SpringBig's Platform Leadership Amid Cannabis Market Challenges and Profitability Pressures

SpringBig leads as a SaaS platform for cannabis marketing and loyalty but faces profitability and liquidity challenges amid evolving regulations.

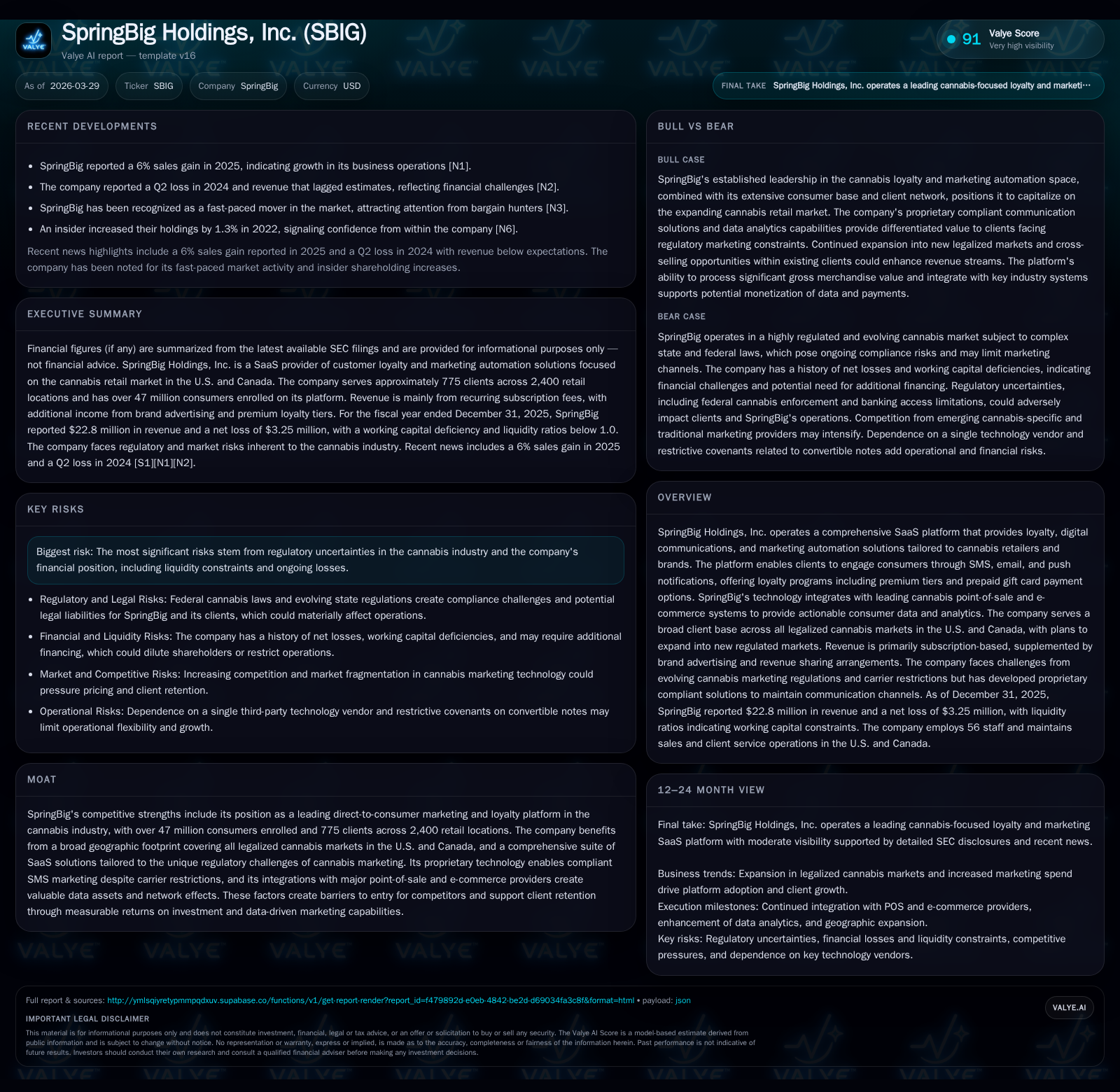

SpringBig Holdings operates a leading SaaS loyalty and marketing platform tailored to the regulated cannabis industry across North America. Revenue declined 7.4% to $22.8 million in FY2025 amid market maturation, with the company serving approximately 775 clients across 2,400 dispensaries and over 47 million enrolled consumers. Its proprietary technology enables compliant SMS-based customer engagement under stringent regulatory restrictions. Despite achieving positive operating cash flow in 2025, SpringBig continues to report operating losses, negative equity, and liquidity pressures influenced by complex federal cannabis laws.

Market Leadership Foundations and Financial Performance

Founded in 2016, SpringBig Holdings has positioned itself as a leading SaaS provider of loyalty and marketing automation solutions for cannabis retailers and brands across all U.S. states and Canadian provinces where cannabis is legal for medical or adult use [S1], [S5]. The company serves approximately 775 clients spanning about 2,400 retail locations with over 47 million enrolled consumers, leveraging deep integrations with major cannabis point-of-sale (POS) systems to provide actionable data insights.

Financially, reported revenue declined by 7.4% to $22.8 million in fiscal year 2025 from $24.6 million in fiscal year 2024, reflecting market maturation and limited expansion into new geographic markets [F1]. Operating losses widened to $1.7 million from $600,000 over the same period despite operational efficiencies, signaling challenges in offsetting costs during competitive pressures [F1].

The plateauing revenue growth is attributed to the finite number of legalized cannabis markets accessible to the company alongside increasing competition within these regions. While consumer enrollment remains strong due to established market presence, incremental growth from new subscribers is constrained without broader legalization developments.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 23 | -3 | 0 | -2 | -7.4% | -73.1% |

| 2024 | 25 | -2 | -1 | -1 | +81.7% | |

| 2023 | -10 | -4 | -8 | +21.7% | ||

| 2022 | -13 | -15 | -16 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 26.0 |

| 2024 | -1 | 19.2 |

| 2023 | -4 | 118.0 |

| 2022 | -15 | 360.4 |

Source: SEC companyfacts cache [F1].

Fiscal years end December 31.

Regulatory Landscape and Compliance Strategies

Marketing in the cannabis sector is heavily regulated by state laws alongside federal prohibitions under the Controlled Substances Act (CSA), which restrict traditional advertising channels such as social media and mass telephony/SMS communications due to tobacco-like advertising bans and carrier limitations [S6]–[S9].

SpringBig’s proprietary platform addresses these constraints by enabling compliant SMS marketing that adheres to TCPA rules alongside FCC and Canadian CRTC regulations through consent capture mechanisms employing double opt-in procedures and automated filtering of invalid phone numbers including burner phones or landlines—a key compliance measure reducing TCPA litigation risk despite the company acting as an intermediary between dispensaries and consumers [S7], [S15], [S25].

Nonetheless regulatory risks remain significant given potential FCC enforcement actions and evolving judicial interpretations that could impose substantial statutory damages per violation. The uncertainty around federal enforcement priorities concerning cannabis further complicates business stability.

Client Footprint Expansion and Growth Potential

SpringBig’s operations span all U.S. states permitting legal cannabis sales plus Canada’s regulated markets—creating a broad geographic moat difficult for competitors to replicate due to fragmented regional compliance requirements [S4], [S5]. The client base of roughly 775 brands/retailers covering about 2,400 retail points reflects deep penetration within licensed dispensaries.

Growth opportunities stem from cross-selling additional services within existing clients who may not have deployed offerings across all locations initially—such as premium loyalty tiers or newly introduced prepaid gift cards integrated into the rewards wallet solution [S4], [S28]. Moreover,

the gross merchandise value (GMV) processed by these retailers exceeds an estimated $5.7 billion annually—highlighting potential upside from monetizing payments processing or reward redemptions beyond subscription fees alone via SpringBig’s platform capabilities [S4].

Integration with major POS providers enhances data quality feeding analytics-driven marketing campaigns critical for client retention amid competitive pricing pressures prevalent in state markets known for price sensitivity [S10], [S25]. These B2B2C network effects strengthen barriers to entry while augmenting data assets essential for SaaS differentiation.

Profitability Trajectory and Cash Flow Dynamics

Despite expanded operating losses in FY2025 (-$1.7 million), the company demonstrates progress relative to prior years’ steep deficits exceeding millions annually while achieving positive operating cash flow of $361k—a marked improvement signaling operational leverage realization stage. Estimated free cash flow after capital expenditures approximates $321k for FY2025 consistent with a software-focused asset-light model emphasizing cloud infrastructure scalability rather than heavy capital investment [F1].

Capital expenditures remain modest at $40k in FY2025 aligning with SaaS business characteristics.

The balance sheet shows negative equity near -$12.5 million reflecting accumulated losses but net income improvements suggest trajectory toward mitigating historical deficits; however this figure requires cautious interpretation given negative book value context typical for emergent tech companies investing ahead of profitability inflection points.

Capital Structure Overview and Liquidity Considerations

Liquidity metrics reveal pressure; a current ratio of approximately 0.54 indicates current liabilities exceed current assets at fiscal year-end—highlighting funding constraints requiring management focus especially given subscription revenue models often receive cash inflows lagging upfront expenses[S14],[F1].

Convertible notes issued in early-2024 impose secured obligations with restrictive covenants potentially constraining financial flexibility for additional debt or equity financing[S14]. Security interests granted to noteholders expose company assets to foreclosure risk if covenants are breached potentially threatening operational continuity[S14].

No dividends or share repurchase programs were declared during FY2025 consistent with prioritizing capital preservation amid regulatory uncertainties[S14],[F1]. This conservative capital management approach aligns with elevated operating losses and external challenges inherent in regulated cannabis markets.

Technological Differentiation and Competitive Positioning

SpringBig’s competitive advantage derives from its ability to facilitate compliant digital communications—including SMS messaging—that bypass conventional restrictions limiting competitors unable to engage consumers directly via text due to TCPA constraints[S25],[S1]. Premium loyalty programs feature paid tiers coupled with prepaid gift card payment options unified within a rewards wallet enhancing consumer spend incentives directly linked to purchase flows[S10],[S25].

Partnerships with leading vertical-specific POS systems improve data fidelity fueling personalized analytics-driven marketing campaigns among retailers/brands[S25],[S10],[S28]. This integration breadth creates network effects: expanding user bases enrich data pools improving campaign precision thereby supporting client retention[S1],[S10].

Auto-connect marketing automation triggered by live consumer behavior enhances campaign timing effectiveness—a critical capability given intense price competition prevalent within cannabis retail[S25].

This comprehensive platform integration positions SpringBig beyond rudimentary competitors offering isolated loyalty mechanics lacking regulatory nuance or full-stack service cohesiveness necessary for evolving cannabis ecosystem demands.

Key Risks From Regulatory Environment and Federal Law Uncertainty

The primary existential risk stems from enduring federal prohibition under the Controlled Substances Act(S6-S9); intensified federal enforcement against clients could materially impact SpringBig through client attrition or forced operational cessation[S6],[N/A]. Bankruptcy protections may be unavailable if judicial relief is sought due to indirect involvement with federally illicit revenues[S7].

TCPA-related litigation risk remains material; although internal compliance controls including double opt-in e-signature tools mitigate exposure[S7],[S15], potential multi-million-dollar statutory damages per violation pose ongoing concerns absent legislative reform.[S15]

Additional risks include limited insurance coverage availability linked directly to client industry participation restricting operational risk insurance options[S8]; reliance on a single third-party technology vendor creating concentration risk threatening service stability[S8]; intellectual property disputes without patent protection potentially undermining competitive advantage[S17]; plus evolving privacy laws increasing compliance burdens[S18].

Stakeholders should monitor these factors closely given their implications on medium-term viability amidst dynamically evolving legal frameworks unique to cannabis software platforms.

This report synthesizes SEC filing disclosures without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments