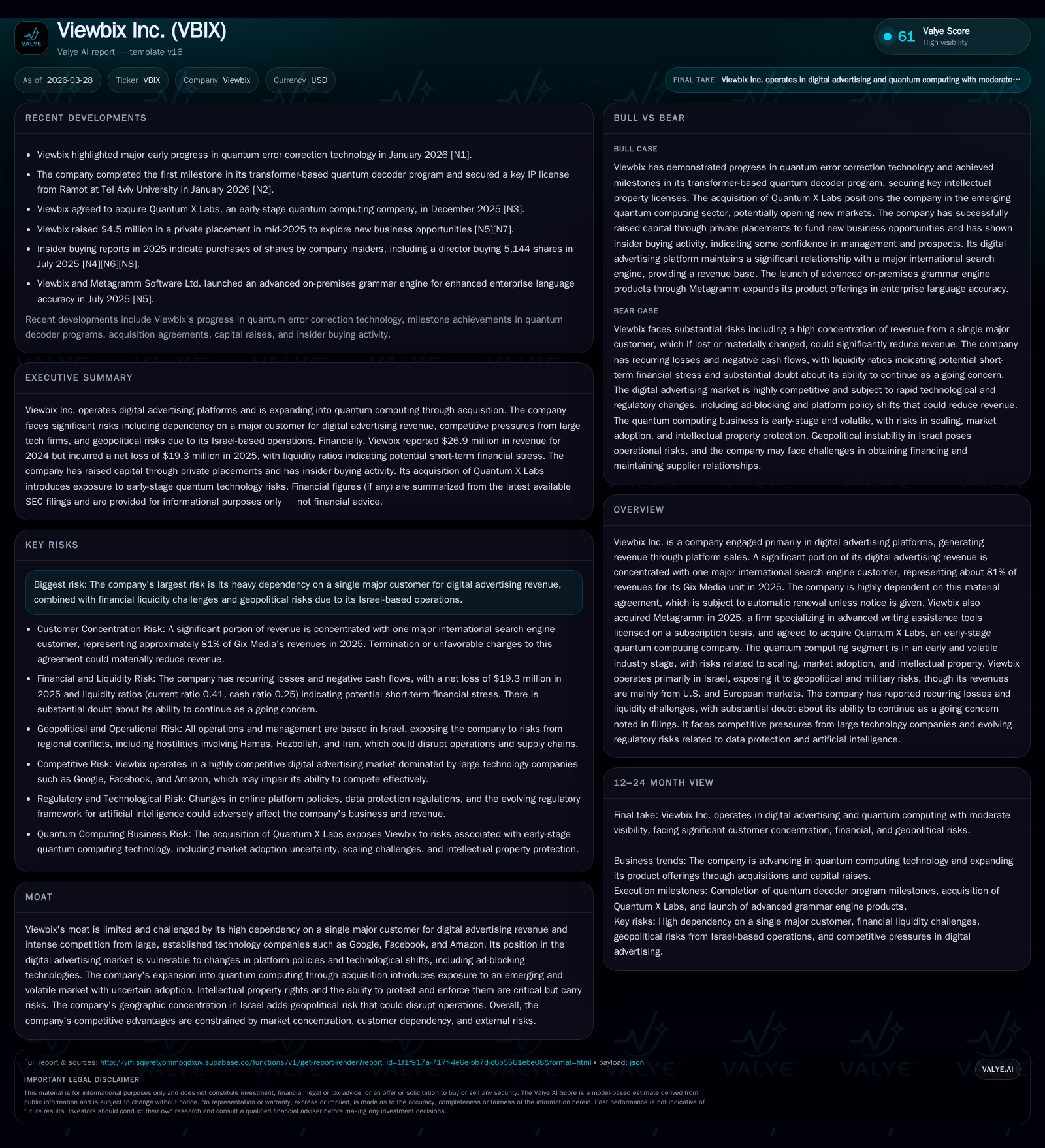

Viewbix Inc. Confronts Revenue Concentration and Liquidity Strains While Expanding into Quantum Computing

Viewbix’s heavy reliance on a single major digital advertising customer poses significant risk as it diversifies into nascent quantum computing technology.

Viewbix Inc., primarily a digital advertising platform provider, saw a sharp revenue decline in 2024 linked to its concentrated customer base dominated by one large international search engine client responsible for 81% of its Gix Media unit revenue in 2025. The company faces ongoing liquidity challenges and operating losses, exacerbated by geopolitical risks from its Israeli operational base. Recent acquisitions in advanced writing tools and quantum computing represent strategic diversification efforts but introduce new execution and market uncertainties. Financial performance underscores high operational strain: despite improving operating income trends in 2025, net losses deepened and liquidity remains constrained with a current ratio below 0.5.

Historical Financial Performance

Viewbix's financial trajectory over recent years highlights significant volatility centered on its core digital advertising business. Revenue reached $79.6 million in FY2023 but plunged by approximately 66% to $26.9 million in FY2024 [F1]. This steep decline reflects the company's concentrated exposure to a single major international search engine customer within its Gix Media segment, which accounted for roughly 81% of that unit’s revenues in 2025 [S10]. The reliance on this single customer creates a substantial renewal risk given the agreement automatically renews annually unless either party opts out with sufficient notice.

Operating income followed this contraction showing a volatile pattern: profit was recorded at $2.7 million positive in FY2022 but shifted negatively to -$7.47 million in FY2023, worsening further to -$11.55 million in FY2024 before improving somewhat to -$2.18 million in FY2025 [F1]. Despite this narrowing of operating losses last year, net income deteriorated markedly to a loss of $19.3 million in FY2025 versus $12.05 million loss in FY2024, indicating increased non-operating expenses or impairments [F1].

Operating cash flow trends show improvement with positive cash generation rising from $934k in FY2023 to $1.54 million in FY2024 [F1], supporting modest free cash flow after minimal capital expenditures historically capped below $60k annually [F1]. However, the balance sheet reflects precarious liquidity positioning; cash and equivalents stood at only around $1 million at the end of 2025 while current liabilities more than double current assets leading to a current ratio of just 0.41 [F1]. This low ratio underscores near-term payment vulnerabilities.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -19 | -2 | -60.0% | |||

| 2024 | 27 | -12 | 2 | -12 | -66.2% | -64.6% |

| 2023 | 80 | -7 | 1 | -7 | -26253.6% | |

| 2022 | 0 | 3 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -386.6 | |

| 2024 | 2 | -208.9 |

| 2023 | 1 | -49.4 |

| 2022 | 3 | 0.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue breakdown for FY2025 not fully disclosed; operating income and net loss suggest continuing strain.

Business Model and Concentration Risks

Viewbix operates predominantly as a digital advertising platform provider delivering services through Gix Media, heavily reliant on programmatic ad inventory tied primarily to one global search engine partner whose account constitutes the bulk of revenues [S10]. This dependency manifests significant contract renewal risk given the automatic rollover every year unless terminated well ahead of time [S10]. Any adverse change or termination would materially impair revenue generation unless alternative comprehensive supply relationships are swiftly established — a challenging feat given the oligopolistic nature of Western internet search advertising dominated by titans like Google and Microsoft.

The digital advertising revenue base is also vulnerable to shifting policies by browsers, search engines, social media platforms around ad presentation formats, data usage permissions, cookie regulations, and ad-blocker proliferation which may constrain monetization [S1][S13]. Competitors such as Google, Facebook (Meta), and Amazon wield dominant ecosystem control which could squeeze Viewbix’s margins or pipeline opportunities through platform updates or preferential partner arrangements [S1].

Strategic Diversification Efforts

In response to these constraints, Viewbix acquired Metagramm in March 2025—a firm specializing in advanced writing assistance tools licensed via subscriptions—and agreed to acquire Quantum X Labs, an early-stage quantum computing company focused on developing scalable quantum solutions [S2][S24]. These moves signal a pivot attempt away from pure-play digital advertising toward technology segments with promising long-term growth characteristics yet considerable execution risk.

Metagramm's subscription-based model provides recurring revenues that differ from Viewbix’s traditional platform sales model but integration challenges such as technical compatibility and cultural alignment pose obstacles that could delay anticipated benefits [S2]. Quantum X Labs operates within an embryonic industry characterized by costly R&D cycles, unproven commercial models, potential IP disputes including inventorship claims, and lengthy patent prosecution coupled with global enforcement complexities [S6][S9][S22][S24].

Market adoption timelines for quantum technologies remain speculative given the fundamental nature of breakthroughs needed—not only hardware scaling but also practical deployment via quantum networks—which drives uncertainty around Quantum X Labs’ ability to scale effectively amid intensifying competition from other niche players pursuing qubit fidelity advancements [S24][S25]. Intellectual property litigation risks go hand-in-hand with emerging tech ventures where proprietary algorithms or manufacturing processes are contested frequently [S15][S16].

Liquidity and Capital Structure Constraints

Financially, Viewbix faces pronounced liquidity pressures reflected by meager cash balances ($1M), current liabilities exceeding assets by over $2.4M (current ratio: ~0.41), recurring net losses culminating in nearly $20M deficit for FY2025 alone, and reliance on credit facilities subject to covenants tied tightly to financial performance metrics that have deteriorated sharply post-2023 revenue contraction [F1][S4][S5].

The company’s ability to secure additional financing is uncertain given these negative trends alongside geopolitical risks stemming from its Israeli operational locus, where regional conflict dynamics could disrupt supply chain continuity or personnel availability affecting business continuity plans [S14][S23]. Management has publicly expressed substantial doubt over continuing as a going concern without successful capital raises or operational improvements [S2]. There have been no dividend payments historically nor plans disclosed for share repurchases; retained earnings are directed at sustaining operations alongside strategic investment efforts [S11].

Competitive Environment and Regulatory Risks

Viewbix confronts stiff competition not only from dominant digital advertising juggernauts but also emerging entrants leveraging AI-driven programmatic platforms—efficiency gains here may compress margins further if Viewbix cannot match innovation speed or scale economics [S17][S20]. Additionally, rapid evolution of data protection legislation globally—including GDPR-like statutes, privacy-focused reforms such as the Colorado AI Act effective February 2026—impose compliance costs that can erode profitability or restrict targeting practices integral to effective digital advertising campaigns [S23][S25][S26][S28].

Moreover, intellectual property risks extend beyond emerging quantum ventures into traditional realms where infringement claims can lead to costly litigation settlements or injunctive relief that impedes product offerings critically dependent on proprietary technology stacks [S19][S20]. Cybersecurity threats potentially compromise infrastructure stability or user trust damaging reputational integrity crucial for client retention particularly across large enterprise accounts such as their key Gix Major Customer [S23].

Future Outlook Analysis

Absent explicit guidance disclosures regarding upcoming milestones or forecasts in recent filings or news releases—the analyst paradigm suggests closely monitoring three pivotal elements:

- Renewal status and terms of the critical Gix Major Customer contract due for annual automatic renewal with any non-renewal notice required at least three months beforehand;

- Operational integration success of Metagramm subscription services including evidence of cross-product synergy generating stable recurring revenues;

- Progress benchmarks related to Quantum X Labs’ technology development roadmaps alongside patent application successes or resolution of any IP disputes.

The degree to which Viewbix can alleviate revenue concentration risk through diversified product lines while managing liquidity constraints will determine near-term viability against market competition intensified by entrenched incumbents who hold significant structural advantages including scale economies and broader advertiser ecosystems.

Returns and Capital Allocation Summary

Return metrics paint a challenging picture: with net losses dominating equity levels ($19M net loss vs ~$5M equity for an estimated negative ROE near -386%) reflecting impaired capital efficiency metrics [F1]. Cash flow from operations remains positive yet modest ($1.54M for FY2024), sufficient only marginally above minimal capex spend yielding small free cash flows supportive chiefly for maintaining day-to-day operations rather than funding expansions or debt repayments robustly.

Dividends have never been declared nor initiated consistent with a growth/reinvestment policy mandated by financial distress conditions [S11]. Buybacks similarly absent given pressing liquidity preservation requirements.

Conclusion

Viewbix Inc.’s narrative is marked by significant performance headwinds rooted mainly in excessive dependency on one dominant advertising customer within an intensely competitive digital ad ecosystem controlled by major technology giants. Despite notable cost control leading towards narrower operating deficits recently achieved amid rapidly shrinking top-line revenue—net losses remain elevated underscoring systemic challenges.

Diversification strategies via acquisition of Metagramm’s subscription-based software assets plus entry into early-stage quantum computing through Quantum X Labs offer potential avenues for future growth albeit accompanied by heightened operational complexity, technological uncertainty, intellectual property risks, and managerial distraction.

Liquidity constraints paired with geopolitical exposure inherent from Israeli headquarters inject added vulnerability concerning continuity risk raising questions over capacity to execute strategic plans without adequate external financing or dramatic operational turnaround.

Investors should monitor upcoming contract renewals with their primary customer as well as tangible progress integrating acquisitions while tracking cash runway extensions under existing debt covenants.

Disclaimer: This analysis is for informational purposes solely based on publicly available data as of March 28, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments