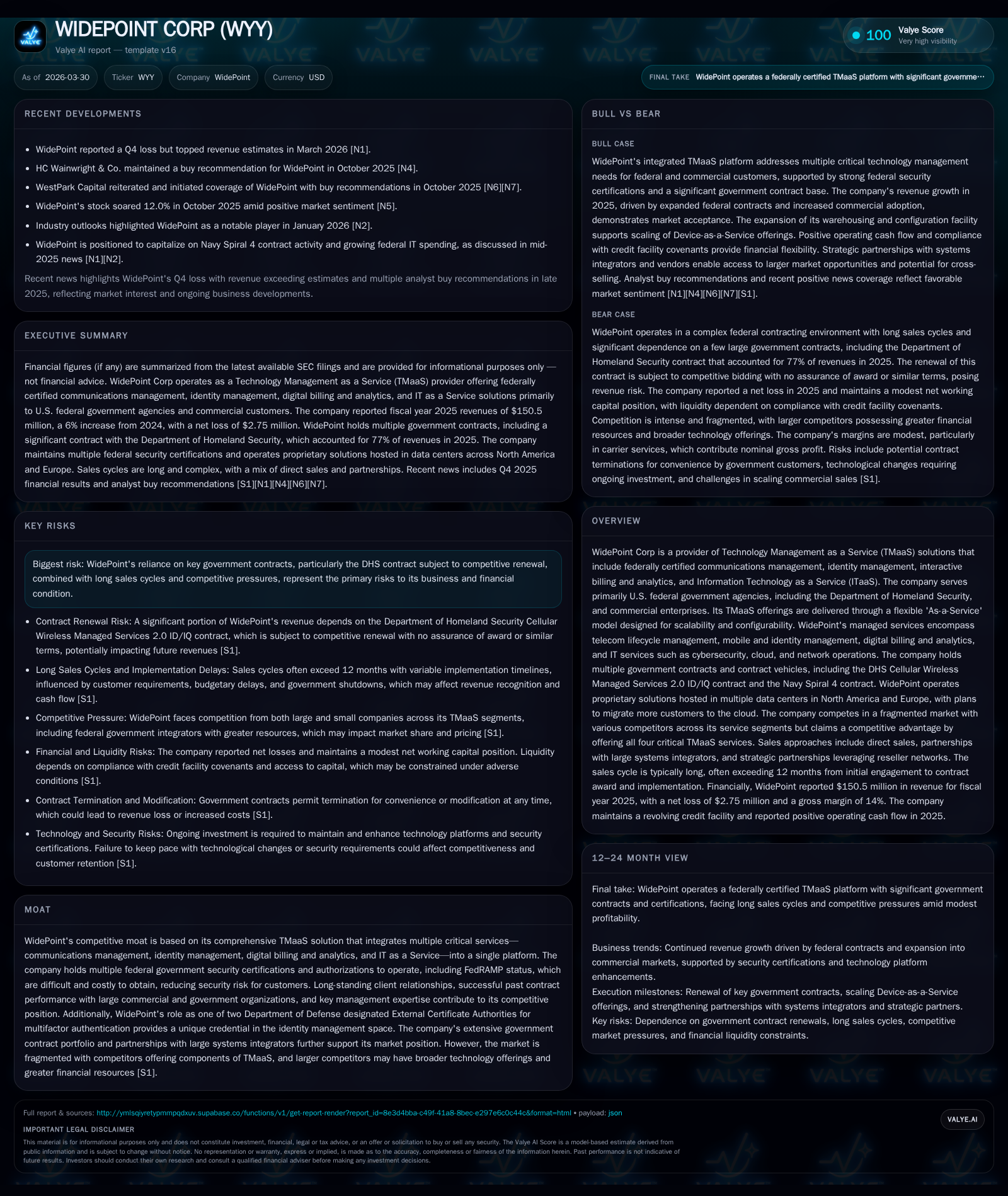

WidePoint Corp Builds on Government TMaaS Leadership Despite Profit Challenges

WidePoint leverages federally certified TMaaS solutions to grow revenues amid ongoing pressure on profitability and reliance on key government contracts.

WidePoint Corp has demonstrated consistent top-line growth driven by its comprehensive Technology Management as a Service (TMaaS) platform, primarily serving U.S. federal agencies. From FY2022 through FY2025, revenue advanced with steady expansion in managed services gross margin. However, profitability remains challenged, with operating losses persisting despite margin improvement. The company's competitive moat is anchored in unique government certifications and contract relationships, notably its designation as one of two DoD External Certificate Authorities. Key risk centers on the renewal of its major DHS CWMS 2.0 IDIQ contract, which accounts for a substantial portion of revenue, introducing uncertainty to financial stability. WidePoint’s capital structure is solid with improving operating cash flow and modest capital expenditures, though it currently refrains from capital returns. Growth catalysts include AI integration and commercial market expansion as the company seeks to diversify beyond federal government dependency.

Historical Revenue Growth and Margin Drivers

WidePoint Corp has exhibited steady revenue growth over the past four fiscal years, increasing from $94.1 million in 2022 to $150.5 million in 2025 [F1]. This growth reflects an expansion in managed services offerings and deeper penetration within federal agency portfolios.

Gross profit improvements were driven primarily by managed services where gross margin rose from 34% in 2024 to 36% in 2025 [S4]. Carrier services, while representing a significant portion of revenue, contribute nominal gross profit due to their commodity-like nature within the TMaaS platform.

Despite revenue gains and margin improvements, operating income remained negative at approximately -$2.8 million in FY2025 but showed marked improvement compared with -$19.6 million in FY2022 [F1]. Elevated general and administrative expenses (~13% of revenue) and labor-intensive service delivery constrain profitability.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 151 | -3 | 6 | -3 | +5.6% | -42.2% |

| 2024 | 143 | -2 | 2 | -2 | +34.5% | +52.2% |

| 2023 | 106 | -4 | 1 | -4 | +12.7% | +82.8% |

| 2022 | 94 | -24 | 6 | -20 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 5 | -23.9 |

| 2024 | 2 | -14.2 |

| 2023 | 0 | -27.6 |

| 2022 | 6 | -132.9 |

Source: SEC companyfacts cache [F1].

Note: Operating cash flow and capex figures are based on reported property and equipment purchases [F1].

TMaaS Portfolio and Government Contract Significance

WidePoint’s Technology Management as a Service (TMaaS) integrates federally certified communications management, Identity Management (IdM), interactive billing with analytics, and IT as a Service (ITaaS). Delivered via a flexible 'Xaas' model, this suite enables customers to scale mobility management easily without costly software redevelopment [S1].

A key differentiator is WidePoint’s role as one of only two Department of Defense designated External Certificate Authorities (ECA), enabling provision of multifactor authentication critical for secure federal access [S15]. The company also offers comprehensive mobile security solutions supporting both federal and private sector clients.

Revenue concentration is notable with approximately 77% of FY2025 revenues stemming from the Department of Homeland Security Cellular Wireless Managed Services (CWMS) 2.0 IDIQ contract [S11]. Additional contracts include Navy Spiral 4 and various GSA schedules providing broad government access [S24]. WidePoint’s FedRAMP Authorized status enhances its competitive positioning by meeting stringent federal cybersecurity standards [S1].

Recurring Revenue Expansion and Competitive Positioning

Expanding recurring managed services remains central to WidePoint’s growth strategy as it targets both federal expansions and commercial sector opportunities [N1],[S1],[S16]. The SaaS-based platform supports steady monthly billing tied closely to user/device counts per contract terms [S11].

Sales efforts combine direct internal teams with partnerships involving large systems integrators that enable participation in sizable procurements often requiring subcontractor roles [S5],[S14]. Strategic alliances extend reach into verticals such as healthcare and telecommunications leveraging partner networks.

Competitive advantages arise from government accreditations (FedRAMP), unique DoD credentials in IdM, integrated multi-faceted technology management solutions avoiding common siloed approaches among peers, and transparent pricing policies that resist commoditization pressures prevalent in the sector [S16],[S17]. Nonetheless, competition includes large incumbents like Leidos alongside mid-sized specialists targeting niche areas.

Contract Renewal Risks: The DHS CWMS 2.0 IDIQ Challenge

The DHS CWMS 2.0 IDIQ contract underpins WidePoint’s financial profile with approximately $116 million or ~77% of revenues in FY2025 tied to it [S20]. The contract's recompete process initiated late in calendar year 2025 remains pending award decision at filing.

Failure to renew or unfavorable terms could materially reduce operating cash flow necessitating significant cost reductions including workforce adjustments given labor is the largest expense category [S20],[S7]. Line-of-credit availability also hinges on billed receivables collateral linked to this contract adding liquidity risk if not adequately renewed [S3]. This concentration risk underscores the importance of diversification efforts.

Profitability Trends Amid Top-Line Gains

Revenue growth moderated to +5.6% year-over-year in FY2025 following double-digit increases prior years; net losses narrowed substantially but remain at -$2.8 million reflecting ongoing investment areas [F1].

Sales & marketing expenses rose slightly to $2.7 million (2% of revenues), while general & administrative costs remain elevated (13%) due partly to legacy infrastructure support and regulatory compliance typical for government contractors [S4],[S18]. Product development targets incremental platform enhancements including cloud migration and AI integration aimed at operational efficiencies.

Return on equity stands negative at approximately -23.9%, consistent with loss-making but improving financial performance supported by positive cash flows [F1]. Capital expenditures remain modest relative to revenues emphasizing scalable software over heavy infrastructure investments.

Capital Structure, Cash Flow Profile, and Shareholder Returns

At December 31, 2025 WidePoint held cash & equivalents near $9.8 million against current liabilities totaling roughly $64 million yielding a current ratio of about 1.04x indicative of tight working capital management [F1],[S3]. A revolving credit facility capped at $4 million expires May 28, 2026 with management expecting renewal [S3],[S6].

Operating cash flow grew markedly to nearly $5.7 million in FY2025 driven by improved collections despite typical public sector invoice timing delays [F1],[S7]. Capital expenditures were low at $237 thousand focused on property and equipment supporting technology platforms.

No dividends or share repurchases have occurred recently reflecting capital retention for reinvestment or liquidity amid competitive uncertainties [F1],[N1].

Growth Catalysts – AI Integration and Commercial Expansion

For fiscal year 2026 plans include several strategic initiatives aimed at sustainable growth:

- Integration of artificial intelligence into TMaaS platforms targeting enhanced cybersecurity through smarter threat detection alongside operational efficiencies reducing response times and costs [S1].

- Expansion into commercial markets leveraging ITaaS capabilities acquired via ITA acquisition enabling cross-selling particularly around Identity Management and telecom lifecycle solutions previously focused on public sector clients [S24].

- Continued cloud migration efforts improving resiliency aligned with evolving remote workforce demands.

- Pursuit of selective acquisitions broadening solution offerings enhancing recurring revenue streams beyond government focus.[S24]

These initiatives reflect a strategic pivot towards diversified revenue sources while leveraging federally compliant technological credentials—a key differentiation factor.

Key Milestones and Investor Considerations

Investors should monitor:

- Outcome of the DHS CWMS successor contract award expected imminently; securing this would underpin baseline revenue stability while failure would require significant repositioning.

- Progress on AI integration manifesting through margin improvements or reduced operating expenses aiding profitability turnaround.

- Success expanding commercial sales pipeline via system integrator partnerships.

- Maintenance of FedRAMP compliance alongside new certifications preserving high security standards critical for government clients.

- Liquidity position monitoring including revolver renewal timing relative to covenant compliance ensuring financial flexibility.

These milestones occur amidst accelerating digital transformation demands within government agencies balanced against heightened competition and pricing pressures common across technology-as-a-service markets.

Disclaimer: This report synthesizes publicly available filings and statements without providing investment advice or predictions beyond documented disclosures from WidePoint Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments