POET Technologies Advances Optical Engine Development Amid Significant R&D and Capital Deployment

The company is progressing in product innovation while managing substantial losses and operational risks amid heavy investment in research and development.

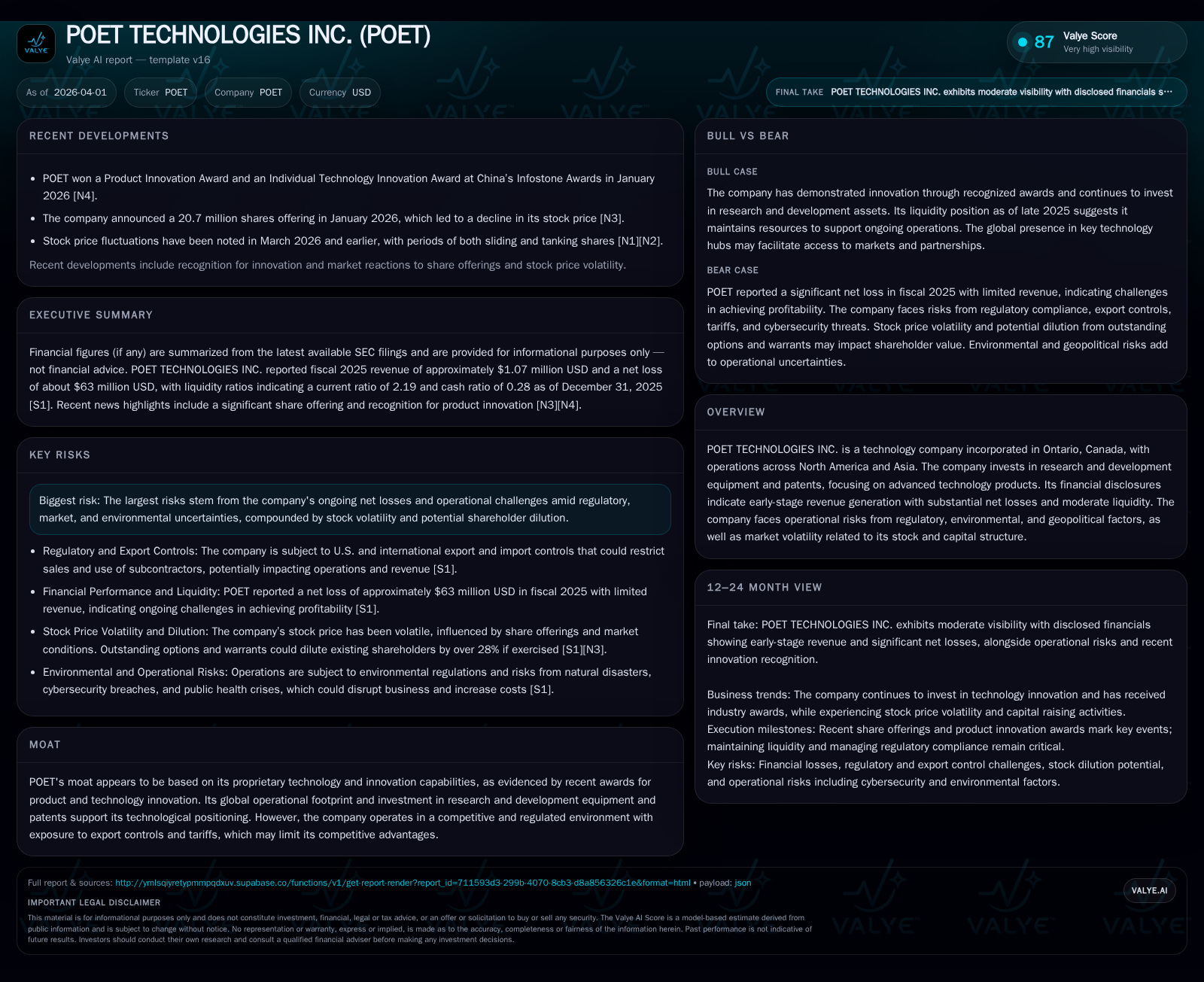

POET Technologies Inc. specializes in integrated optical interposer platforms and hybrid laser light sources for data communications, targeting hyperscale data center markets. Revenue increased significantly in 2025 to over $1 million, reflecting early-stage commercialization, but the company remains deeply unprofitable with a net loss near $63 million due to escalating R&D and operating expenses. POET’s strategic focus is on advancing optical engine chipsets from 400G to 1.6T and deploying proprietary Blazar™ hybrid laser light sources. The company raised approximately $293 million net proceeds in 2025, maintaining a strong liquidity position, but faces ongoing regulatory, geopolitical, environmental, and market risks alongside stock price volatility and shareholder dilution potential.

Company Overview

POET Technologies Inc., headquartered in Ontario, Canada, operates globally with facilities in North America and Asia focused on optical communication technologies. The company's core innovation lies in its proprietary integrated optical interposer platforms coupled with hybrid laser light sources designed for high-speed data transmission applications prevalent in hyperscale data centers supporting artificial intelligence workloads [S1][S7].

Historical Financial Performance

The company's audited financials for the fiscal years ending December 31 demonstrate volatile but evolving performance consistent with its transition from development to early commercial sales:

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 1074865 | -63 | +2494.6% | -11.1% |

| 2024 | 41427 | -57 | -91.1% | -179.7% |

| 2023 | 465777 | -20 | -15.7% | +3.7% |

| 2022 | 552748 | -21 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -34.3 |

| 2024 | -274.0 |

| 2023 | -411.0 |

| 2022 | -183.8 |

Source: SEC companyfacts cache [F1].

Revenue surged by approximately 2495% in 2025 reflecting initial product commercialization yet remains small relative to expenses [F1]. Net losses deepened by about $6 million year-over-year due to expanding operating overhead.

Research and development expenditures were a major cost driver: R&D spending increased roughly 60% from $11.3 million in 2024 to $18.1 million in 2025 [S1][S10][F1]. This growth included consolidation of SPX operations acquired late 2024 and the establishment of new production capacity at Malaysian facilities incurring "bring-up" costs [S1]. Breakdown of R&D expenses includes wages ($7.0 million), subcontract fees ($2.8 million), stock-based compensation ($2.2 million), and supplies ($6.1 million).

Selling and administrative expenses also increased substantially driven by higher stock-based compensation ($3.9 million) and finance advisory fees exceeding $8 million linked to multiple capital raises [S1].

Capital expenditures decreased notably from over $10 million in 2024 to about $2.3 million in 2025 focused on equipment acquisition and patents [S12][S16].

Growth Drivers and Outlook

POET’s growth prospects depend on several key factors:

- Optical Engine Commercialization: Development efforts focus on high-speed transmit (Tx) and receive (Rx) chipsets ranging from 400G up to targeted 1.6 terabits per second modules intended for hyperscale data center customers [S7]. Successful customer qualifications are critical for scaling revenue.

- Blazar™ Hybrid Laser Light Sources: Complementing chipsets are proprietary light source products aimed at AI-centric hyperscale module makers emphasizing energy efficiency and performance gains [S7].

- Manufacturing Capacity Expansion: Integration of SPX operations supports operational control but incurred restructuring costs; Malaysian facilities aim at volume production ramp-up requiring upfront investments [S1][S7].

- Intellectual Property Protection: Ongoing patent filings support technological leadership amid competitive pressures and regulatory export restrictions [S4][S9].

Challenges include regulatory complexities such as stringent export controls especially related to China; tariff uncertainties affecting supply chains; environmental compliance costs; natural disaster risks; and pandemic-related operational impacts [S4][S8][S11][S14].

Milestones & Monitoring Points

Key indicators for progress include:

- Continued revenue growth signaling broader commercial acceptance beyond pilot phases.

- Qualification success for next-generation optical engines (400G/800G currently qualified; early samples for 1.6T underway).

- Production readiness milestones at Malaysian manufacturing sites absorbing SPX assets.

- Commercial deployment progress of Blazar™ light source products.

- Trends toward improved operating leverage as fixed costs are absorbed through higher volume production.

Regular updates on product qualification timelines along with supply chain stability commentary will be essential for assessing trajectory [N1][S2][S3].

Returns & Capital Allocation

Reflecting its developmental stage:

- Return on Equity was approximately -34% for FY2025 calculated from reported net loss relative to equity base [$183.8 million equity end-of-year] [F1].

- Operating cash flow remained negative at about -$31 million consistent with capital-intensive growth phase [F1][S16].

- No dividends or share repurchases have been declared; equity financings dominate capital strategy with net proceeds exceeding $290 million raised during fiscal year 2025 through multiple offerings [S12][S16].

- Stock-based compensation expenses exceed $6 million annually across R&D plus selling/admin functions supporting talent retention amid share price volatility [S1][F1].

- Year-end cash balances stood near $40 million supplemented by short-term investments providing liquidity runway beyond one year absent unexpected disruptions; planned spending includes approximately $313 million remaining capital commitments primarily toward R&D scale-up [S12][F1].

Risks Summary

Major risk factors include:

- Persistent large net losses increasing dilution risk via frequent equity raises.

- Regulatory compliance risks including Foreign Corrupt Practices Act exposure and evolving U.S. export/import controls potentially restricting market access or increasing costs [S4][S6][S9].

- Environmental liabilities potentially driving additional capital expenditure or operational constraints.

- Tariff impositions or trade policy shifts adversely impacting component costs or supply chain reliability.

- Share price volatility driven by small float relative to outstanding warrants/options creating financing frictions or dilution pressure [S14].

- Potential disruption from health crises including pandemics affecting workforce productivity or insurance costs.

- Risk of losing foreign private issuer status on Nasdaq which would increase reporting complexity and compliance costs [S17].

Conclusion & Outlook

POET Technologies typifies an early-stage technology innovator balancing technological progress with significant financial investment demands while navigating complex multi-jurisdictional regulatory environments. Despite initial revenue traction reflecting nascent product commercialization aligned with AI-driven hyperscale demand profiles, the company remains unprofitable amid aggressive R&D scaling.

Robust capital market support throughout fiscal year 2025 has extended financial runway beyond one year; management must now focus on executing customer qualification milestones alongside improving manufacturing scale efficiencies that pave a path toward profitability. Vigilance around regulatory developments, supply chain dynamics, environmental compliance, governance status changes, and shareholder dilution management will be crucial going forward.

Investors should closely track customer adoption rates across optical engine generations alongside evidence of operating leverage improvements supporting margin expansion over the next two years.

This report is based solely on publicly available information as of March 2026 without offering investment advice or recommendations regarding securities transactions involving POET Technologies Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments