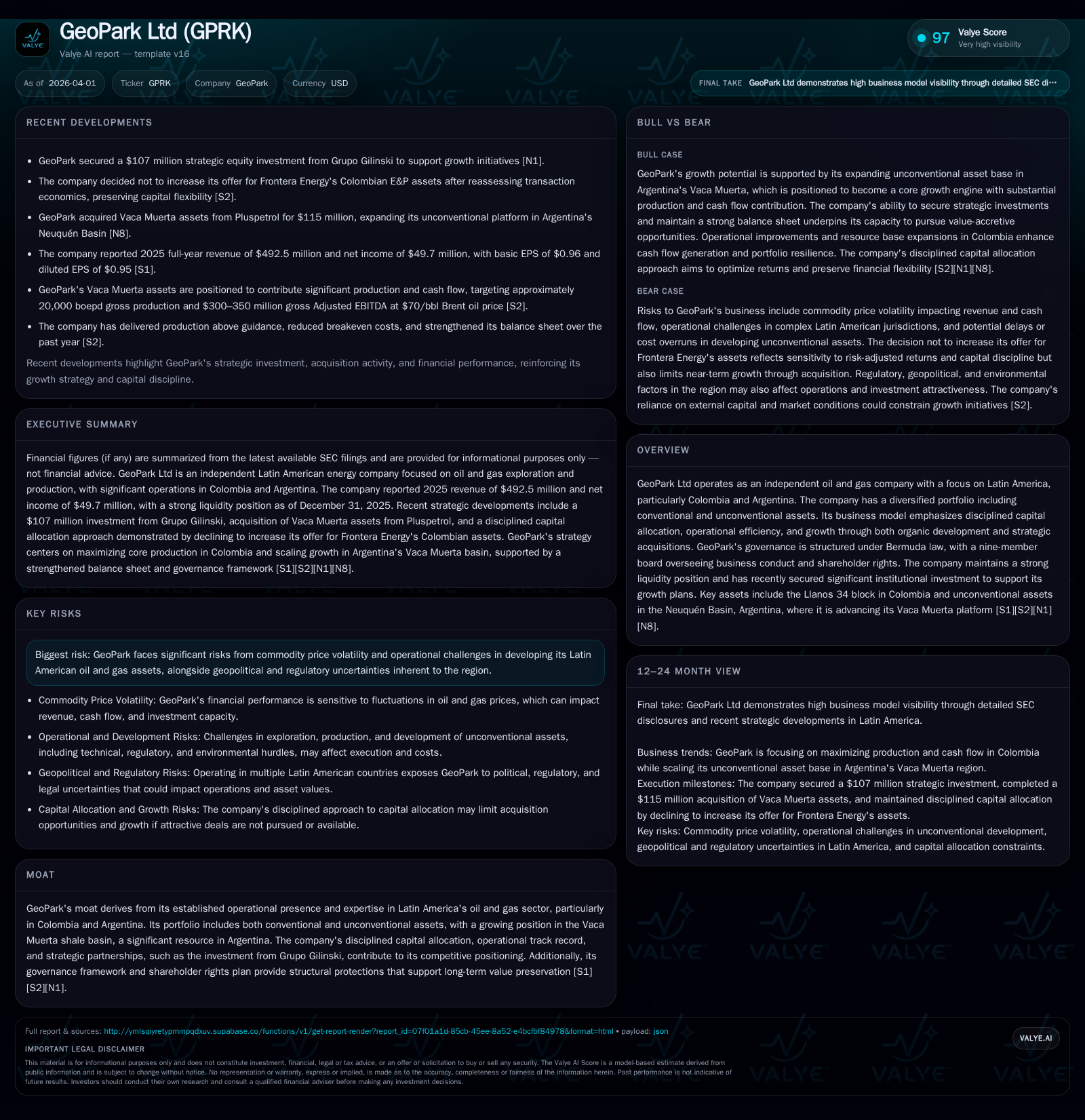

GeoPark Secures Institutional Backing to Support Growth Despite Recent Revenue Decline

GeoPark Ltd's strategic focus on Latin American oil assets and disciplined capital management underpin its operational resilience and growth ambitions.

GeoPark Ltd, an independent oil and gas producer with a diversified portfolio primarily in Colombia and Argentina, experienced a notable decline in revenue and net income in 2025, influenced by commodity price volatility and operational factors. The company has reinforced its financial position through a $107 million strategic investment from Grupo Gilinski, enhancing liquidity to support continued development in key assets like the Llanos 34 block and Argentine unconventional plays within Vaca Muerta. GeoPark maintains a cautious capital allocation approach, balancing organic growth with selective acquisitions while navigating geopolitical and regulatory risks intrinsic to Latin America's oil and gas sector.

Overview

GeoPark Ltd is an independent exploration and production (E&P) company focused on oil and gas assets predominantly across Latin America, specifically Colombia and Argentina. Its asset base combines conventional fields such as the flagship Llanos 34 block in Colombia with unconventional shale developments in Argentina’s Neuquén Basin (Vaca Muerta). The company’s governance is established under Bermuda law with a nine-member board overseeing strategic execution and shareholder protections [S1][S3][N1][N8].

Historical Financial Performance

GeoPark’s recent financial results reflect the cyclicality endemic to the upstream energy sector amid shifting commodity prices. Revenues fell sharply to approximately $492.5 million in FY 2025 from $660.8 million the prior year—a decline of about 25.5%—largely attributable to lower realized oil prices linked closely to Brent benchmarks adjusted for local differentials particularly relevant in Latin America’s regional markets [F1][S1]. This top-line contraction pressured net income down by nearly half, registering $49.7 million compared to nearly $96.4 million in FY 2024 [F1].

Despite this earnings setback, GeoPark maintained a solid balance sheet with total shareholders’ equity reaching $245.8 million at year-end, resulting in an approximate return on equity near 20%, a respectable figure given the top-line challenges [F1]. The company sustains a healthy current ratio of roughly 1.6, indicating sound short-term liquidity from current assets amounting to $219.7 million against current liabilities of $137.2 million [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 493 | 50 | -25.5% | -48.5% |

| 2024 | 661 | 96 | -12.7% | -13.2% |

| 2023 | 757 | 111 | -27.9% | -50.5% |

| 2022 | 1050 | 224 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 20.2 |

| 2024 | 47.4 |

| 2023 | 63.1 |

| 2022 | 194.2 |

Source: SEC companyfacts cache [F1].

Source: SEC filings consolidated by companyfacts snapshot [F1]

The decrease over these years reflects both macro commodity cycles—with Brent crude swinging from lows near $19/bbl to highs above $120/bbl historically—and localized operational considerations including production mix changes.

Drivers Behind Past Performance

Revenue variability traces chiefly to exposure to international oil price fluctuations linked mainly to Brent crude pricing benchmarks but adjusted further for regional crude quality differentials such as Vasconia or Medanito references depending on Colombian or Argentine assets respectively [S1]. GeoPark partially mitigates price risk through derivatives strategies hedging portions of forecast production volumes but remains susceptible broadly to market movements.

Operating costs have also evolved alongside inflationary pressures notably in energy inputs critical for lifting operations—chemical usage, contractor fees—and royalty regimes mandated by national authorities including ANH in Colombia that feature tiered royalties correlated with price thresholds beyond statutory rates [S1]. These fiscal overlays inherently cap profitability when prices retreat.

On the operational front, production campaigns focus on maximizing efficiencies at mature fields like Llanos 34 while progressively scaling unconventional resource extraction via drilling programs targeting Vaca Muerta formations with requisite technology adaptation for shale completions unique relative to conventional reservoirs.

Future Growth Prospects

GeoPark’s growth trajectory hinges heavily on deepening its foothold within Latin America’s hydrocarbon plays with two concurrent levers: sustaining cash flow generation from productive conventional assets primarily within Colombia—expected due to the recent reserve certification upgrade (+22% certified increase in Llanos 34 original oil-in-place) enhancing long-term asset longevity—and ramping unconventional production capacity leveraging recent acquisitions such as Loma Jarillosa Este poised synergistically within Neuquén Basin concepts [N1][S2].

Acquisition discipline remains central; notably, the company declined to increase its bid for Frontera Energy’s Colombian E&P holdings after reassessing risk-adjusted returns deemed below threshold relative to alternative capital uses—underscoring stringent capital allocation policies focused on portfolio resilience rather than opportunistic scale-up without value justification [S2].

Strategic capital injection amounting to $107 million from Grupo Gilinski early in Q1 ‘26 substantially bolsters funding availability, strengthening balance sheet flexibility for ongoing capex programs envisaged at ~$100 million annually mostly directed toward development drilling, facility expansions, and environmental compliance projects aligned with regional sustainability priorities [S3][N2][S18].

Near-term milestones include:

- Advancing Vaca Muerta-scale operations aiming at methodical production uplifts facilitated by enhanced well designs.

- Optimization initiatives at Llanos blocks reducing breakeven costs thus improving cash margins under volatile price regimes.

- Ongoing negotiations with local governments/regulators ensuring contract extensions and permit renewals mitigating geopolitical risk exposure.

Capital Allocation and Returns

GeoPark manifests conservative capital deployment principles framed by prudent financial management consistent with Bermuda corporate governance frameworks emphasizing solvency protection against dividend distributions or share repurchases absent robust cash flow coverage [S5][S6]. The firm conducted share repurchases aggregating nearly $44 million during early-to-mid-2024 through a tender offer but halted buybacks thereafter amid market uncertainty maintaining liquidity buffers exceeding $100 million cash equivalents at end-2025 [F1][S10][S16]. Dividends remain subject to board discretion contingent on profitability and balance sheet metrics without formal policy commitment given cyclical earnings sensitivities.

Balance sheet improvements recently culminated from refinancing steps executed in January/April ‘25 replacing shorter maturities notes due ’27 ($350M & $150M tranches cumulatively) partially via issuance of higher-coupon senior notes due ’30 totaling $550M thereby extending debt maturity profiles lowering refinancing risk over the medium term [S12]. Total outstanding debt reported at approximately $554 million as of December ’25 includes notes plus local bank loans reflecting manageable leverage ratios supported by adjusted EBITDA metrics within covenants restricting incremental indebtedness unless tested favorably pre-incurrence preserving lender confidence [S4][S7][S8][S12].

Industry Context (Analysis)

Latin America’s oil sector presents a complex interplay of attractive resource potential counterbalanced by operational, regulatory, and political challenges including variable fiscal regimes subjecting producers to non-traditional royalty burdens linked not only to production but benchmark pricing bands—differentiated contract terms per basin—and fluctuating currency translation effects impacting local operating costs denominated often in pesos or pesos argentinos versus dollar-priced sales revenues.

Shale exploration within Argentina’s Neuquén Basin remains one of the continent’s most promising growth avenues due to abundant technically recoverable reserves but requires steep upfront capital absorption for multi-stage fracture completions coupled with evolving infrastructure buildout logistics that tighten project IRRs until economies of scale consolidate.

Risks Summary

Primary headwinds encompass exposed commodity pricing vulnerability influencing operating cash flows directly; geopolitical risk profiles tied largely to country-specific regulatory environments where contract terms may be subject to amendments or reinterpretations; operational uncertainties characteristic of both mature conventional fields facing decline curves plus unproven unconventional development economics; currency risk embedded through Argentine peso inflation impacting cost structures; and competitive bidding landscapes limiting accretive acquisition opportunities without premium outlays risking marginal return dilution [S1][N2][N3].

What To Watch (Analysis)

Given absence of explicit forward guidance beyond qualitative commentary from latest reports:

- Monitor commodity price trends as direct determinants of revenue sustainability.

- Track progress on unconventional drilling campaigns including well count ramp-ups across Vaca Muerta sectors influencing production profiles.

- Observe any new asset acquisitions or disposals signaling strategic portfolio shifts.

- Capital expenditure discipline versus realized free cash flow generation indicating balance sheet resilience.

- Potential refinancings or changes in leverage metrics affecting borrowing capacity.

- Regulatory developments within Colombian ANH contracts regarding royalties or contractual tenure extensions impacting operating economics.

- Shareholder activity around institutional ownership levels reflecting strategic control dynamics after Grupo Gilinski’s sizable stake acquisition.

Conclusion

GeoPark Ltd operates amidst fluctuating upstream markets characterized by significant commodity price oscillations tempered through disciplined fiscal stewardship complemented by geographic asset diversification across Latin America’s mature and emerging oil basins. Despite notable declines in recent revenues driven primarily by external macroeconomic variables rather than core operational failures, the company has strategically leveraged institutional backing through Grupo Gilinski partnership enhancing its liquidity position poised for growth execution particularly focused on expansion initiatives within Vaca Muerta alongside stabilizing proven conventional reserves horizons like Llanos blocks deploying technology optimization measures while remaining vigilant over capital efficiency prioritization consistent with its governance frameworks.

This analysis synthesizes publicly available data through April 2026 and does not constitute investment advice or recommendations but aims to objectively present GeoPark Ltd's business status, historical trends, strategic priorities, financial condition, risks, and sector context based on disclosed filings and credible news sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments