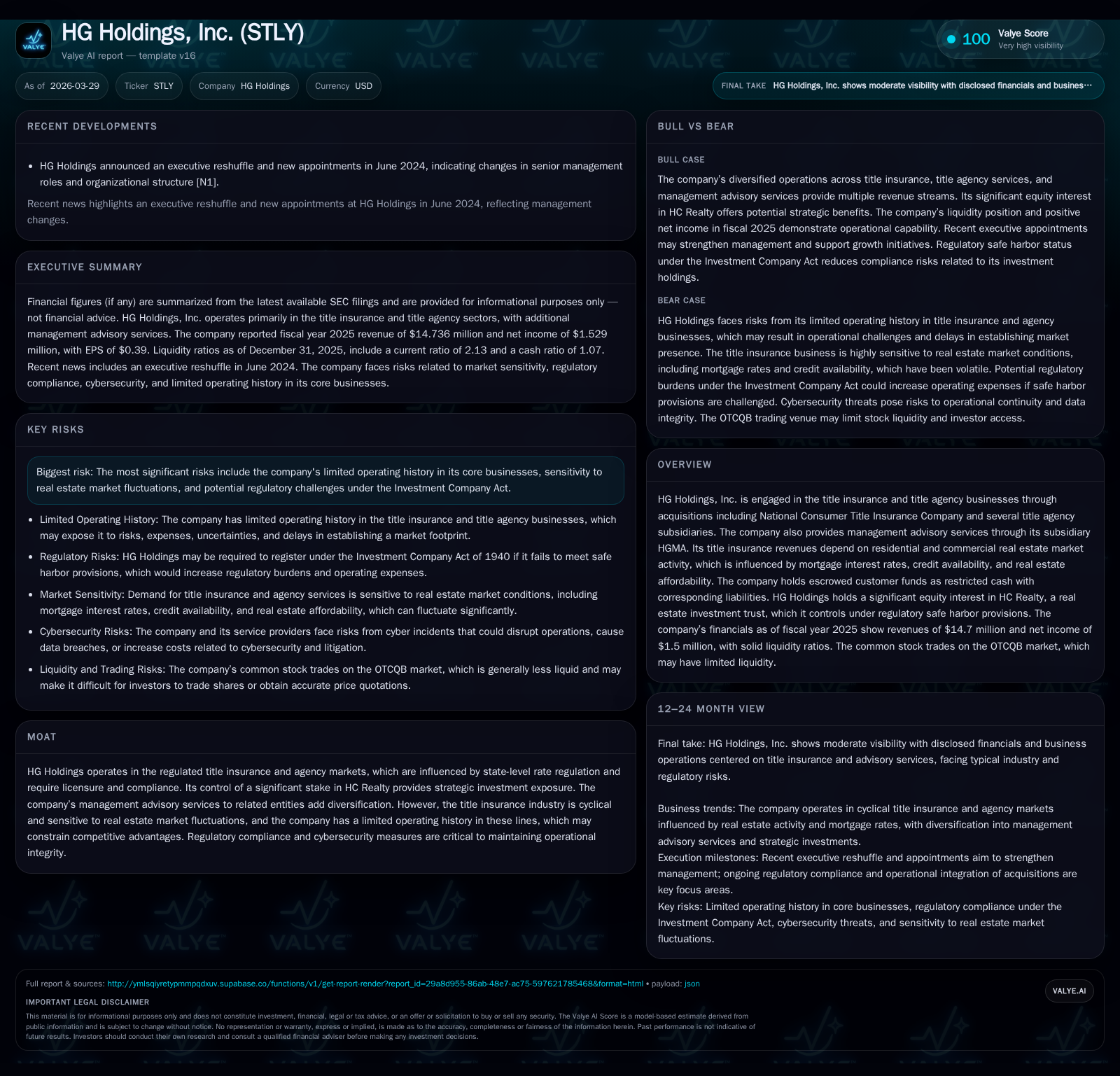

HG Holdings’ Turnaround and New Investment Challenges in Title Insurance

HG Holdings has rebounded to profitability, yet faces market cyclicality and complex regulatory hurdles in expanding its title insurance and real estate investment operations.

After years of operating losses, HG Holdings pivoted in recent fiscal years to post a net income of $1.53 million in FY2025 on revenues of $14.7 million, driven by cyclical recovery in real estate activity and operational improvements. The company’s core title insurance business remains sensitive to mortgage rates and real estate affordability, while its significant equity stake in HC Realty provides strategic diversification but introduces potential regulatory risks under the Investment Company Act. Capital allocation notably accelerated share buybacks in FY2025, signaling confidence amid ongoing liquidity strength. Moving forward, growth will hinge on successful acquisitions and navigating intensified regulatory scrutiny.

Historical Financial Performance: From Losses to Profitability

HG Holdings’ financial trajectory reflects a marked turnaround between FY2024 and FY2025 following several prior years of net losses. Revenues rose from approximately $11.5 million in FY2024 to $14.7 million in FY2025, representing a strong 28% year-over-year increase [F1]. This growth accompanied an encouraging net income swing from a loss of nearly $239,000 in FY2024 to a positive $1.53 million profit in FY2025. Operating cash flows saw a decline from their peak of about $2.7 million in FY2022 down to roughly $878,000 most recently – indicative of tighter cash generation despite improved net results.

The company’s equity base expanded to about $41.7 million as of end-2025, a healthy buffer reflecting retained earnings accumulation and capital management effectiveness. However, operating income remains modest compared with prior negative marks disclosed as far back as FY2018–FY2020 when losses exceeded one million USD annually [F1]. This rebound suggests early stabilization though profitability margins remain thin.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 15 | 2 | 1 | +28.0% | +739.7% | |

| 2024 | 12 | 0 | 2 | 0 | +3.6% | +70.9% |

| 2023 | 11 | -1 | 2 | 51000 | -23.3% | -122.0% |

| 2022 | 14 | 4 | 3 | 67000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 4 | 3.7 | |

| 2024 | 0 | 2 | -0.7 |

| 2023 | 0 | 2 | -2.5 |

| 2022 | 0 | 3 | 11.2 |

Source: SEC companyfacts cache [F1].

Note: Capex was zero or negligible during last two years; dividends not reported recently [F1].

Core Business Drivers: Title Insurance Revenue Dynamics and Market Sensitivity

The primary revenue source for HG Holdings is its title insurance underwriting through National Consumer Title Insurance Company (NCTIC) alongside several agency subsidiaries [N1]. These revenues are highly dependent on residential and commercial real estate transaction volumes which experience pronounced cyclicality influenced by mortgage interest rates, credit availability, and general affordability conditions [S17]. Residential purchase activity typically slows in winter months but picks up seasonally during spring and summer; mortgage refinancing patterns fluctuate primarily with interest rate changes.

As HG Holdings holds escrowed customer funds arising from real estate transactions, these create offsetting restricted cash assets and liabilities on its balance sheet [S1]. The fiduciary nature of these funds imposes operational risk related to internal safeguards against errors or fraud – any failure could lead to financial losses or reputational damage [S4]. This escrow accounting also adds complexity to liquidity management as these cash balances are essentially held on behalf of clients rather than available for corporate use.

Regulatory Landscape and Compliance Challenges Unique to HG Holdings

HG operates within a tightly regulated environment governed at both federal and state levels due to the nature of title insurance activities [S8]. State regulators exercise control over pricing through rate setting statutes that prevent excessive or discriminatory charges; licensing requirements impose ongoing compliance costs [S17]. On the federal side, agencies like the Consumer Financial Protection Bureau (CFPB) enforce consumer protection laws designed to prevent unfair practices within mortgage finance chains including title services [S4].

Additionally, the sizable equity stake held by HG Holdings in HC Realty—a Real Estate Investment Trust (REIT)—poses potential classification risk under the Investment Company Act of 1940 [S1]. If securities owned exceed specified thresholds outside safe harbor exclusions (notably Section 3(a)(1)(C) and Rule 3a-1), the Company may be obligated for additional registration compliance burdens that could raise operational costs and constrain strategic flexibility.

Cybersecurity risks also form an essential part of regulatory concern given the sensitive customer information processed within title operations, requiring sustained investments into IT controls [S8].

Strategic Investment Portfolio: HC Realty Stake and Management Advisory Services

Beyond underwriting title insurance policies, HG has diversified into strategic investments primarily through holding a meaningful equity interest in HC Realty—structured as a REIT—and via management advisory services rendered by its subsidiary HGMA [N1][S2]. Investments are accounted for using the equity method with valuation considerations increasingly nuanced following maturities of fixed-income securities previously held held-to-maturity [S5].

The Company acknowledges investment-related losses flowing through ‘‘Income (loss) from investments in related parties’’ line items due to HC Realty’s performance outcomes; such losses are pre-tax given REIT status [S2]. Meanwhile, HGMA provides management services adding recurring fee income not directly tied to title insurance underwriting volumes—thereby offering some revenue diversification.

This hybrid operational model requires balancing risk-return tradeoffs between steady but cyclical insurance operations juxtaposed with more market-sensitive investment exposures managed under regulatory safe harbor provisions.

Capital Allocation Review: Balancing Buybacks, Dividends, Cash Flow, and Liquidity

In fiscal year ending December 2025, HG Holdings deployed approximately $4.38 million toward common stock repurchases—a dramatic increase over prior years where buybacks hovered below $250 thousand annually—with no current dividend distributions noted [F1][S18][S24]. This sizable repurchase activity followed a significant reduction in shares outstanding tied partially to agreements executed with large shareholders managed by Solas Capital Management LLC [S18].

Operating cash flow decreased sharply from $1.96 million in FY2024 to about $878 thousand in FY2025 while capital expenditures remained minimal (zero or near-zero) reducing pressure on free cash flow generation [F1]. Free cash flow approximated operating cash flow given negligible capex spend.

At year-end FY2025 total cash balances stood at over $10 million supported by strong liquidity metrics including a current ratio near 2.13 as measured at latest available quarterly data [F1][S14]. Return on equity was modest at roughly 3.7%, reflecting recovery but still constrained profitability levels relative to asset base.

Overall capital allocation appears focused on balancing shareholder returns through active buybacks while maintaining sufficient liquidity buffers amid sector cyclicality.

Growth Prospects Constrained by Cyclicality and Limited Operating History

Management commentary acknowledges that future growth will likely be underpinned by further acquisitions within title insurance agency lines alongside organic volume increases linked closely to underlying real estate market conditions [S1][N1]. However, integration challenges remain salient given HG’s limited historical operating track record extending back only several years following key acquisitions such as NCTIC.

Volatility in interest rates influencing refinance demand plus broader economic factors shaping residential/commercial transaction volumes present ongoing top-line uncertainty [S8][S27]. Competitive pressures are notable given dominance by large incumbents controlling majority market share nationally constraining pricing power.

Further regulatory evolution especially around investment company classification status could impose additional operational constraints limiting strategic maneuvering room [S4][S8]. As such growth outlook carries cautionary tones emphasizing execution risk despite improving financial footing.

Monitoring Forward Milestones: What Investors Should Watch Next

No explicit financial guidance has been provided; hence monitoring key operational indicators will be critical for assessing trajectory:

- Trends in net premiums written reported by NCTIC serving as proximal driver of core title insurance revenues [S2];

- Regulatory developments/deadlines concerning potential registration under Investment Company Act due to extent/value of ‘‘investment securities’’ holdings especially HC Realty interests [S1];

- Patterns of capital deployment including continued buyback activity or shifts toward dividends indicating management priorities;

- Real estate market developments impacting volume-sensitive revenue streams such as mortgage rate movements or credit availability shifts;

- Execution progress on targeted acquisitions adding scale/capabilities within agency businesses underpinning long-term growth aspirations.

These factors collectively will shape whether HG Holdings can sustain its turnaround momentum amid structural challenges intrinsic to its business model.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available filings and does not constitute investment advice or recommendations. Readers should consult professional advisors before making any decisions related to securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments