Luminar Technologies' Asset Sales and Bankruptcy Conclude a Decade of Advanced LiDAR Pursuits

Emerging from pioneering high-performance LiDAR development to bankruptcy and asset liquidation within a decade.

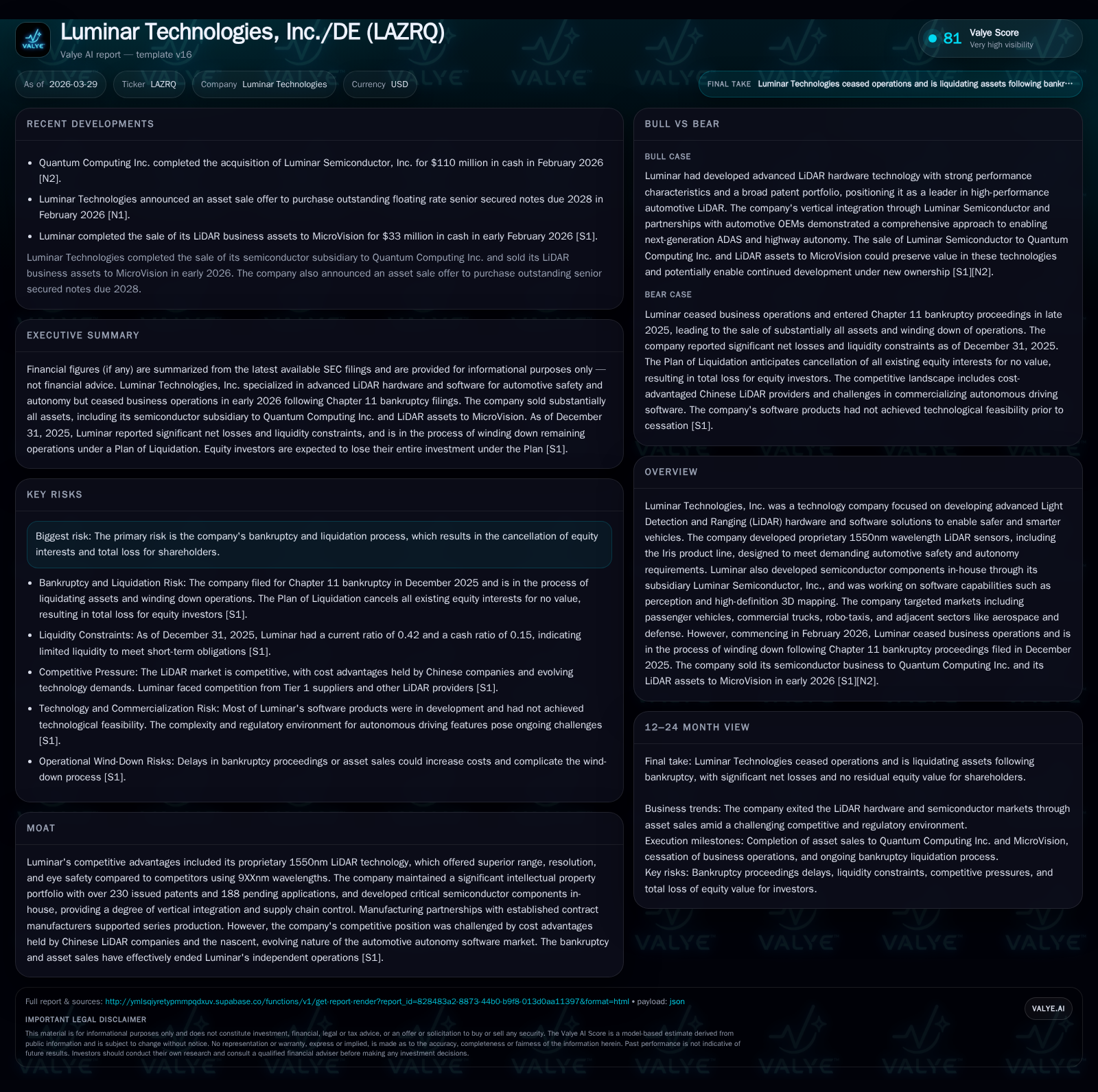

Luminar Technologies, a developer of advanced automotive LiDAR hardware and software, ceased operations and entered Chapter 11 bankruptcy liquidation in early 2026 following significant financial and operational challenges. Despite proprietary 1550nm wavelength LiDAR sensors delivering superior range and resolution, the company struggled with cost competitiveness and scale. Assets including its semiconductor subsidiary and LiDAR business were sold during bankruptcy proceedings, resulting in complete equity value loss for shareholders.

Company Overview

Luminar Technologies, Inc., based in Sunnyvale, California, developed advanced Light Detection and Ranging (LiDAR) solutions aimed at enabling safer and smarter vehicles. The company’s core products centered on proprietary 1550nm wavelength LiDAR sensors—most notably the Iris sensor line—offering superior range and resolution compared to competitors mostly using sub-1000nm lasers [S1][S5][S10]. These sensors targeted advanced driver assistance systems (ADAS) and highway autonomy across passenger vehicles, commercial trucks, robo-taxis, and adjacent markets such as aerospace and defense.

Historical Performance and Financial Overview

Until ceasing operations in early 2026, Luminar invested heavily in R&D and manufacturing capacity development. Despite achieving production milestones such as start of production (SOP) with Volvo Cars’ EX90 in 2024 [S6][S13], the company recorded persistent operating losses:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -366 | -196 | -297 | 2 | -34.1% |

| 2024 | -273 | -277 | -435 | 5 | +52.2% |

| 2023 | -571 | -247 | -563 | 22 | -28.1% |

| 2022 | -446 | -208 | -442 | 16 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -198 | 76.8 |

| 2024 | -282 | 123.7 |

| 2023 | -269 | 254.2 |

| 2022 | -224 | 1688.8 |

Source: SEC companyfacts cache [F1].

(Source: SEC Companyfacts data as of fiscal year-end)

Operating losses narrowed by roughly 32% between FY24 and FY25 but remained significant. Net losses increased markedly in FY25 due to restructuring costs associated with bankruptcy proceedings. Operating cash flows remained negative reflecting continued investment in R&D and scaling manufacturing.

Capital expenditures declined sharply by over 60% in FY25 as investment tapered amid the planned wind-down. Shareholders’ equity turned deeply negative by the end of FY25 signifying severe capital erosion.

Core Technology & Competitive Positioning

Luminar’s key differentiation derived from its use of a 1550nm laser architecture allowing higher photon emissions while maintaining eye safety compared to conventional sub-1000nm alternatives [S5][S10]. This enabled long-range detection up to approximately 600 meters with high angular resolution exceeding 200 points per square degree across wide fields of view—critical for autonomous driving requiring reliable object detection.

Vertical integration through its subsidiary Luminar Semiconductor Inc. consolidated chip design activities producing key components like receiver ASICs and InGaAs photodiodes optimized for this wavelength [S6][S13]. Manufacturing partnerships with Celestica and Fabrinet facilitated initial series production phases starting late 2023/early 2024.

However industry dynamics challenged Luminar: Chinese manufacturers benefited from earlier local adoption leading to economies of scale unmatched by Luminar’s Western-focused higher-spec sensor approach [S10]. Additionally software enabling higher-level autonomy remained nascent with regulatory uncertainty limiting near-term deployment.

Product Portfolio & Market Focus

Hardware:

- Iris: Primary sensor combining transmitter/receiver assemblies enabling configurable vertical fields of view up to ~30 degrees.

- Luminar Halo: Announced in 2024 targeting mass-market adoption with next-generation chips aiming to reduce size (<1 inch height), weight (

1 kg), power (10W), and cost—backwards compatible with Iris systems. Development of Iris+ was discontinued as focus shifted entirely onto Halo platform [S13].

Software:

Luminar developed a full-stack software platform named Sentinel intended to enable proactive safety features such as automatic emergency braking (AEB) and emergency steering interventions targeting SAE Level 2+ autonomy. Most software components remained under development without technological feasibility prior to wind-down [S8][S14].

Markets:

Focus centered on passenger vehicles incorporating ADAS features; commercial trucking seeking highway autonomy benefits; robo-taxi fleets facing extended timelines; plus adjacent sectors like aerospace & defense [S14][S17].

Bankruptcy Proceedings & Asset Disposition

Liquidity pressures culminated in December 2025 when Luminar filed Chapter 11 petitions supported by holders of over 90% of senior notes issued months earlier [S1][S9]. The filing initiated structured liquidation:

- In early February 2026,

- Luminar Semiconductor assets were sold to QCi for approximately $110 million cash consideration.

- Core LiDAR assets were acquired by MicroVision after an auction at approximately $33 million plus adjustments.

These sales received Bankruptcy Court approval providing cash inflows for creditor settlements but ended independent operations [S1][S9][S24]. Staff departures accelerated during winding down [S1][S11].

The company’s Class A common stock was delisted from Nasdaq effective January 23rd then traded on OTC Pink Limited Market under ticker LAZRQ at severely depressed liquidity before expected cancellation upon Plan confirmation eliminating shareholder value entirely [S3][S11][S16]. Equity holders were subordinated behind senior secured creditors resulting in total loss.

Capital Allocation & Returns

No dividends or share repurchases occurred since prior to the pandemic period; buybacks last recorded only through FY21 [F1]. Capital allocation prioritized technology development over shareholder returns.

Financial metrics reflect no positive return on equity; instead negative net income combined with negative equity yields an inconsistent ratio indicative of capital destruction rather than returns generation [F1]. Free cash flow remained substantially negative throughout recent years highlighting ongoing investment despite mounting losses.

Outlook & Conclusion

Post-bankruptcy formal guidance ceased. The Plan of Liquidation remains subject to Bankruptcy Court approval timelines with inherent uncertainties including potential delays increasing wind-down costs affecting residual recoveries [S1][S16][S26].

The automotive sector continues evolving towards mandatory ADAS adoption globally; however Luminar’s operations have ceased with assets transferred to other entities who may integrate technologies into their platforms.

Luminar’s experience underscores challenges faced by high-potential technology innovators contending with capital intensity and competitive cost pressures within emerging autonomous vehicle sensing markets. While proprietary hardware innovations created meaningful technical moats protected by extensive patents [S7], inability to achieve scale or commercialize software limited viability. The bankruptcy proceedings culminating in asset sales mark closure of Luminar as an independent entity with total equity value loss for shareholders.

Disclaimer: This report is based solely on publicly available SEC filings dated through March 29th 2026; it does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments