AmpliTech Group's Revenue Surge Highlights Challenges in Sustaining Profitability and Liquidity

AmpliTech's 165% revenue growth in 2025 contrasts with continued operating losses and liquidity pressures, underscoring execution and market risks.

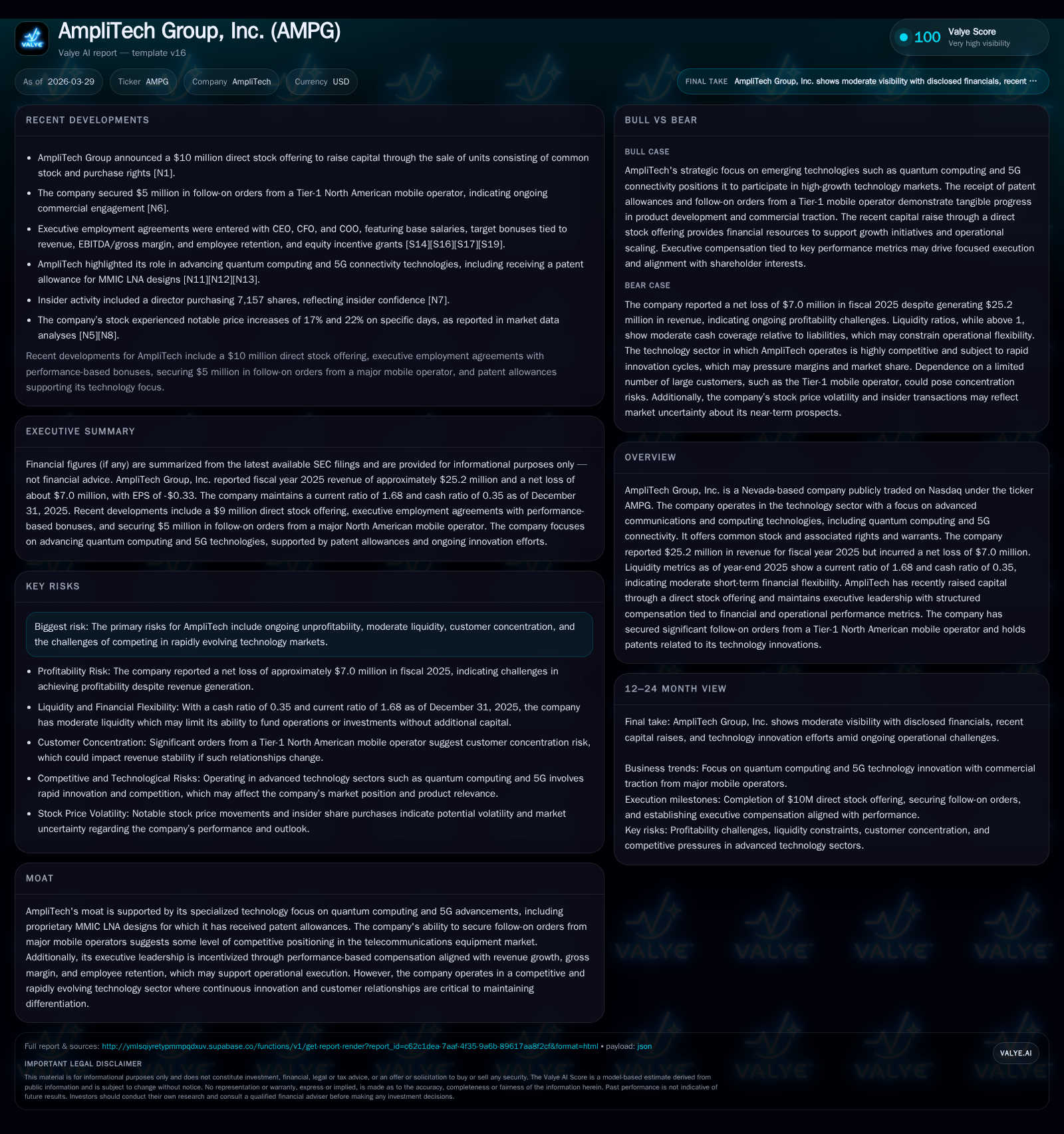

AmpliTech Group, Inc., a Nevada-based technology company focusing on advanced communications including quantum computing and 5G, reported $25.2 million in revenue for fiscal 2025, marking a substantial year-over-year increase of 165%. Despite this surge, the company remains unprofitable with a net loss of $7.0 million and operational cash flow challenges. Recent capital raises, including a $9 million direct stock offering, provide near-term liquidity but underscore ongoing funding needs. Key growth catalysts include follow-on orders from a major North American mobile operator and anticipated benefits from an asset purchase agreement; however, customer concentration and execution risks temper outlook clarity.

Company Overview and Business Segments

AmpliTech Group, Inc., incorporated in Nevada since 2010, specializes in advanced communications components with emphasis on RF amplifiers tailored for satellite communications (SATCOM), telecom (notably 5G and IoT), space defense applications, and emerging quantum computing markets [S1]. Its divisions include Specialty Microwave producing precision microwave components; Spectrum Semiconductor Materials distributing IC packaging acquired in late 2021; the AmpliTech Group MMIC Design Center (AGMDC) focused on monolithic microwave integrated circuit chip design; and True G Speed Services promoting Open RAN compliant 5G systems integrating proprietary low noise amplifiers [S1].

Products span low noise amplifiers (LNA), medium power amplifiers, cryogenic amplifiers, and custom assemblies across frequencies ranging from 50 kHz to 44 GHz — critical for high-frequency signal applications.

Historical Financial Performance

AmpliTech demonstrated significant revenue growth over recent years but continues to report operating losses due to ongoing investments in R&D and scaling operations. The table below summarizes key financial metrics:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 25 | -7 | -9 | -7 | +165.0% | +37.7% |

| 2024 | 10 | -11 | -5 | -8 | -39.0% | -356.0% |

| 2023 | 16 | -2 | -3 | -3 | -19.6% | -264.1% |

| 2022 | 19 | -1 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -10 | -21.3 |

| 2024 | -5 | -30.0 |

| 2023 | -4 | -9.2 |

| 2022 | -2.4 |

Source: SEC companyfacts cache [F1].

Key points:

- Revenue surged by approximately 165% from FY2024 to FY2025 driven by expanded orders related to core LNA and emerging product lines.

- Operating losses narrowed modestly by about 13%, reflecting scale efficiencies but continued investment drag.

- Net losses declined significantly though profitability remains elusive.

- Operating cash flow worsened due to working capital shifts and increased investment activity.

- Capital expenditures increased sharply supporting expansion initiatives like the MMIC design center [F1].

Growth Drivers and Risks

Growth Catalysts

Growth depends on commercialization of advanced RF amplifier technologies for expanding markets including Open RAN-based 5G networks, satellite communication upgrades requiring high-performance LNAs at GHz frequencies, quantum computing needing cryogenic amplification solutions, and IoT devices demanding miniaturized MMIC implementations.

Notably:

- Funded purchase orders totaling approximately $5 million were received starting late December 2025 from a Tier-1 North American mobile operator with shipments expected through Q2 2026 [S1].

- The March 2025 Titan Asset Purchase Agreement could enable intellectual property transfer fueling innovation pipelines though milestone achievement is uncertain [S1].

- A non-binding letter of intent for $78 million of O-RAN radios indicates potential large-scale contracts subject to finalization [S1].

Risk Factors

Risks include:

- Persistent unprofitability with an accumulated deficit exceeding $28 million reflecting sustained losses from investments.

- Liquidity constraints despite recent equity raises leave execution dependent on funding availability.

- Customer concentration risk given reliance on major operators.

- Potential order cancellations or delays impacting revenue predictability.

- Competitive pressures within fast-evolving technology sectors requiring consistent innovation outputs [S18][S1].

Liquidity and Capital Structure

As of December 31, 2025:

- Cash and equivalents stood at approximately $4.98 million.

- Current assets totaled about $25.06 million against current liabilities near $14.9 million yielding a current ratio around 1.68.

- The cash ratio was about 0.35 indicating limited pure cash reserves relative to short-term obligations [F1].

Recent financing activity includes:

- A registered direct offering closed January 27, 2026 raising gross proceeds exceeding $9 million before fees through issuance of approximately 2.23 million units each comprising common stock plus Series A & B rights exercisable into additional shares at premiums ($5/$6 strike prices) enhancing capital flexibility [N1][S16][S19].

No dividends or share buybacks are currently planned aligning with reinvestment priorities amid negative free cash flow nearing almost $9.7 million when accounting for operating cash flow less capex during fiscal year end [F1][S9][S20].

Executive Compensation Alignment

Management bonuses are tied to annual revenue targets, gross margin/EBITDA improvements, and employee retention metrics designed to align executive incentives with operational performance objectives [S13]. CEO target bonuses can reach up to significant portions of base salary contingent on performance milestones. Equity awards including stock options vesting over time plus immediate restricted stock unit grants further incentivize shareholder value creation alignment [S18][S22].

Outlook Considerations

Formal guidance is not publicly disclosed beyond anticipated milestones:

- Completion of initial funded orders through Q2 CY26.

- Achievement of Titan APA milestones expected mid-2026 remains uncertain. Monitoring will focus on backlog conversion from funded orders, milestone attainment under the asset purchase agreement, and diversification efforts to mitigate customer concentration risks across aerospace/defense/satellite/telecom verticals. Cash burn stabilization balanced against equity raises will be critical for sustaining operations.

Emerging telecommunications architectures like Open RAN paired with nascent quantum computing hardware needs represent sizable opportunities if execution risks are managed effectively.

This analysis is based exclusively on publicly available information up to March-April of fiscal year ending December 31st, 2025 as filed or disclosed by AmpliTech Group Inc., supplemented by news through early Q12026 without any investment advice or price forecasts implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments