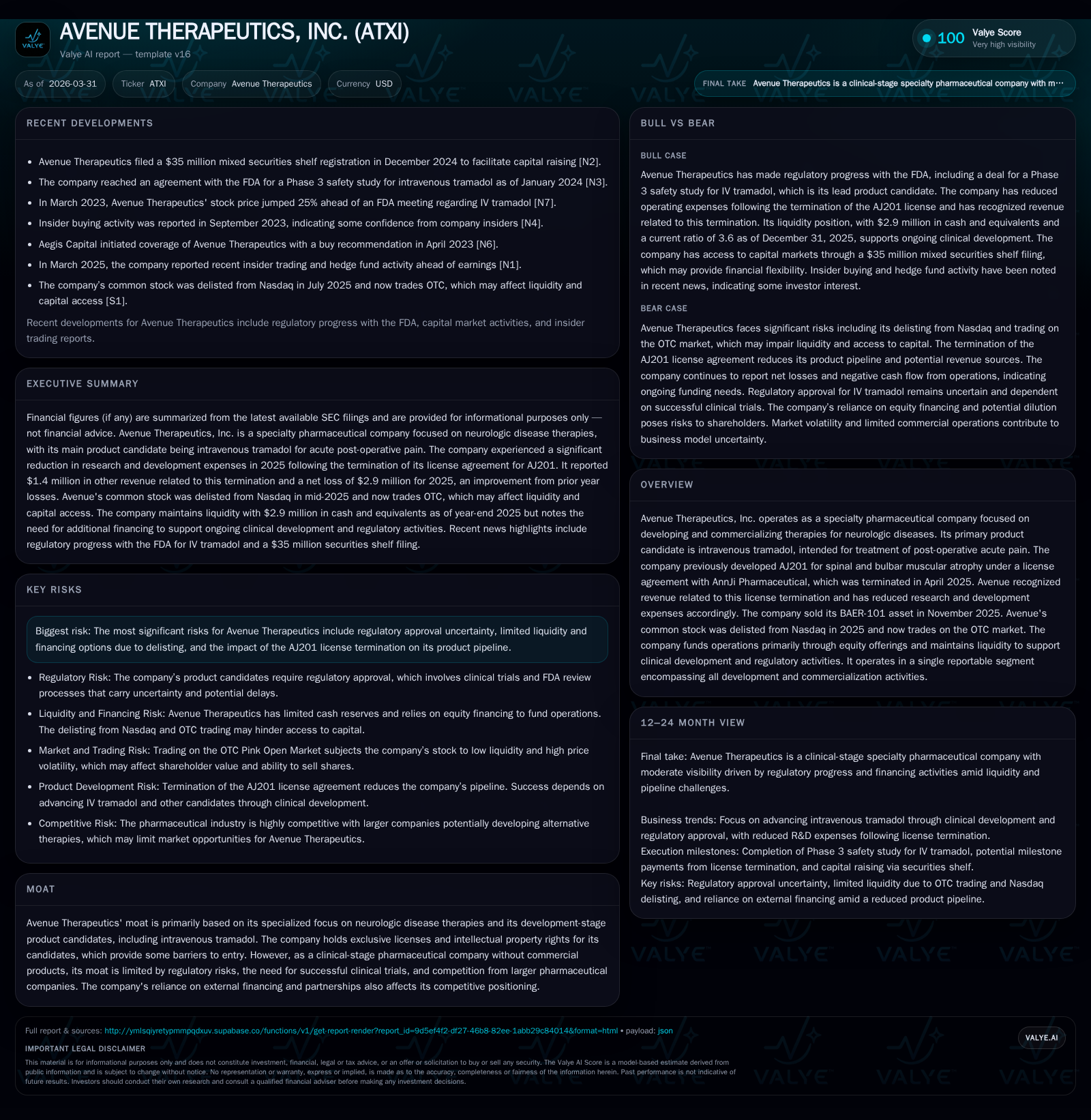

Avenue Therapeutics’ Financing Constraints and Growth Path in Neurologic Therapies

Post-delisting, Avenue Therapeutics refocuses its pipeline on intravenous tramadol while managing liquidity challenges amid halted assets.

Avenue Therapeutics’ transition in 2025 involved significant portfolio pruning with the termination of the AJ201 license and sale of BAER-101, leading to improved operating income primarily due to reduced R&D. The company’s strategic pivot centers on intravenous tramadol as its lead clinical candidate for acute post-operative pain. However, delisting from Nasdaq has constrained traditional financing avenues, forcing dependence on OTC markets and equity sales to sustain operations. Future growth hinges on clinical progress with tramadol and the recently licensed ATX-04 asset, while liquidity risks and regulatory uncertainties remain material hurdles.

From License Terminations to Asset Sales: Historical Growth Trajectory

Avenue Therapeutics faced pivotal shifts throughout 2025 that reshaped its financial profile and operational focus. Most notably, in April 2025, the company terminated its license agreement with AnnJi Pharmaceutical for AJ201, a candidate targeting spinal and bulbar muscular atrophy. The termination came following AnnJi's assertion of contractual rights leading Avenue to relinquish all related rights to AJ201 while receiving a modest revenue credit associated with this unwind [S16][F1]. Later that year, in November 2025, Avenue divested its BAER-101 asset, further consolidating its portfolio .

These structural moves significantly influenced the financials. Revenue for FY2025 was reported at approximately $1.4 million exclusively related to payments from the AJ201 license termination—a revenue line absent in prior years [F1]. Operating losses narrowed sharply by nearly 73% YoY from $11.3 million in 2024 to $3.1 million in 2025 due principally to reduced research and development (R&D) expenses following AJ201’s exit and cessation of BAER-101 activities [F1][S22]. Such license milestone revenues are typical one-time gains accounted per pharma industry practices when contract terminations occur [S1].

Reduced R&D spend—from $6.6 million in 2024 down to about $1 million in 2025—reflects this shift away from costly clinical development programs for discontinued assets [F1][S22]. Although net losses improved by over 75% YoY to about $2.9 million, the company remains unprofitable with accumulated deficits exceeding $105 million at YE25 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -3 | -2 | -3 | |

| 2024 | -9 | -11 | ||

| 2023 | -9 | -15 | ||

| 2022 | -4 | -8 | -8 | +4.8% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -158.8 |

| 2024 | |

| 2023 | |

| 2022 | -91.0 |

Source: SEC companyfacts cache [F1].

Operating income improved largely due to reduced R&D expense from license termination and asset sales.

Recentered Product Focus: The Promise of Intravenous Tramadol

Following portfolio rationalization, Avenue’s strategic focus has re-centered tightly on intravenous tramadol (IV tramadol), its lead clinical-stage candidate designed for management of acute post-operative pain [S3]. This candidate represents a specialty therapeutic within neurologic disease pain management—a domain necessitating careful balancing between efficacy, safety profiles, and abuse potential.

Additionally, in February 2026, Avenue secured an exclusive worldwide license from Duke University for ATX-04 (clenbuterol), aimed at treating lysosomal storage diseases—a rare disease indication distinct from IV tramadol’s acute pain market but aligned with neurology-related disorders [S3]. This licensing deal underscores cautious pipeline diversification while resources remain focused primarily on tramadol advancement.

This kind of tight pipeline focus is emblematic of specialty pharmaceutical companies operating under constrained resources—it minimizes dilution of R&D efforts while positioning near-term commercialization prospects around a well-defined clinical candidate.

Navigating Capital Constraints Post-Delisting: Financing Operations without Nasdaq Access

Capital structure considerations have grown more complex since Avenue’s common stock was suspended from Nasdaq trading on March 17, 2025 and formally delisted by July 18, transitioning the security onto the OTC Pink market under ticker ATXI [S10]. This delisting event materially restricts institutional investor access and eliminates eligibility for shelf registration use under Form S-3; concurrently disabling access to the At-The-Market (ATM) offerings which had been a primary liquidity conduit [S4][S7].

At December 31, 2025 cash and equivalents stood at approximately $2.9 million—slightly higher than the $2.6 million balance at year-end 2024—but net cash used in operations improved dramatically by almost 80% YoY given lower spend levels [F1][S20]. The company generated about $2.1 million gross proceeds before commissions through ATM share sales before losing access post-delisting; however, subsequent equity raises now face diminished market depth due to OTC illiquidity [S7][S25].

Current liabilities totaled just under $1.1 million against current assets approximating $3.96 million as of late 2025 evidencing a respectable current ratio near 3.6x [F1][S6], but runway extension beyond twelve months is uncertain absent additional financing or partnerships [S4]. The thinly traded OTC Pink venue heightens volatility risk for float shares while limiting efficient capital raising capacity—a critical challenge for small-cap clinical-stage biopharmaceuticals reliant on external funding.

Clinical Development Milestones and Regulatory Hurdles Ahead

Clinical progression for IV tramadol constitutes the core growth vector amidst tightened resource allocation [S3]. While explicit forthcoming milestones such as FDA NDA filing dates have not been publicly disclosed as of Q1 2026, industry-standard expectations include successful completion of pivotal safety and efficacy studies—likely phase III—to underpin registration submissions.

Given FDA’s stringent scrutiny over opioid class drugs including abuse liability assessments coupled with evolving regulatory paradigms on pain therapeutics, regulatory risk remains non-trivial [S27][S29]. Additionally, the newly licensed ATX-04 asset introduces further developmental demands requiring time and capital commitment prior to viable commercialization pathways.

Investors should monitor updates relating to IND filings, clinical trial commencements or completions, FDA correspondence outcomes, and potential partnerships or collaborations that could underwrite expensive late-stage studies.

Capital Allocation, Shareholder Returns, and Cash Flow Dynamics

Avenue Therapeutics currently exhibits no dividend payments or share repurchase programs reflecting typical developmental-stage biotech capital discipline prioritizing cash conservation for ongoing R&D activities [F1][S10][S17]. Share-based compensation expense continues at modest levels (~$0.7 million in FY25) contributing non-cash charges underpinning net loss figures.

Equity financing has served as the principal source of operational funding; issuance volumes increased shares outstanding from roughly 2.1 million common shares at end-2024 to over 3.18 million by end-2025 primarily through ATM sales conducted pre-delisting [F1][S7]. Despite these efforts net income remained negative with an effective ROE hovering near negative 159%, emblematic of deep accumulated losses offsetting residual equity [F1].

Improved operating cash flow (-$1.8 million in FY25 vs -$9.0 million in FY24) reflects sharp cost rationalization though does not yet indicate transition towards positive free cash flow generation given nascent commercial activity absence [F1][S20]. Careful stewardship will be required to stretch existing capital buffers during continued clinical investments.

Key Risks: Liquidity, Regulatory Uncertainty, and Market Volatility

Liquidity constraints present among the most salient risks stemming from delisting-driven loss of broad financing channels alongside thin OTC trading volumes that amplify price swings unrelated to fundamental business developments—potentially impairing shareholder value realization opportunities [S1]. Equity raises face elevated dilution risk or unattractive terms without institutional participation.

Regulatory approvals for IV tramadol carry inherent uncertainty given FDA's evolving posture toward opioid analgesics compounded by requirements for comprehensive safety data including abuse deterrence features [S27][S29]. Failure or delay could adversely impact timelines and increase financing dependency.

Furthermore, legacy impacts from AJ201 license termination remove an alternate product development avenue reducing pipeline breadth; concurrent reliance on minimal assets elevates operational leverage vulnerability during extended development cycles.

Collectively these factors underscore significant risk-reward challenges typical among specialty pharma firms heavily dependent on single product candidates amid adverse capital market conditions.

This analysis synthesizes available public disclosures through early Q2 2026 emphasizing disclosed financial trends, licensing arrangements, regulatory backdrop insights, and capital structure developments relevant for stakeholders monitoring Avenue Therapeutics' evolution within neurologic disease therapeutics space.

Disclaimer: This report is prepared solely for informational purposes based on public filings without any investment recommendation or forecast promise regarding future security performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments