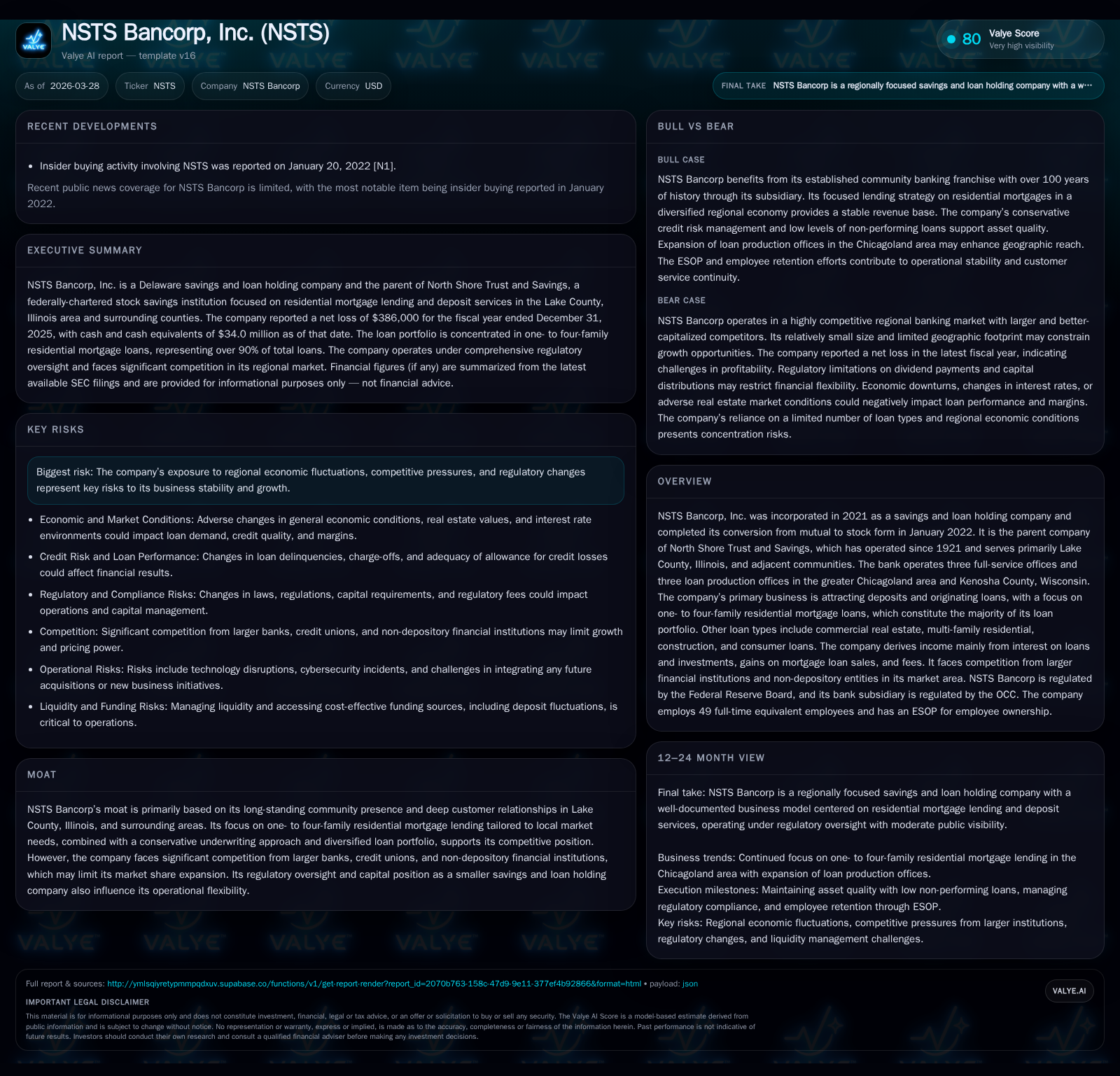

NSTS Bancorp Sustains Local Mortgage Niche Amid Consistent Net Losses and Stable Capital

NSTS Bancorp leverages long-term community ties in Lake County, Illinois, focusing on one- to four-family residential loans, while confronting profitability challenges and regulatory constraints.

NSTS Bancorp, Inc., a relatively newly formed savings and loan holding company succeeding a century-old local bank, concentrates its lending largely on residential mortgages within the greater Chicagoland area. Despite progressive deposit growth and stable capital ratios as per regulatory frameworks, NSTS has reported net losses for three consecutive years through 2025. The company’s future growth depends on maintaining strong local relationships and expanding mortgage origination offices. Yet competition from larger banks and economic fluctuations pose headwinds. Capital allocation strategies currently do not include share repurchases or dividends, reflecting cautious financial management amid risk factors including regional market volatility and regulatory demands.

Company Background and Historical Performance

NSTS Bancorp, Inc. was incorporated in 2021 as a Delaware savings and loan holding company. Its genesis is directly tied to the conversion of North Shore Trust and Savings (the "Bank") from mutual to stock ownership completed in January 2022. The Bank itself has deep roots dating back to 1921, serving primarily Lake County, Illinois alongside adjoining communities including parts of Cook and Will counties as well as Kenosha County in Wisconsin [S1].

The company operates three full-service branch offices plus three loan production centers strategically located within the greater Chicagoland metropolitan region aimed at leveraging local knowledge for mortgage origination growth [S19]. This geospatial expansion particularly includes openings in Aurora and Plainfield since late 2023 which assists in pulling in new clientele beyond existing customer bases.

The foundational business model relies heavily on attracting local deposits coupled with originating predominantly one- to four-family residential mortgage loans—these compose over 91% of the total loan portfolio consistently since at least end-2024, illustrating product concentration but also specialization within a familiar segment [S19], [S24]. Additional lending comprises commercial real estate (around 3%), multi-family residential loans (2.5%), construction (~3%), with consumer loans accounting for only about 0.2%—highlighting a conservative diversification approach appropriate for a community-focused thrift institution.

Financially, NSTS has grappled with sustained net losses through its early public years: documented net income was a mere $27K positive in FY 2022 followed by losses of approximately $3.96 million in FY 2023 improving steadily but still negative at $0.39 million loss by year-end FY 2025 [F1]. Operating cash flow trends present a more resilient picture with growing positive inflows ($4.05 million CFO in 2025), reflecting operational cash generation notwithstanding bottom-line deficits [F1]. Capital expenditures have been modest and declining from $516K (2023) to $104K (2025), reinforcing a lean operating posture.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 0 | 4 | 104000 | +51.1% |

| 2024 | -1 | 9 | 319000 | +80.1% |

| 2023 | -4 | 0 | 516000 | -14755.6% |

| 2022 | 0 | 3 | 215000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 4 | -0.5 |

| 2024 | 1 | 9 | -1.0 |

| 2023 | 2 | 0 | -5.1 |

| 2022 | 3 | 0.0 |

Source: SEC companyfacts cache [F1].

The above table summarizes NSTS Bancorp’s net income trajectory along with cash flow and equity positions.

Growth Prospects

NSTS has charted growth through strategic expansion of its loan production footprint within high-density areas around Chicago via Oak Leaf Community Mortgage lending teams established since mid-2010s and supplemented further post-2023 additions targeting Aurora and Plainfield markets [S19], [S15]. These efforts are designed to tap into burgeoning housing demand dynamics typical of suburban metro expansions.

Maintaining focus on conforming mortgage originations enables sales into secondary markets backed by Freddie Mac and Fannie Mae programs while retaining flexibility to keep unique portfolio loans that fall outside conventional secondary market criteria based on borrower credit nuances or property characteristics [S15]. This blend offers both balance sheet growth potential while managing interest rate risk through active sale participation.

However, expansion is naturally curtailed by formidable competition from considerably larger community banks, credit unions with lower cost deposits and enthusiastic fintech lenders offering digital capabilities attractive especially to younger demographics [S10]. Additionally, regional economic fluctuations impacting employment diversity notably across Lake County’s healthcare/pharma employers versus Cook County governmental bodies may create uneven credit demand patterns.

Regulatory oversight remains significant for NSTS as a smaller entity under Federal Reserve supervision limiting operational agility compared to large national bank peers; this could influence capital strategy decisions thus indirectly capping faster growth pathways absent capital injections or acquisitions not yet contemplated [S25].

Key Forecast Considerations and Milestones

Explicit forward guidance from NSTS is limited; management has articulated their intent to continue enhancing product offerings centered on residential mortgages with geographic expansion within their Illinois-Wisconsin catchment areas serving as a barometer for growth execution success [N/A], [S19], [N/A]. Watchpoints include loan origination volumes emerging from Oak Leaf Community Mortgage operations relative to prior periods as an early indictor.

Credit quality monitoring remains essential given exposure concentration—with allowance adjustments reflecting modest reserve provision swings consistent with very low levels of nonperforming assets (~0.11% of total assets) as of end-2025 emphasizing prudent underwriting standards without aggressive risk-taking evident yet providing leeway against potential economic downturns [S23], [S27].

Regulatory capital status is excellent; the Bank elected use of the Community Bank Leverage Ratio framework achieving a robust leverage ratio exceeding minimum thresholds significantly (CBLR ~24%) positioning it well for organic capital accumulation without imminent capital raises required barring unforeseen stress scenarios [S20].

Dividend or buyback policies are currently restrained influenced by ongoing net losses albeit improving; no repurchases were undertaken during fiscal year ended December 31, 2025 nor were dividends declared helping preserve retained earnings for balance sheet fortification purposes [F1], [S8].

Capital Allocation & Returns Analysis

Return on equity remains negative given trailing net losses—approximately -0.5% calculated for FY 2025 (net loss relative to equity base). This reflects early stage profitability challenges common among thrift companies transitioning post-demutualization while scaling operations amid competitive pressures.

Cash flow generation via operating activities presents a more optimistic view showing internal ability to generate liquidity (+$4.05 million CFO versus minor capex outflow), equating roughly to $3.95 million free cash flow for fiscal year ending December 31, 2025 supporting ongoing loan fundings without resorting extensively to external debt financing.[F1]

No significant long-term debt outstanding except temporarily drawn advances from Federal Home Loan Bank fully retired by mid-2025 evidencing disciplined liquidity management strategies aligned with cautious leverage principles expected from community thrifts.[S6], [S14]

Dividends absence implies capital retention priority while buybacks suspension aligns with repairing cumulative losses compounded over recent years precluding discretionary shareholder returns until clear earnings normalization occurs.[F1], [S8]

Sector Contextual Analysis (Non-company-specific)

In the broader US savings & loan sector landscape focused on local residential lending niches like NSTS occupies private-label originations steadily face headwinds from digital-first competitors leveraging automated underwriting tools lowering costs plus national banks exercising scale economies enabling strategic pricing leveraged against deposits.

Post-pandemic normalization in mortgage rates also affects volume dynamics adversely curbing refinancing surges experienced historically boosting margins temporally whereas institutional investor appetite for whole loans adds pressure on balance sheet composition shifting mix further toward agency-backed sales impacting net interest margin stability.

Risks Summary

NSTS remains exposed chiefly to local economic cycles influenced by employment patterns across manufacturing decline prospects or service sector volatility locally while competing against bigger institutions constraining pricing power or share gains.[N/A],[S1],[S10]

Regulatory changes including possible tightening capital adequacy or stress testing regimes could reduce strategic flexibility particularly given its sub-$3 billion asset size class confines though current regulation lifting some burden via CBLR adoption provides partial reprieve.[S25],[S26]

Information technology risks manifest too; evolving cybersecurity threats or platform disruptions could incur unforeseen remediation costs challenging small organization capabilities versus outsized peer defense mechanisms.[N/A]

Conclusion

NSTS Bancorp’S evolution post-demutualization centers around solidifying its stronghold within defined regional mortgage lending markets supported by legacy customer intimacy accrued over decades through North Shore Trust & Savings lineage. Its financial results denote important progress toward stabilizing losses into marginal negatives accompanied by positive operating cash flows hinting at underlying operational sustainability rather than structural weakness.

Future growth is contingent upon successful geographic expansion converting new market presence into profitable loan originations offsetting pervasive competition locally while balancing conservative underwriting standards maintaining credit quality integrity amidst macroeconomic uncertainties.

Capital discipline reflected through non-distribution of dividends or repurchases evidences prudent stewardship though limits attractiveness from a total return perspective currently.

Investors tracking this entity should vigilantly monitor loan production trends from new offices alongside quarterly updates on asset quality metrics and any shifts in regulatory capital requirements that might influence future outlooks.

Valye News produces company analysis solely for informational purposes without recommending investment decisions. Readers should conduct independent due diligence before forming opinions based on this content.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments