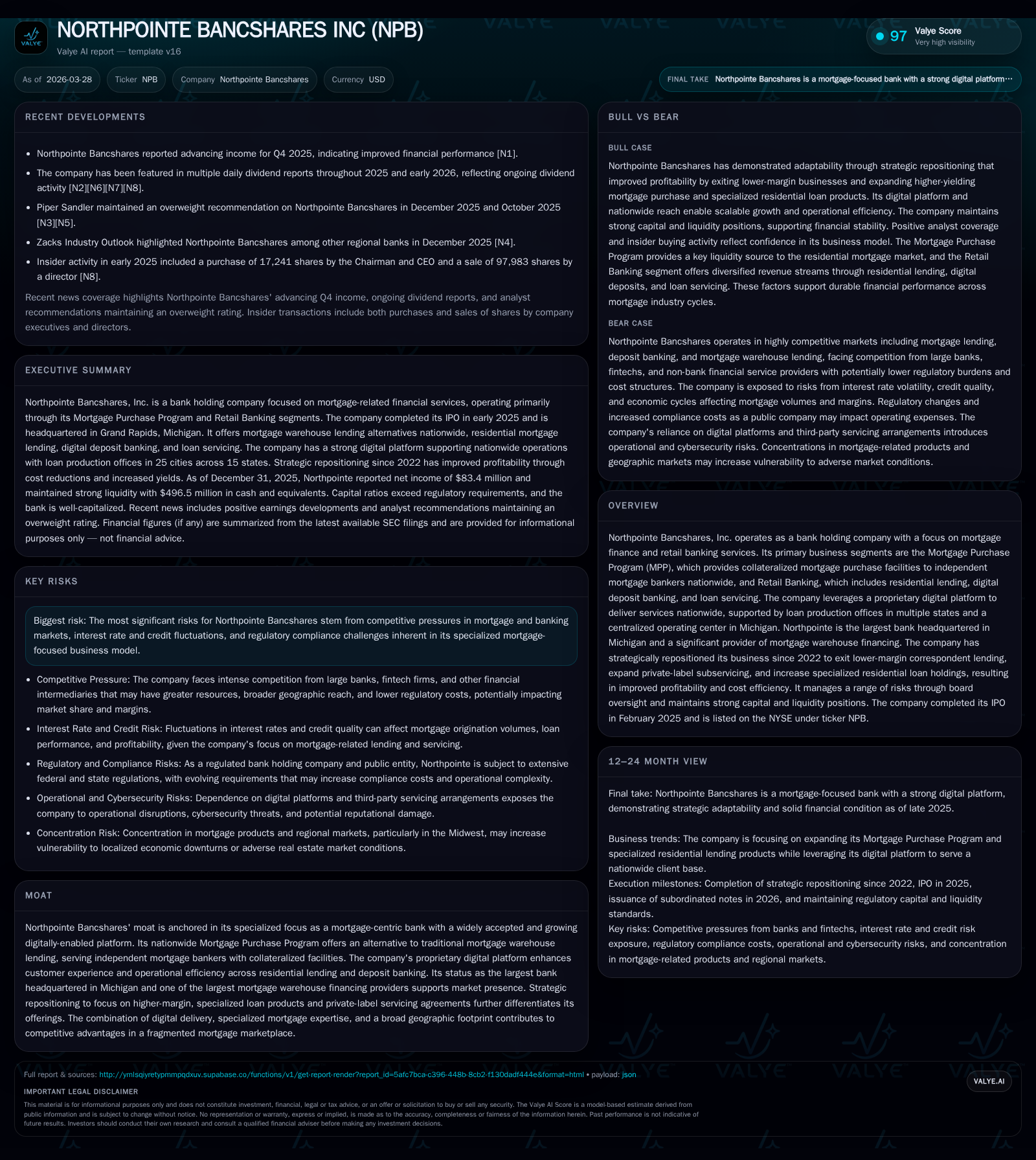

Northpointe Bancshares’ Transition Elevates Mortgage Specialty and Digital Reach

Northpointe Bancshares leverages its mortgage-centric banking model and proprietary digital platform to drive growth while navigating industry shifts and capital discipline.

Northpointe Bancshares, the largest bank headquartered in Michigan, has strategically reshaped its operations since 2022 by exiting low-margin correspondent lending and expanding its mortgage purchase facilities nationwide. The company’s digital-first approach supports scalable residential lending and deposit services alongside its Mortgage Purchase Program, which remains a core driver of volume and revenue growth. Financially, Northpointe posted over 50% net income growth in 2025 with disciplined capital management marked by a recent subordinated debt issuance and a consistent dividend policy. Looking ahead, performance hinges on evolving mortgage volumes, interest rate dynamics, regulatory conditions, and competitive pressures within the specialized mortgage finance sector.

Specialty Mortgage Bank with a Digital Backbone: Company Overview

Northpointe Bancshares operates as a focused mortgage-centric bank holding company headquartered in Grand Rapids, Michigan. Established primarily as a mortgage portfolio lender in the Midwest, it has expanded its footprint nationwide through a proprietary, digitized point-of-service lending platform that underpins both its retail residential lending and Mortgage Purchase Program (MPP). This platform enables efficient remote loan origination and servicing capabilities, combining digital convenience with access to experienced loan officers across its loan production offices in 25 cities spanning 15 states [S1][S18].

The Bank’s business model is distinctly specialized rather than broadly regional or full-service. It centers on two primary segments: the MPP that provides collateralized warehouse financing alternatives to independent mortgage bankers nationwide, and Retail Banking that delivers residential mortgages, including its All-in-One (AIO) loans—first-lien home equity lines tied to demand deposit sweep accounts—and digital deposit products managed primarily through one branch in Grand Rapids supported by centralized back-office operations [S1]. This specialization differentiates Northpointe among banks by focusing on mortgage finance while leveraging modern fintech delivery channels.

Historic Growth Catalysts and Financial Performance Trends

Northpointe has exhibited robust financial performance through recent cycles. For fiscal year ended December 31, 2025, net income reached $83.4 million—an increase of approximately 51.2% compared to $55.2 million in FY2024 [F1]. This substantial gain stems from accelerated growth of the MPP portfolio combined with enhanced yields on assets following strategic portfolio repricing.

Operating cash flow more than doubled to $44.3 million in FY2025 from $19.8 million the prior year, indicating effective conversion of revenues into liquid funds [F1]. Capex also rose significantly (+162.8% YoY) reflecting continued investments in technology infrastructure critical to supporting scalable digital platforms. Equity capital expanded by nearly 23% to $569 million [F1], facilitating growth without compromising regulatory capital buffers.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 83 | 44 | 3 | +51.2% |

| 2024 | 55 | 20 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 3 | 0 | 42 |

| 2024 | 3 | 770000 | 19 |

Source: SEC companyfacts cache [F1].

These metrics underscore Northpointe’s capability to scale operational leverage amid dynamic volume swings typical in mortgage banking cycles [F1][S1].

Strategic Repositioning: From Correspondent Lending Exit to Private-Label Subservicing

Starting in early 2022 and completing over approximately two years, Northpointe strategically shifted away from its historically lower-margin correspondent lending business due to tightening sector margins [S1]. This exit reduced exposure to cyclical volatility associated with correspondent channels.

Concurrently, the company expanded private-label subservicing agreements for conforming agency mortgages—a non-specialized product line that complements Northpointe’s specialized loan holdings while diversifying fee income streams. Furthermore, it enhanced residential lending focus on higher-yielding tailored products such as MPP-originated mortgages held on balance sheet [S1].

This realignment improved overall profitability by scaling higher-margin sources while pruning less profitable segments, demonstrating proactive portfolio repositioning consistent with evolving market conditions.

Mortgage Purchase Program (MPP): A Differentiated Growth Engine

The MPP remains central to Northpointe’s expansive footprint. Structurally an alternative collateralized warehouse facility targeting independent mortgage bankers nationwide, it underwrites short-duration loans typically held less than 30 days before sale to end investors [S6][S18].

This short dwell time limits exposure to interest rate risk relative to traditional longer-term warehouse lines, providing effective risk buffering amid fluctuating rate environments. Additionally, the unilateral right retained by Northpointe not to fund new MPP loans within contracts enhances liquidity flexibility [S6].

This segment grew meaningfully in scale during FY2025, as reflected by rising loan balances weighted heavily toward MPP exposure which constituted approximately 54% of total loans held for investment at year-end compared with roughly 37% a year prior [S22].

Integrated with the company’s digital platform, the MPP supports customer experience by streamlining facility access for independent originators competing against bank-affiliated lenders. This positions Northpointe competitively within the fragmented national mortgage origination ecosystem.

Capital Structure, Liquidity Management, and Returns Discipline

Capital adequacy metrics remain strong. Northpointe’s Bank entity reported total capital ratios well above regulatory minima at December 31, 2025—including total capital to risk-weighted assets at approximately 11.35%, Tier 1 capital ratio exceeding 11%, and leverage ratio above 8%—comfortably surpassing “well-capitalized” thresholds mandated by FDIC guidelines [S17][S19].

In March 2026, the holding company issued a $20 million subordinated note bearing a fixed-to-floating coupon starting at 7.50%, maturing in 2036, supporting strategic flexibility in capital deployment for general corporate purposes [S3].

Liquidity priorities favor holding cash and interest-bearing deposits over volatile securities positions, a deliberate choice reflecting risk prudence amid cyclicality of mortgage markets [S4][S6]. As of December 31, 2025, cash and equivalents totaled nearly $496 million against total assets exceeding $7 billion [F1][S22]. Borrowings include $1.42 billion in Federal Home Loan Bank advances plus an unsecured line of credit utilized selectively for liquidity management [S15]. Deposits rose sharply alongside balance sheet growth aided by competitive digital deposit offerings priced within top quartile industry rates nationally [S19][S26].

Return on equity was approximately 14.7% in FY2025 based on reported net income versus average equity levels —indicative of sound profitability backed by leveraged capital deployment without excessive risk concentration [F1]. Dividend payouts remain modest yet growing incrementally reflecting balanced shareholder returns alongside reinvestment priorities [$3.2 million dividends paid fiscal year ending December 2025] [F1][S4]. No share buybacks occurred during FY2025 following modest repurchases during FY2024.

Risks from Interest Rate Volatility and Credit Environment

Northpointe’s performance is inherently sensitive to fluctuations in interest rates wherein differential repricing timing between assets—dominated by floating-rate residential mortgages including the majority floating-rate AIO loans—and liabilities introduces net interest margin variability [S1][S20]. Although the relatively short life of MPP loans mitigates elongation risk, the company must carefully manage asset-liability duration gaps inherent in mortgage finance products.

Credit risks are concentrated within residential real estate portfolios including home equity lines with thorough risk grading systems guiding allowance for credit losses provisioning; however nonperforming assets grew moderately ($92.7 million vs $82 million prior year), albeit declining as a percentage of assets due to rapid portfolio expansion especially driven by MPP loans which have no nonperformers at reporting date [S14][S16]. Approximately one-third of nonperforming loans have government guarantees providing partial loss mitigation.

Competitive pressures arise both from traditional regional banks with broader product suites and from fintech entrants offering streamlined digital-first lending/ deposit alternatives potentially benefiting from lighter regulatory burdens or lower cost bases – challenging Northpointe’s position but also underscoring value provided by its niche specialization combined with proprietary technology focus [S20].[N/A] Operational risks related to the technology-driven model are addressed through mature cybersecurity governance overseen directly by senior management committees including a Cyber Security Oversight Council staffed by experienced professionals ensuring rapid threat identification and mitigation aligned with regulatory expectations [S1].

What to Monitor Forward: Pipeline, Regulatory Factors, and Market Share Dynamics

While explicit guidance is absent,[N/A] key indicators closely watched include:

- Volume trends secured through the Mortgage Purchase Program pipeline reflecting originator appetite against broader housing/mortgage cycle dynamics.

- Adoption rates of Northpointe’s proprietary digital platform both among retail borrowers and institutional partners underpinning scale efficiencies.

- Regulatory developments impacting capital requirements or compliance expectations particularly under Basel III frameworks affecting leverage or liquidity buffers.

- Competitive landscape shifts including fintech innovation trajectories that may alter customer acquisition costs or product pricing dynamics.

- Net interest margin impacts stemming from asset-liability repricing mismatch as monetary policy changes unfold.

- Credit quality trends amid macroeconomic pressures potentially influencing provisioning policies.

- Continued refinement of servicing strategies balancing in-house focus versus external subservicing partners enhancing fee diversification.

Continued execution against these vectors will determine Northpointe Bancshares’ capacity to solidify its differentiated stance as a digitally-enabled mortgage specialty bank poised for sustained earnings resilience despite industry uncertainties.

This analysis is based solely on publicly available information through March 28, 2026 ([F1], SEC filings S1-S29). It aims to provide an insightful overview without offering any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments