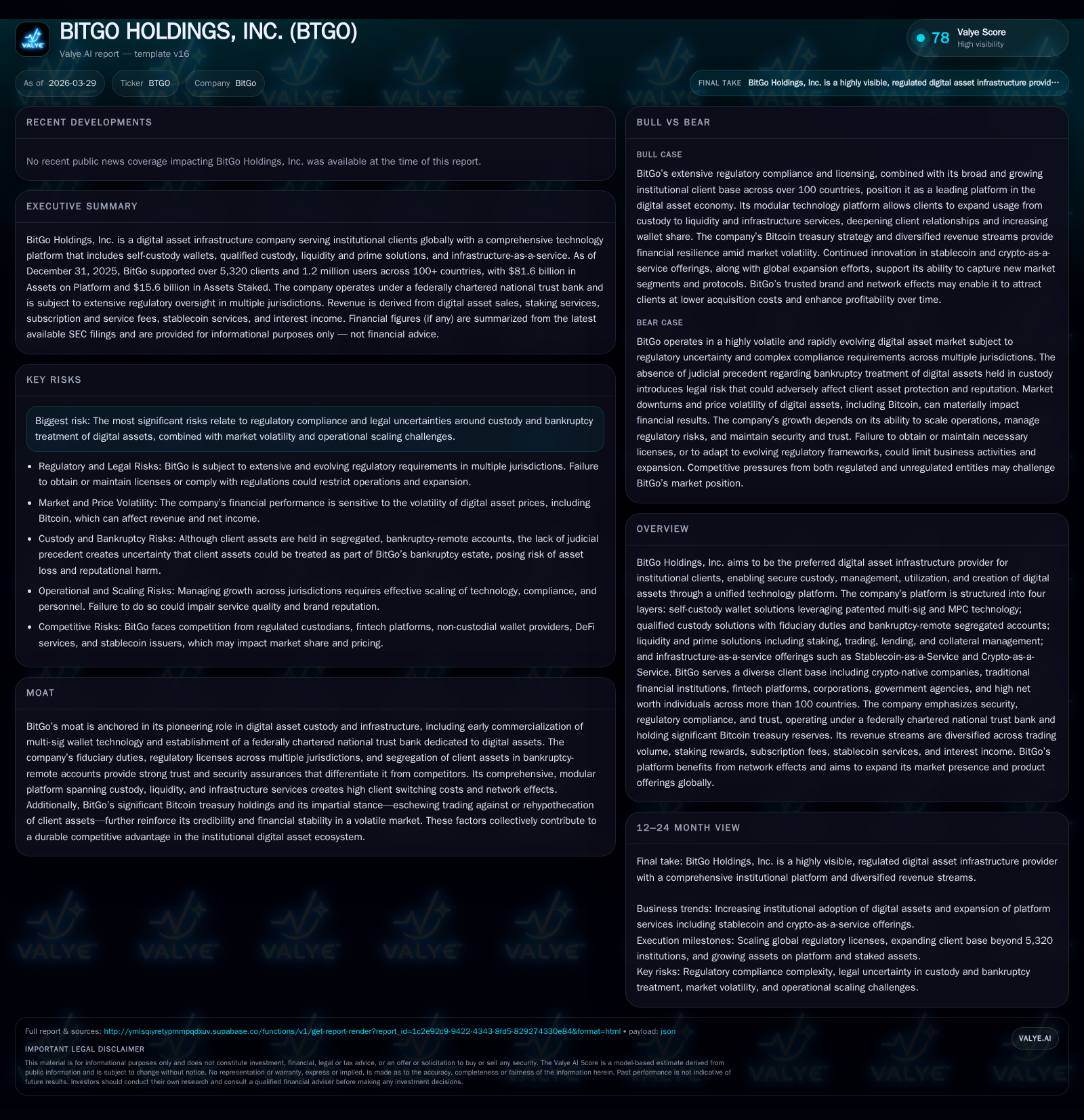

BitGo Holdings’ Digital Asset Infrastructure: Growth, Risks, and Capital Strategy in 2025

A comprehensive analysis of BitGo’s record revenue growth in 2025 driven by digital asset markets, its multi-layered custody platform, regulatory hurdles, and cash flow dynamics.

BitGo Holdings reported a remarkable 424.3% revenue increase in 2025 compared to the prior year, fueled by a recovering digital asset market and increased client engagement. Despite the revenue spike, Assets on Platform declined by 9.2% late in 2025 due to falling digital asset prices, underscoring the volatility intrinsic to the crypto economy. BitGo’s platform integrates patented multi-sig MPC wallet technology with fiduciary custody services and liquidity solutions, driving high client trust amidst evolving global regulatory scrutiny. The company faces ongoing regulatory and compliance risks across multiple jurisdictions but maintains a conservative impartiality strategy by refraining from trading against or rehypothecating client assets. Capital allocation trends reflect fluctuating cash flows tied to market cyclicality, with no disclosed dividend or buyback programs. Monitoring regulatory developments and client metrics will be critical to assess BitGo’s growth trajectory beyond the volatile crypto backdrop.

A Breakthrough Year: BitGo’s Revenue Evolution and Historical Drivers

In fiscal year 2025, BitGo Holdings recorded an extraordinary revenue surge of 424.3% relative to 2024. This growth was principally propelled by a rejuvenated macroeconomic environment that fostered more favorable investor sentiment surrounding digital assets. As prices recovered during much of the year, BitGo saw heightened activity among existing clients along with new client onboarding gains that supported expansion across its product segments — notably in digital asset sales which are directly correlated with trading volume on its platform [S1].

Despite this surge in revenue, BitGo's Assets on Platform (AoP), a critical indicator of scale reflecting total custodied digital assets value tied to prevailing market prices, presented an intriguing dynamic. After growing by nearly 192% from 2023 to 2024 reaching $89.9 billion at year-end 2024, AoP contracted by about 9.2% to $81.6 billion at December 31, 2025 [S1]. This contraction stemmed primarily from digital asset price declines during the final months of the year following peak valuations mid-year.

This reveals how BitGo’s top-line is significantly exposed to the cyclical nature of digital asset valuations where price appreciation expands active balances boosting fees and staking rewards income streams, whereas falling prices depress overall platform metrics.

| FY | Revenue ($B) | Revenue YoY (%) | AoP ($B) | AoP YoY (%) |

|---|---|---|---|---|

| 2023 | ~31 | |||

| 2024 | N/A | N/A | 89.9 | ~191.7 |

| 2025 | 16.2 | 424.3 | 81.6 | -9.2 |

*Revenue growth percentage is based on data cited for fiscal years ending December.

Volatility in Digital Assets: Impact on BitGo’s Performance Metrics

The extreme volatility characteristic of digital asset markets continues to exert a profound influence on BitGo’s financials [S1]. Revenues stem mainly from digital asset sales (trading fees), staking rewards (yield harvesting), subscription services (custody & lending fees), Stablecoin-as-a-Service operations and interest income derived from treasury management.

Such revenue streams are tightly coupled with market activity cycles: when prices rise rapidly clients engage more actively—loading wallets and deploying assets for staking or trading—thereby escalating transaction volumes and fee generation. Conversely, price dips lead to client pullbacks manifested as subdued trading volumes or reduced staked balances which compress revenues.

Moreover, as many digital assets carry speculative components reliant on market adoption expectations alongside technological maturity and regulatory acceptance, unpredictability escalates [S1]. This cyclical volatility contributes to significant fluctuations in operating results quarter-to-quarter.

Platform Capabilities Fueling Expansion: Custody, Liquidity, and Infrastructure Layers

BitGo has evolved beyond simple custody services into a multi-layered institutional infrastructure powerhouse encompassing:

- Self-Custody Wallet Solutions leveraging patented multi-signature (multi-sig) threshold signature scheme MPC cryptography that enhances transaction security without compromising usability.

- Qualified Custody delivered through federally chartered national trust bank entities offering fiduciary duty protections with segregation into bankruptcy-remote accounts ensuring client assets remain untouchable by creditors [S14].

- Liquidity and Prime Services which include staking orchestration facilitating yield farming without risking control loss; trading desks; lending platforms; and collateral management.

- Infrastructure-as-a-Service, such as Stablecoin-as-a-Service enabling clients' stablecoin issuance fully backed by segregated reserves (goUSD project), plus broader Crypto-as-a-Service offerings incorporating integrated fiat on/off ramps and API connectivity.

This modular platform serves a diverse client mix spanning crypto-native firms reliant on self-custody wallets through traditional financial institutions integrating licensed custody within their own products to government agencies requiring highest trust standards [S14].

Regulatory Environment: Navigating Compliance Risks and Legal Uncertainties

BitGo faces an intricate web of regulatory challenges stretching from U.S. federal agencies like the OCC overseeing its national trust bank subsidiary, to state-level supervision including New York Department of Financial Services (NYDFS), as well as international jurisdictions governed under frameworks such as MiCA in the EU granted via BaFIN licensing .

Ongoing examinations have identified compliance gaps requiring significant remedial actions including strengthened due diligence processes, enhanced reporting frameworks, training programs for AML/CTF adherence and cybersecurity fortifications [S4]. The company anticipates continued scrutiny involving audits and possible enforcement actions that might result in fines or imposed business limitations.

Particularly acute are risks tied to DeFi protocol integration exposures where smart contract failures or liquidity crises could cause customer losses triggering litigation or reputational damage [S5]. The firm also confronts CFTC scrutiny due to potential classification issues wherein some supported tokens might be deemed securities or derivatives possibly necessitating new licensure or inviting enforcement actions.

Global licensing uncertainties persist due to divergent foreign regulations that sometimes conflict with U.S.-centric compliance policies impeding rapid global expansion . Furthermore, privacy laws like GDPR introduce operational complexity around cross-border data flows vital for service delivery [S11,S12,S20].

Outlook and Growth Constraints: What the Future Holds for BitGo

Looking ahead into post-2025 dynamics without explicit company guidance available, key determinants for BitGo’s trajectory include sustained recovery or stagnation of digital asset valuations impacting AoP size alongside intensification or easing of regulatory restrictions across critical markets [N1,S1,S14].

While the firm aims to broaden its product suite including innovations around crypto financial services leveraging foundational custody tech—as well as potentially tapping network effects via platforms like goUSD—the overarching volatility of crypto markets remains a natural brake limiting predictable growth scaling.

Business agility may be constrained further by ongoing legislative uncertainties concerning custodial activities versus investment advisory designations, and evolving digital asset classifications that could restrict certain asset listings harming ecosystem breadth.

Capital Allocation Insights: Evaluating Returns, Cash Flow, Dividends, and Buybacks

Due to limited availability of detailed capital returns data including ROE metrics within public disclosures [F1], assessment centers largely on trends described in MD&A regarding cash flow characteristics influenced heavily by market cycles.

Operational cash flow exhibits significant variability echoing top-line fluctuations linked directly with transactional activity changes [S1]. No dividends or share repurchase programs were disclosed suggesting cautious capital stewardship reflective of nascent profitability phases coupled with risk aversion amid unresolved regulatory environments.

Resource deployment appears concentrated on expanding compliance infrastructure rather than shareholder distributions. Investors should monitor forthcoming quarterly cash flow statements for evidence of improving free cash flows enabling potential capital returns.

Competitive Advantages: Technology Edge and Client Trust Dynamics

BitGo’s moat stems fundamentally from pioneering early commercial use of multi-sig wallet technology specifically advanced via proprietary MPC protocols enhancing both security and transaction efficiency—a critical barrier given frequent breaches seen industry-wide .

The establishment of a federally chartered national trust bank focused exclusively on digital assets creates another formidable moat dimension offering bankruptcy-remote segregated accounts affording clients protection not generally matched by competitors lacking such fiduciary oversight mandates.

Moreover, BitGo’s strict impartiality policy prohibits trading against client positions or rehypothecating their assets—a key differentiation reinforcing client trust especially with institutional users wary of conflicts seen at less transparent rivals . The company serves over 5,320 institutional clients globally spanning multiple continents generating high switching costs rooted in integrated platform reliance across custody through liquidity provisioning layers [S14].

Network effects deepen competitive positioning as aggregated scale attracts partners favoring comprehensive regulated platforms over fragmented offerings.

Key Financial Metrics and What to Monitor Going Forward

Below is a concise synopsis capturing selected annual performance indicators through recent years:

| FY | Revenue ($B) | Revenue YoY (%) | Net Income ($M) | CFO ($M) | Capex ($M) |

|---|---|---|---|---|---|

| 2023 | |||||

| 2024 | N/A | N/A | |||

| 2025 | 16.2 | +424 |

Note: Net income, CFO and Capex amounts not explicitly disclosed; table focuses on key available metrics per filings.

Key near-term indicators include monthly/quarterly updates on Assets on Platform reflecting continuing valuation swings; potential announcements related to additional global licensure under evolving frameworks like MiCA; successful rollouts or traction within infrastructure-as-a-service products such as stablecoin issuance; legal developments especially regarding CFTC enforcement outcomes; shifts in overall crypto market sentiment impacting client acquisition rates; progress in internal AI integration affecting operational efficiency; updates on cybersecurity incidences impacting reputation; and any initiation of capital return policies.

Vigilance toward these data points will illuminate whether BitGo sustains momentum through inherent market cycles amid tightening regulation or if headwinds stall further expansion.

This analysis is based solely on publicly available information up to March 29, 2026. It does not constitute investment advice but rather aims at providing an informed perspective on BitGo Holdings’ financial performance dynamics, strategic positioning within the digital asset ecosystem, prevailing risks especially regulatory-related constraints faced by crypto infrastructure providers, and means by which the firm allocates resources given marketplace uncertainties.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments