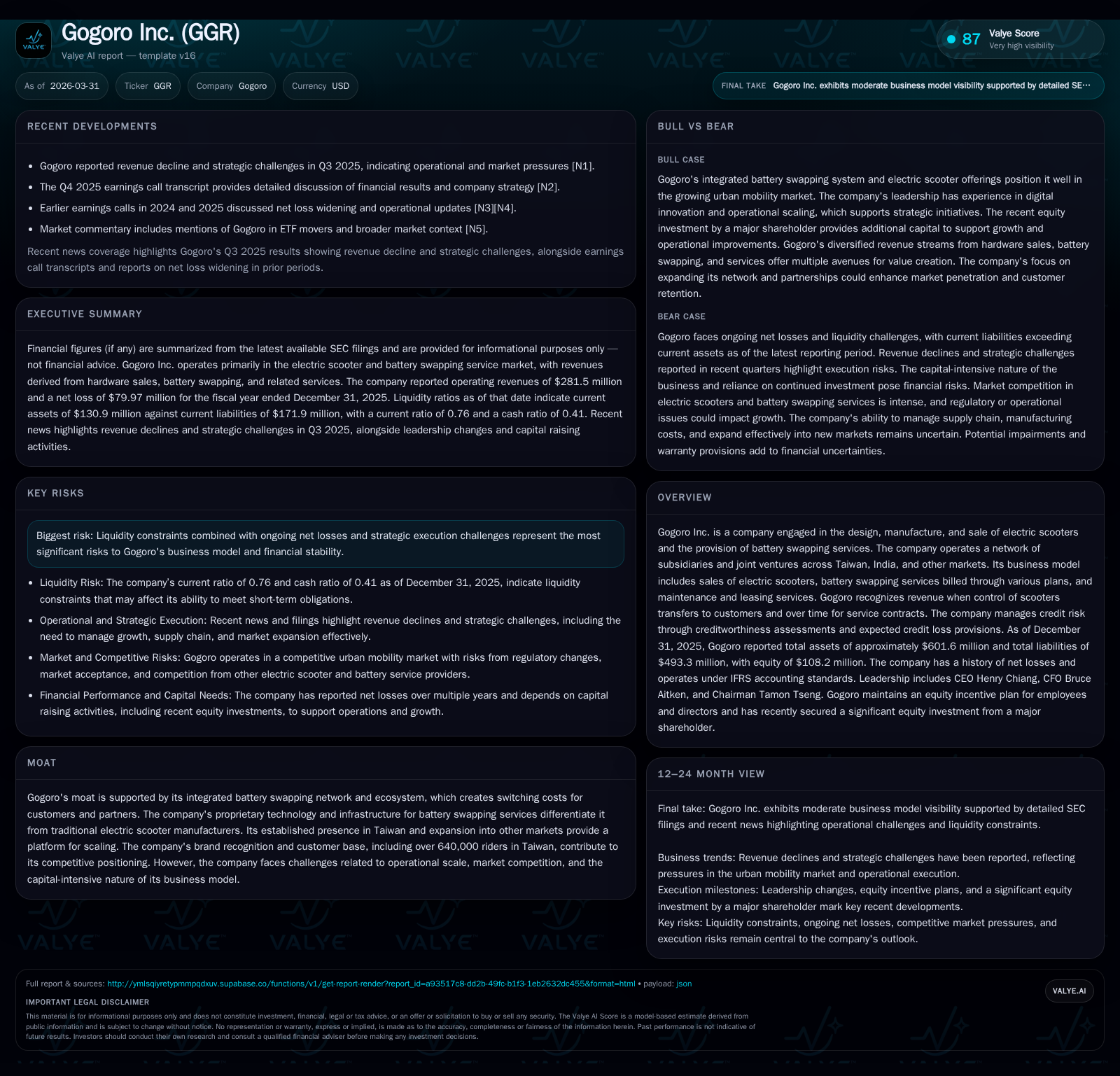

Gogoro Inc.’s Financial Turbulence and Battery Swapping Proposition

Gogoro’s innovative battery swapping network underpins its market moat amid persistent financial pressures and strategic capital maneuvers.

Gogoro Inc. operates a pioneering battery swapping ecosystem supporting electric scooters across Taiwan and newer markets, creating meaningful switching costs and network effects. Despite this, the company has faced continuous net losses from 2022 to 2025, with a narrowing loss in the most recent year but persistent liquidity challenges. Gogoro’s balance sheet reveals substantial liabilities compared to equity, with ongoing capital raises including a recent $16.7 million equity infusion from its largest shareholder to bolster liquidity. Operational headwinds, supply chain irregularities, and competitive pressures contributed to revenue declines in 2025, yet growth opportunities remain across Asia with expanding joint ventures. Investors should closely monitor Gogoro’s execution on operational ramp-up, working capital management, and the effectiveness of its unique integrated battery swapping infrastructure.

From Growth to Pressure: Historical Financial Performance Review

Gogoro Inc. has continued to operate at a net loss over the past four fiscal years, reflecting the capital-intensive nature of its electric vehicle (EV) battery swapping business model and early-stage market penetration efforts. According to the latest audited financials ending December 31, 2025, net income recorded a loss of approximately $79.97 million, an improvement from the $122.75 million loss reported in FY2024, indicating some contraction in operating losses though still substantially negative [F1]. The equity base diminished notably alongside volatile profitability dynamics, falling from $298.97 million at the end of FY2022 to just $108.24 million by FY2025 as accumulated deficits have grown [F1]. This translates into an implied return on equity (ROE) for FY2025 of roughly -73.9%, underscoring persistent inefficiencies [F1].

Meanwhile, working capital metrics illustrate liquidity stresses with current assets at $130.9 million against current liabilities of $171.9 million for a current ratio of about 0.76—below the critical threshold of unity—highlighting challenges in cash cycle management as Gogoro scales operations [F1]. The following table summarizes key elements of Gogoro’s financial position over the last three years:

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | -80 | +34.9% |

| 2024 | -123 | -61.4% |

| 2023 | -76 | +23.1% |

| 2022 | -99 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -73.9 |

| 2024 | -69.5 |

| 2023 | -30.6 |

| 2022 | -33.1 |

Source: SEC companyfacts cache [F1].

*Detailed cash or current asset/liability figures prior to 2025 are not consistently reported.

This trajectory illustrates significant financial pressure amidst Gogoro's expansion phase.

Battery Swapping Ecosystem as a Moat: Competitive Edge and Market Reach

At the core of Gogoro’s market differentiation lies its proprietary battery swapping infrastructure—an integrated ecosystem coupling electric scooters with a network of rapid exchange stations supported by subscription-based service plans (). This unique architecture fosters substantial switching costs for customers by embedding them within recurring payment schemes tied to battery services rather than single hardware purchases alone.

In industry terms, Gogoro leverages both network effects—whereby increasing user adoption enhances utility of each station—and lock-in factors that deter competitor encroachment due to costly customer transitions away from established service points.

Compared to conventional EV scooter OEMs reliant solely on sales volume without ongoing service relationships, Gogoro’s model incentivizes continuous engagement through subscriptions akin to Software-as-a-Service (SaaS), effectively blending hardware sales with recurring revenue streams.

Geographically anchored primarily in Taiwan—with over 640,000 riders registered—the company expands abroad via subsidiaries and joint ventures extending access to emerging markets such as India (), seeking to replicate this moated asset base.

Revenue Decline Drivers and Operational Challenges Emerging in 2025

Despite structural innovations, Q3 2025 results illuminated strains as total revenues declined compared to prior periods driven partly by operational bottlenecks [N1]. Supply chain irregularities surfaced during calendar years '24-'25—including component sourcing disruptions linked to policy-driven domestic content mandates—dented margin compression and production continuity [S1][S9].

These disruptions led to recalls or adjustments on certain vehicle shipments involving imported parts disqualified under subsidy programs aimed at stimulating domestic manufacturing ([S1]). The residual impact reduced hardware sales volume growth while elevating warranty provisions.

Competition intensifies both locally and internationally as other EV mobility providers increase presence with varied business models lacking comparable proprietary swapping technology but leveraging aggressive pricing or partnerships ([N1],[S9]). This sets a challenging backdrop for revenue stabilization absent accelerated operational ramp.

Capital Structure and Liquidity: Navigating Debt and Funding Risks

Gogoro's balance sheet reveals leverage concentrated principally in bank loans totaling about $361 million as of December 31, 2025 (current + non-current), reflecting long-tenor syndicated facilities primarily arranged with Mega Bank along with various term loans dedicated to battery procurement and station buildout [S6][S15]. Interest rates range from low single digits (~2-3%) up to approximately 11% on lease liabilities [S6],[S15].

The company’s non-derivative financial liabilities mature mainly over medium-to-long terms (up to five years), but interim maturities create working capital gaps requiring active cash flow management [S5][S6]. Amended credit agreements executed March 2026 loosen financial covenants in response to operational realities while obligating related parties like director Yin Chung Yao to secure additional equity investment up to NT$2.5 billion (~$80 million USD equivalent) within calendar year-end [S4][S16], mitigating near-term refinancing risks.

Debt service coverage remains pressured by recurring operating losses while cash reserves declined from over $117 million in prior year-end down to roughly $70.6 million at December 31, 2025 ([F1],[S15]), indicating increasing reliance on financing activities.

Strategic Equity Infusion and Recent Investor Commitment

March 12, 2026 filings revealed a strategic $16.7 million new equity injection by Gold Sino—the company’s largest shareholder holding ~31% prior—acquiring over five million newly issued shares at a discount price aiming for increased ownership nearing half the total outstanding shares post-subscription ([S3],[S4],[S20]).

This infusion aligns directly with undertakings tied to credit facility amendments remodeling covenant terms as part of an overall recapitalization effort designed to stabilize liquidity while providing runway for operational initiatives including international expansion efforts ([S4],[S16]).

Such moves signal both investor confidence aligned with management vision and underscore urgent funding needs amid ongoing cash burn.

Growth Opportunities Across Regional Markets and Business Segments

Beyond Taiwan’s mature foothold, Gogoro seeks traction through alliances and joint ventures targeting markets such as India where two-wheel EV mobility experiences secular growth potential fueled by urbanization trends (,[N1],[S2]).

Its go-to-market strategy differentiates B2C direct sales of electric scooters supported by agent networks versus subscription-model monetization derived from battery swaps, leveraging technology licensing arrangements like "Powered by Gogoro Network" partnerships that scale reach without commensurate capex requirements (,[N1]).

Nonetheless, regulatory risk profiles vary considerably across these jurisdictions introducing legal compliance complexity especially around component sourcing rules noted earlier ([N1],[S9]). Competitive intensity from entrenched local players also constrains rapid market share gains.

Key Milestones Ahead: What Investors Should Watch in 2026

While explicit forward guidance remains muted with no detailed forecasts published ([N1],[S2]), several operational yardsticks will critically influence trajectory:

- Successful integration ramp of new JV markets including batch deployments in India,

- Stabilization or growth resumption in hardware sales combined with rising subscription revenue scale,

- Supply chain normalization mitigating margin erosion,

- Effective working capital management improving current ratio nearer parity,

- Execution risk reduction concerning litigation outcomes around supply chain irregularities,

- Capital structure optimization potentially via further equity rounds or debt refinancing.

Monitoring quarterly updates for revenue trends alongside legal risk disclosures will be pivotal against backdrop of competitive innovation cycles across EV mobility sectors.

Capital Allocation Strategy: ROE, Dividends, Buybacks, and Reinvestment Insights

Gogoro reports sustained negative ROE approximate -74% under IFRS based on net losses relative to shrinking equity base ([F1]). Dividend payments have been explicitly deferred indefinitely per board declarations prioritizing earnings retention for business operations without scheduled cash dividends or share repurchases ([S11],[S20],[S24]).

Capital is funneled primarily toward R&D investments strengthening product roadmaps alongside infrastructure expansions supporting battery swapping stations (,[S25]). This conservative approach preserves cash amid ongoing losses but limits shareholder distributions which may remain suppressed until profitability materializes.

Supply Chain Governance and Litigation Risks Monitoring

Ongoing legal proceedings include multi-million-dollar claims associated with supplier contracts previously dismissed then appealed with some resolutions attained yet exposures remain circa $4.4 million still contested before Taiwanese courts ([S1],[S9]). Employment litigation mostly resolved favorably lessens contingent liabilities albeit requiring continued monitoring.

Supply chain governance reforms have been adopted following governmental inquiries on domestic content substitution impacting subsidy eligibility emphasizing enhanced internal controls ([S1],[S9]). Cybersecurity governance also commands board level attention via audit committee review cycles ensuring enterprise risk mitigation aligns with digital service continuity demands fundamental to subscription platform reliability ([S9]).

This analysis incorporates solely publicly filed data sources as referenced without conjecture beyond documented disclosures or reported facts by management or third parties cited herein. It is intended for informational purposes supporting due diligence rather than recommending any security transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments