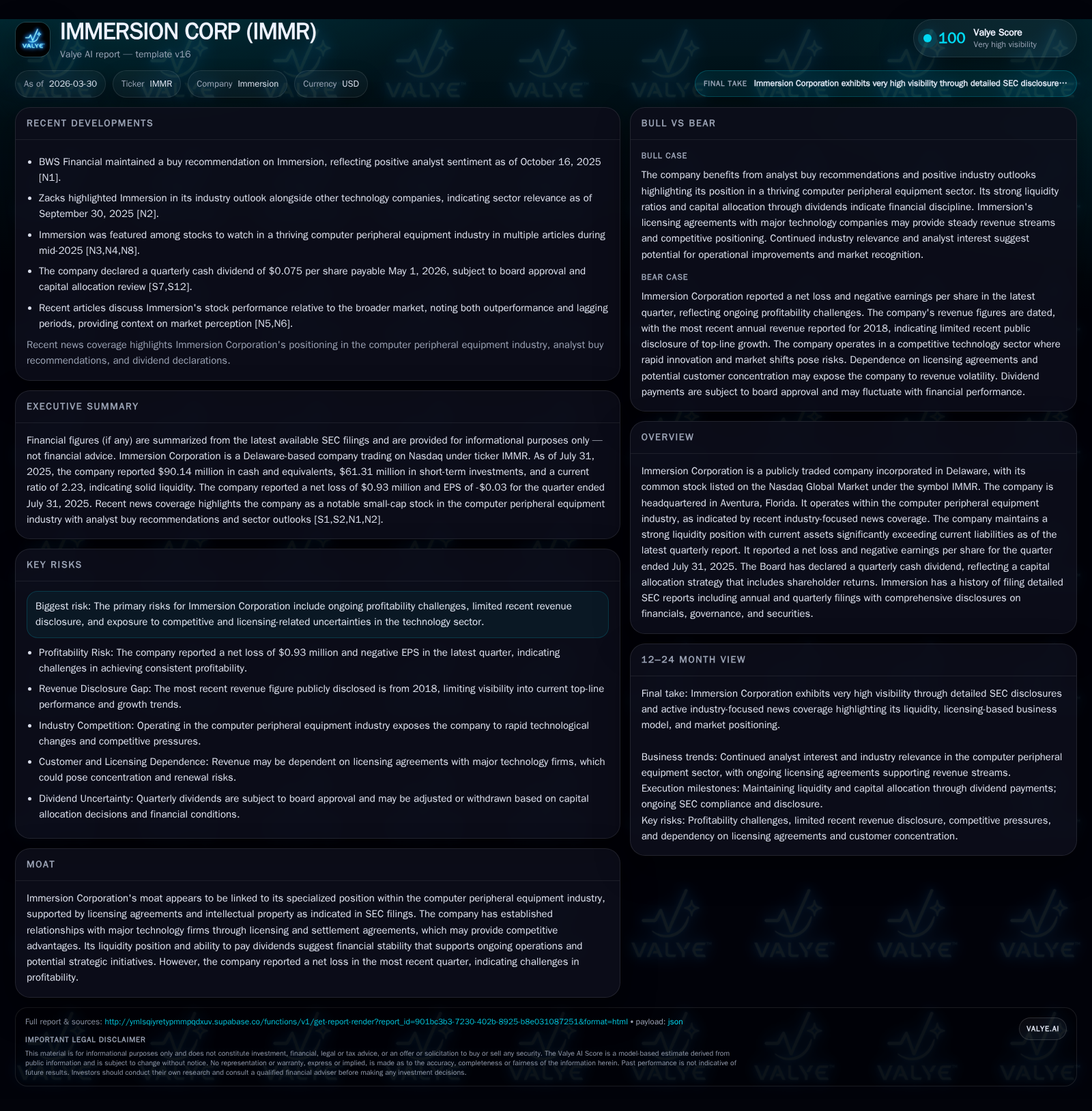

Immersion Corp’s Rebound in Operating Income, Dividend Payouts, and Cash Flow Dynamics

Immersion Corporation’s recent financial results reveal marked operating income growth alongside ongoing cash flow challenges and a steadfast dividend policy.

Immersion Corporation has posted a striking rebound in operating income and net profit for its latest fiscal year, driven by revenue gains and intellectual property licensing engagements. However, the company simultaneously faces significant negative operating cash flow pressures linked to increased capital expenditures and working capital shifts. Despite these cash flow dynamics, the board continues to prioritize shareholder returns through steady dividend increases and modest share repurchases. Looking forward, key industry-specific risks and regulatory compliance matters underscore a cautious outlook that investors should monitor closely.

Impressive Operating Income Growth: Historical Financial Trajectory

Immersion Corporation demonstrated a remarkable turnaround in its operating performance for FY2025 ending April 30, 2025. Revenue expanded substantially by approximately 57.6% compared with prior years, reaching roughly $10.87 million [F1]. This top-line acceleration fueled an outsized leap in operating income—surging over 558% year-over-year to about $118 million [F1]. Net income also gained sharply by nearly 89%, totaling $64.3 million [F1]. These figures signal a meaningful operational rebound compared to comparatively modest profits in preceding years.

However, this financial upswing paradoxically coincided with intensified investments reflected in a substantial increase in capital expenditures (capex), totaling $11.24 million—a more than thirty-seven-thousand percent jump from earlier periods [F1]. The capex surge likely relates to strategic initiatives or IP portfolio expansion efforts critical to sustaining future revenue but exerting near-term cash pressure.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 64 | -58 | 118 | 11 | |

| 2023 | 34 | 21 | 18 | +10.8% | |

| 2022 | 31 | 40 | 24 | 0 | +145.6% |

| 2021 | 12 | 17 | 18 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 13 | 2 | -69 |

| 2023 | 7 | 8 | |

| 2022 | 13 | 40 | |

| 2021 | 0 | 17 |

Source: SEC companyfacts cache [F1].

Note: Latest data reflects fiscal years ending April or December as per source; CFO = operating cash flow.

Revenue Trends and Key Growth Drivers Over Recent Years

The dramatic uplift in FY2025 revenues ties closely with Immersion’s monetization of its intellectual property through licensing agreements and settlements with major technology sector players [S1]. While detailed segment-level revenue disclosures remain sparse, the company's corporate filings indicate active pursuit and enforcement of IP rights within the computer peripheral equipment realm—a niche where patents on haptic technologies often generate sustained royalty streams.

The strategic initiation or renewal of these licensing contracts appears instrumental in driving both revenue growth and improved margins for FY2025 [S1], reinforcing the company’s specialized competitive position.

Additionally, the Board's consistent declaration of quarterly dividends correlates with confidence in steady underlying cash inflows from these arrangements (see Capital Allocation section). Such dividends started at $0.045 per share before increasing to $0.075 per share in subsequent declarations [S9][S21], signaling management’s intent to distribute value even amid operational reinvestments.

Liquidity Position and Working Capital Management

Immersion maintains robust short-term liquidity metrics that support its operational needs despite some quarterly net losses recently reported [S2][F1]. As of July 31, 2025, current assets stood at approximately $796.9 million against current liabilities near $358 million, yielding a healthy current ratio of about 2.23 [F1]. This buffer provides vital operational flexibility while navigating unsettled market conditions.

Several recent SEC Form 8-K filings throughout late 2025 and into Q1 2026 detail ongoing capital structure management activities including debt arrangements or amendments designed to maintain liquidity reserves [S4][S5][S6][S7][S8][S29]. No material liquidity crises are evident from these disclosures; however, compliance notices related to delayed filings hint at some administrative challenges [S24][S26].

Examining the Disconnect: Negative Operating Cash Flow Despite Profitability

Despite reported net profits in fiscal year 2025, Immersion witnessed an unusual negative swing in operating cash flow amounting to roughly -$57.6 million for the same period [F1]. This disparity typically arises from non-cash accounting charges coupled with working capital changes—factors especially pertinent for companies reliant on licensing fee collection cycles.

In Immersion’s case, a notable uptick in capex spending (over $11 million) likely exacerbated cash outflows during the year [F1], representing significant investments possibly aimed at enhancing patent portfolios or developing enforcement capabilities.

Moreover, fluctuations in receivables timings or payables related to licensing receipts can distort CFO temporarily—typical in high-IP-reliant tech firms where revenue recognition does not always align immediately with cash collections.

The resulting free cash flow (CFO minus capex) calculated around -$68.8 million portrays continuing liquidity absorbency that management must reconcile against ongoing dividend commitments.

Intellectual Property Licensing as Moat and Revenue Engine

Central to Immersion's competitive moat is its extensive portfolio of haptic technology patents integral to products ranging from smartphones to gaming peripherals [S1]. The company has historically engaged in proactive enforcement actions resulting in settlement agreements with large tech entities that secure licensing fees contributing materially to revenue streams.

Such IP monetization models rely heavily on sustained patent exclusivity backed by legal enforceability which affords Immersion pricing power unlike typical hardware vendors facing commoditization pressures.

This model’s embedded value is manifest not only through royalties but also via litigation settlements which supplement core earnings—underscoring the essential nature of intangible asset management within the computer peripheral equipment industry.

Capital Allocation: Dividends, Buybacks, and Implications for Shareholders

Immersion demonstrates a clear commitment to returning value via dividends despite mixed profitability trends and negative operating cash flows recently observed [S9][S10][S11][S12][S15][S20][F1]. The Board ratcheted up dividends sequentially from $0.045 per share up to $0.075 per share by early FY2026 period announcements [S9][S21][S25], signaling confidence in sustainable licensing revenues.

Share repurchase activity has been relatively modest compared with dividends—totaling about $2.38 million repurchased by FY2025 versus over $12.85 million paid as dividends [F1]. This selective buyback approach suggests prudent capital stewardship balancing shareholder return objectives against liquidity preservation.

Return on equity measured approximately at 21.6% based on FY2025 net income relative to equity base indicates effective use of shareholder funds amidst evolving market dynamics [F1].

Risks from Competitive & Licensing Uncertainties in Technology Markets

Immersion flags considerable risks centered on profitability pressures derived from intense competition within technology sectors reliant on peripheral innovation alongside uncertainties inherent in licensing negotiations [S19]. Litigation outcomes remain unpredictable while patent validity or infringement claims could materially impact future earnings potential.

Furthermore, administrative hurdles including Nasdaq listing compliance delays due to late SEC filings pose reputational risks potentially affecting investor confidence [S24][S26]. Limited granularity on revenue composition further complicates visibility into sustainable earnings trends.

These risk elements necessitate cautious monitoring given their capacity to constrain growth or disrupt established licensing frameworks underpinning Immersion’s business model.

Forward-Looking Considerations: What to Watch Next for IMMR

Although no explicit forecasts are provided as of latest filings or news disclosures [N0][S3], several milestones warrant close attention:

- Timely filing of delayed SEC reports critical for restoring full investor transparency and Nasdaq compliance.

- Tracking quarterly operating cash flow patterns vis-à-vis capex spending could reveal sustainability of reinvestment strategies.

- Progress on renewing or expanding key intellectual property licenses would materially influence top-line momentum.

- Ongoing dividend declarations will reflect management's assessment of free cash availability amid fiscal pressures.

- Developments regarding outcomes of any pending litigation or new enforcement actions may reshape competitive positioning.

In sum, stakeholders must weigh Immersion’s pronounced profit improvement against nuanced financial challenges embedded in its IP-centric business model while awaiting more granular reporting updates.

Disclaimer: This memorandum is solely for informational purposes based on publicly available data as of March 30, 2026; it does not constitute investment advice nor an offer to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments