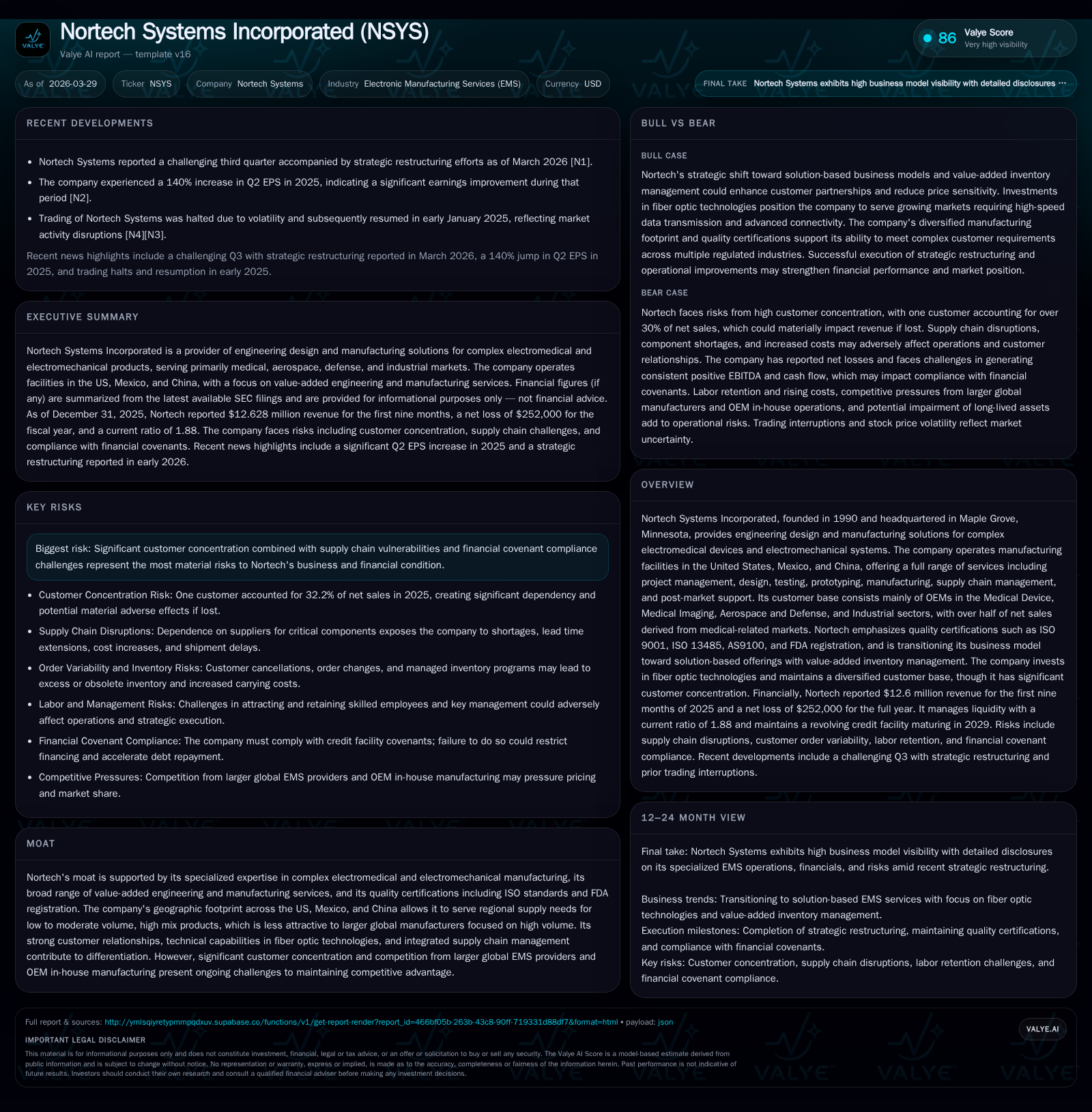

Nortech Systems Inc: Reshaping Electromechanical Manufacturing through Strategic Restructuring

Nortech Systems leverages its niche electro-medical manufacturing expertise and strategic restructuring to navigate recent financial setbacks and position for sustainable growth.

Founded in 1990, Nortech Systems Incorporated specializes in complex electromedical and electromechanical manufacturing with a focus on medical, aerospace, and industrial markets. After strong operating income levels in FY2022 and FY2023, the company faced significant profitability challenges in FY2024, prompting operational restructuring efforts reported in early 2026. Nortech is pivoting toward solution-based manufacturing models emphasizing customer inventory management and fiber optic technologies. While the company continues to benefit from industry certifications and regional manufacturing capabilities, risks from customer concentration, supply chain disruptions, and credit covenant compliance remain material. Monitoring liquidity metrics, execution of restructuring, and new program wins will be critical indicators going forward.

Legacy Growth Drivers and Financial Trends

Nortech Systems Inc., since its foundation in 1990, has carved out a specialized niche within the electronic manufacturing services (EMS) sector focusing on complex electromedical devices and electromechanical systems. The company's multi-facility footprint across the U.S., Mexico, and China equips it to handle high-mix/low-to-moderate volume production tailored for Medical Device, Aerospace & Defense, and Industrial OEM customers.

From FY2022 through FY2023, Nortech exhibited robust financial performance driven by the demand for specialized manufacturing services paired with value-added engineering support. Operating income was healthy at approximately $3.9 million in FY2022 before surging to over $5.9 million in FY2023 [F1]. This expansion was bolstered by leveraging their engineering design prowess and robust quality certifications (ISO 9001, ISO 13485, AS9100) enabling access to highly regulated medical device markets.

However, this momentum faltered sharply in FY2024 when operating income swung into a slight operating loss of $195K signaling acute margin pressures likely related to rising labor costs, supply chain bottlenecks especially around critical components for fiber optic technologies, and order timing volatility within their core medical segments [F1]. Net income mirrored this erosion dropping from nearly $6.9 million profit in FY2023 to a $1.29 million loss for FY2024.

In FY2025, Nortech initiated operational steps leading to a modest rebound—operating income recovered to $975K albeit net income remained slightly negative at -$252K reflecting continued underlying challenges [F1]. The gyrations highlight the cyclical nature tethered closely to OEM investment cycles as well as competitive pressures within their target EMS market which favors regional low volume providers like Nortech over large global high-volume manufacturers.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | 3 | 1 | 1 | +80.5% |

| 2024 | -1 | -2 | 0 | 1 | -118.8% |

| 2023 | 7 | 2 | 6 | 1 | +242.0% |

| 2022 | 2 | 5 | 4 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 2 | -0.7 |

| 2024 | -4 | -3.8 |

| 2023 | 0 | 19.4 |

| 2022 | 3 | 7.2 |

Source: SEC companyfacts cache [F1].

Note: Revenue is stable across last two years; operating income experienced wide swings indicating operational volatility.

Impact of Challenging Q3 and Strategic Restructuring Initiatives

Nortech’s Q3 results reflected ongoing pressures amplified by labor market tightness, supply chain interruptions particularly affecting fiber optic component sourcing critical to its advanced product offerings [N1]. In response to deteriorating margins and cash flow constraints evidenced by negative operating cash flow in the prior fiscal year [F1], management implemented strategic restructuring initiatives during late 2025 [S3]. These included workforce realignment targeting efficiency improvements while preserving key technical capacity; consolidation of certain production functions; and tightening inventory management programs.

These actions are framed against a backdrop of persistent inflationary cost environment across labor and materials as well as shifting customer order patterns requiring greater flexibility across production batches—a known challenge given Nortech’s focus on high mix/low volume runs which are less scalable than large batch production operated by global EMS providers [S4]. The restructuring aims not only address near-term cost structure but also align Nortech's manufacturing footprint with current demand realities while preparing for more integrated service delivery models emphasizing supplier-managed inventory programs [N1][S14].

Transitioning Business Model: From Commodity to Solution-Based Services

Nortech has been pivoting away from traditional transactional engagements based solely on discrete manufacturing orders toward delivering end-to-end solutions incorporating inventory management and supply chain integration customized for OEM clients [S4][S6]. This shift reflects broader EMS industry evolution wherein customers increasingly outsource not just production but ancillary operational activities such as procurement coordination and component stocking.

Distinctively for Nortech is its investment into fiber optic interconnect technologies aiming to capture emerging demand for lightweight high-bandwidth solutions imperative for medical imaging instruments and aerospace communications systems [S18]. These technical advances require sophisticated statistical process control methods given tight tolerances mandatory for optical cable assembly reliability—further setting Nortech apart from commodity EMS providers.

By integrating 'supplier-managed inventory' systems that allow real-time synchronization of stock levels with customer consumption rates coupled with proactive technical support during design-for-manufacturing phases [S6], Nortech elevates itself into a strategic partner role offering price stability and reduced time-to-market advantages versus purely price-driven contract manufacturers.

Market Positioning in Medical Device and Aerospace Sectors

The medical-related segment accounts for over half of Nortech's net sales underscoring its entrenched position within stringent regulatory frameworks demanding adherence to ISO 13485 standards plus multiple FDA registrations across U.S. operations [S12][S16]. Similarly important is its aerospace & defense segment where AS9100:D certification specifically certifies quality processes aligned with military-grade specifications essential for defense communication platforms [S12].

Such certifications create significant barriers to entry given the capital intensity of certification upkeep plus continuous quality audits involving installation qualification (IQ), operating qualification (OQ), and performance qualification (PQ) phases effectively validating every process step throughout production life cycle [S12]. These rigorous compliance demands limit credible suppliers capable of handling regulated electromechanical assemblies thus reinforcing Nortech’s moat around complex high-reliability product niches.

Supply Chain and Customer Concentration Risks

A material risk vector stems from customer concentration dynamics—one primary customer accounted for roughly one-third (32.2%) of total net sales in FY2025 up from about 27.7% a year earlier—which exposes Nortech materially to fluctuations or loss of this major client without immediate replacement alternatives available [S4][S8][S9].

This vulnerability intertwines with persistent supply chain headwinds: sourcing delays on electronic components especially semiconductors and specialty cables have forced emergency freight usage along with higher inventory buffer holdings inflating working capital demands [S9][S15]. While this strategy cushions customer fulfillment reliability amid volatile input lead times it constrains liquidity as excessive raw material stock ties up cash that could otherwise fund capex or debt service obligations.

Credit covenant compliance has required multiple amendments throughout recent quarters reflecting episodic EBITDA decline forcing leverage ratio waivers coupled with higher borrowing costs adding interest expense burden [S2][S24][S26]. Failure to meet these covenants without renewal or extension risks triggering loan acceleration detrimental to capital access [S7][S22].

Capital Allocation, Liquidity, and Returns Analysis

Despite recent top-line stability near $14.4 million USD reported revenues for recent periods [F1], returns have remained pressured—with a narrowly negative return on equity approximated at -0.7% given ongoing net losses relative to equity base (~$34.5 million end-2025) [F1]. This reflects lingering margin recovery hurdles amid restructuring.

Positive strides appear evident in operating cash flow restoration—from deeply negative ($-2.25 million) in FY2024 back into positive territory ($+2.74 million) by end-FY2025—facilitated by improved working capital management post restructuring alongside subdued capital expenditures ($661K down nearly half year-over-year) reflecting disciplined capex trimming given cash preservation priorities [F1]. This translated into an approximate free cash flow generation beyond $2 million bolstering liquidity buffers.

Buyback activity has essentially ceased since pre-2019 small-scale repurchases suggesting capital deployment preference towards internal restructuring investments rather than shareholder distributions during this turnaround phase [F1]. The new Associated Bank credit facility signed March 20th, 2026 replaces prior revolving credit lines extending maturity to March 2029 with defined borrowing base constraints tied mainly to eligible receivables and inventory assets—the latter being substantial given supply chain buffers—and fixed charge coverage covenants further underscoring lender vigilance over emerging cash flow metrics [S7][S26].

Outlook and Catalysts to Watch

Looking ahead no explicit revenue or profit guidance was published as of latest disclosures [N1][S3] indicating continued uncertainty around timing for full margin recovery. Key milestones investors should monitor include: effective execution timelines around stated restructuring programs measured via future quarterly operating income trajectories; developments easing component shortages enabling order visibility improvements; successful contract renewals or new customer wins especially within medical fiber optic solutions segments enhancing engineering backlog; plus maintenance of debt covenant compliance preventing liquidity shocks.

Additionally watching gross margin stabilizations reflective of transitioning away from purely commodity pricing toward integrated solution offerings will serve as critical proxy measures confirming business model evolution effectiveness [S4][N1]. Moreover given notable exposure outside U.S., any geopolitical shifts impacting tariff regimes or cross-border supply chains merit consideration given potential cost structure implications.

Disclaimer: This analysis is based solely on publicly available information as cited without any forward-looking projections beyond documented company disclosures or reported facts provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments