Bit Digital's Transformation: From Mining to AI-Driven Cloud Infrastructure

Bit Digital is shifting from its roots in digital asset mining to focus on high-performance computing infrastructure tailored to AI workloads, contending with financial losses amid expansion.

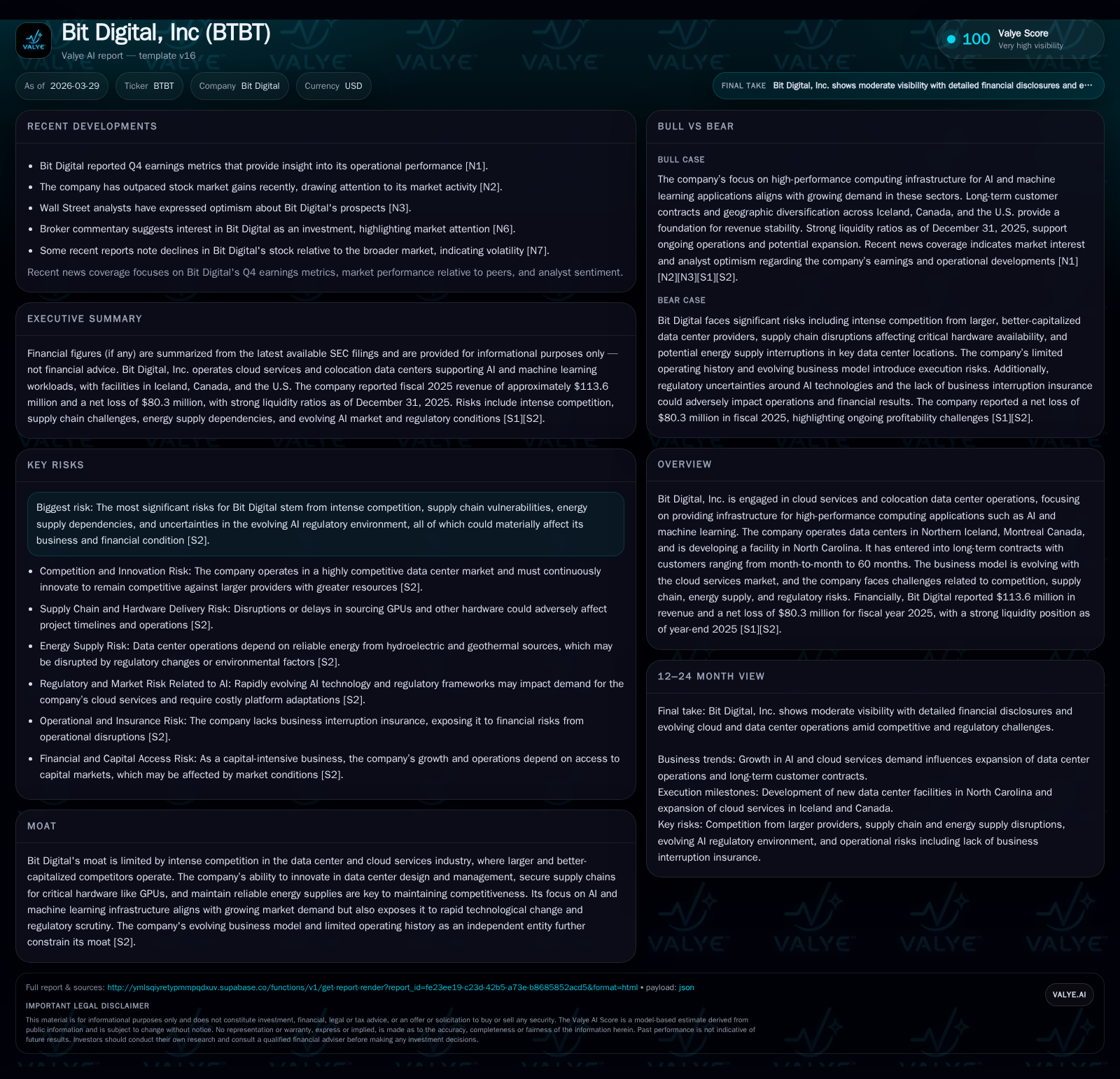

Bit Digital, Inc. has experienced modest revenue growth alongside significant net losses through 2025, reflecting its pivot from traditional crypto mining towards cloud services and high-performance computing aimed at AI and machine learning applications. The company has substantially increased capital expenditures to build out data center capacity while maintaining strong liquidity, but faces ongoing risks including intense competition, supply chain dependencies on GPU availability, and regulatory uncertainties in the evolving AI landscape. Contractual diversity and WhiteFiber’s IPO transition add complexity to revenue visibility and operational execution. Monitoring site ramp-ups, contract renewals, and regulatory developments will be crucial given the company’s limited historical profitability and evolving business model.

Financial Trajectory: Growth Amid Heavy Losses

Bit Digital’s fiscal results through 2025 illustrate a company in aggressive transformation mode. Revenue advanced slightly by 5.1% year-over-year to $113.6 million in FY2025 from $108.1 million in FY2024 [F1]. Despite this top-line growth, operating income swung deeply negative, eroding from a positive $27.6 million operating income in FY2024 to a loss of approximately $91.8 million in FY2025. Net income followed a similar pattern, deteriorating from profitable territory ($28.3 million in FY2024) into an $80.3 million net loss by year-end 2025 [F1].

This divergence signals that while Bit Digital's expansion efforts are lifting revenues—likely supported by increased exposure to high-performance computing (HPC) services—the cost base outpaced these gains substantially. Notably, FY2025 operating cash flow suffered a massive swing to a negative -$288.9 million compared to -$13 million the prior year, amplified by capex more than tripling year-over-year to nearly $286 million [F1]. This is consistent with heavy investment phases typical in data center buildouts transitioning core assets.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 114 | -80 | -289 | -92 | +5.1% | -383.7% |

| 2024 | 108 | 28 | -13 | 28 | +140.6% | +303.7% |

| 2023 | 45 | -14 | 1 | -17 | +86.8% | |

| 2022 | -105 | -8 | -107 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 800000 | -575 | -11.1 |

| 2024 | 1600000 | -107 | 6.1 |

| 2023 | 1600000 | -66 | -9.1 |

| 2022 | -28 | -117.1 |

Source: SEC companyfacts cache [F1].

Source: Company filings [F1]

Pivot to AI Infrastructure: Strategic Shifts and Market Position

Originally rooted as a digital asset mining operator, Bit Digital has strategically reoriented its business toward cloud services tailored for AI and machine learning workloads via its majority stake (~70.5%) in WhiteFiber Inc., which completed an IPO in August 2025 [S1][S2][S4]. The acquisition of Enovum Data Centers adds Canadian-based HPC infrastructure complementing facilities in Northern Iceland and plans for a U.S.-based site in North Carolina [S1].

The company's model now focuses on providing colocation services specializing in GPU-accelerated compute clusters—critical infrastructure underpinning large-scale AI model training and inference workloads [S4]. Contracts vary widely in duration from monthly terms up to five years, offering differentiated revenue stream stability [S4]. However, despite long-term contract anchors for parts of the customer base, the nascent industry dynamics create uncertainty regarding GPU longevity, rate structures, and technological evolution.

While this alignment with growing AI demand is logical given trends toward cloud-delivered HPC for machine learning developers, Bit Digital faces stiff competition from better-capitalized hyperscale cloud providers as well as specialized HPC operators [S2]. Their relatively limited operating history independent of parent integration constrains their ability to fully leverage scale or innovate at pace relative to incumbents.

Contract Structures and Revenue Visibility in Data Center Operations

WhiteFiber’s customer contracts span a broad range—from month-to-month flex arrangements enabling agile consumption of GPU compute resources up to contractual commitments lasting as long as five years [S4]. This variation reflects industry norms where enterprise clients may initially pilot AI workloads before committing long term.

Such contract diversity affects predictability; shorter terms expose the company to churn risk amid competitive pressure and pricing volatility for GPUs like NVIDIA's H100-series chips [S16][S17]. Meanwhile, longer contracts support base load revenues but necessitate accurate capacity forecasting—a challenge given fast-changing GPU technology cycles.

The limited operating track record of Bit Digital’s colocation data centers complicates profit outlooks since scalability hinges not just on customer acquisition but on maintaining optimized utilization of costly fixed-asset infrastructure [S4]. Accurate assessment of renewal rates and new project deployment cadence will be crucial for forecasting stability.

Capital Allocation Analysis: Capex Surge Versus Operating Cash Flows

The company's FY2025 capital expenditure surged over threefold compared with prior year—to roughly $286 million—as it accelerated buildout of HPC facilities including the North Carolina location slated for retrofit into high-capacity data center use [F1][S13][S18]. This capex increase corresponds with a dramatic deterioration in operating cash flow (-$289 million), underscoring intense cash burn during this investment phase.

Despite this heavy expenditure, Bit Digital maintains robust liquidity; its current ratio stood near 6.39 at year-end indicating significant current assets cushion relative to liabilities [F1][S13]. Such liquidity is critical given sector capital intensity and timing mismatches between upfront costs and client billing schedules.

Dividend payments were reduced by half from previous years ($0.8 million vs $1.6 million), signaling management’s prioritization of reinvestment over shareholder returns amid growth efforts [F1]. Share repurchases have been negligible since small amounts recorded in FY2022.

Risks from Supply Chain, Energy, and Regulatory Environment

Operational risks loom large for Bit Digital's emerging cloud infrastructure business:

- Supply Chain Vulnerabilities: Dependence on procurement of cutting-edge GPUs exposes timelines and costs to semiconductor availability disruptions or price inflation exacerbated by geopolitical tensions impacting supply chains spanning US, Canada, Mexico, China and Taiwan [S16][S17].

- Energy Supply Dependencies: Facilities located in Iceland benefit from stable renewable energy but also face climate-related weather event risks; new US data center operations must negotiate local energy sourcing which presents variability risk impacting cost structure [S23][S24].

- Regulatory Uncertainties: As AI technologies rapidly evolve amid increasing scrutiny globally—including nascent US federal/state regulations—there remains uncertainty about compliance costs or usage restrictions against customers' compute demands that could influence infrastructure uptake negatively [S8][S20]. Additionally, prior company history as China-based issuer surfaces residual legal exposures potentially affecting investor sentiment [S1][S2].

- Intellectual Property Litigation: Reliance on open source technologies combined with unpatented proprietary software exposes Bit Digital to infringement claims or forced reengineering potentially diverting resources amidst an already capital constrained environment [S10][S14][S21][S25].

Shareholder Returns: Dividend Policy and Repurchase History

Bit Digital’s dividends decreased notably—from approximately $1.6 million annually pre-FY2025 down to $0.8 million paid last fiscal year—reflecting the emphasis on funding expansion rather than returning capital during the capex-intensive stage [F1]. Share repurchases have been negligible for several years with no buybacks reported since small amounts recorded in FY2022.

This restrained distributions profile fits with an enterprise prioritizing growth investment over near-term cash return amidst substantial net losses.

Outlook and Key Milestones to Monitor in 2026

Although formal forward guidance remains absent post-IPO spinout of WhiteFiber, key milestones will shape BTBT's trajectory over coming quarters:

- Progression and commissioning timetables for the North Carolina data center retrofit represents a major capacity catalyst affecting total HPC footprint going forward [N4][N5][S13].

- Renewal rates and expansion among existing cloud service customers under staggered contract lengths will illuminate revenue stability and scaling feasibility.

- Performance results emerging from WhiteFiber as it transitions into standalone operations following IPO completion; ability to manage transition service agreements without disruption will materially affect financial outcomes [S11][S22].[N1]

- Evolving regulatory landscape surrounding AI infrastructure either accelerating adoption via clarity or constraining via restrictions may materially affect demand patterns.

- Continued volatility or shifts within Ethereum staking treasury strategies—which remain part of Bit Digital’s legacy exposure—constitute an additional element influencing overall corporate financial health despite focus pivot away from crypto mining itself [S2].[N6]

In summary, while the strategic reorientation toward AI-ready HPC infrastructure aligns with sector growth trends, Bit Digital faces critical execution challenges across contract management, capital efficiency, supply chain resiliency, technology risk mitigation, and regulatory compliance going forward.

Disclaimer: This report is prepared solely for informational purposes based on available public filings and news sources as referenced; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments