Gain Therapeutics’ Proprietary Platform Spurs Clinical Progress and Capital Challenges

Gain Therapeutics harnesses its Magellan™ platform for novel protein misfolding therapeutics while managing substantial operating losses and near-term funding needs.

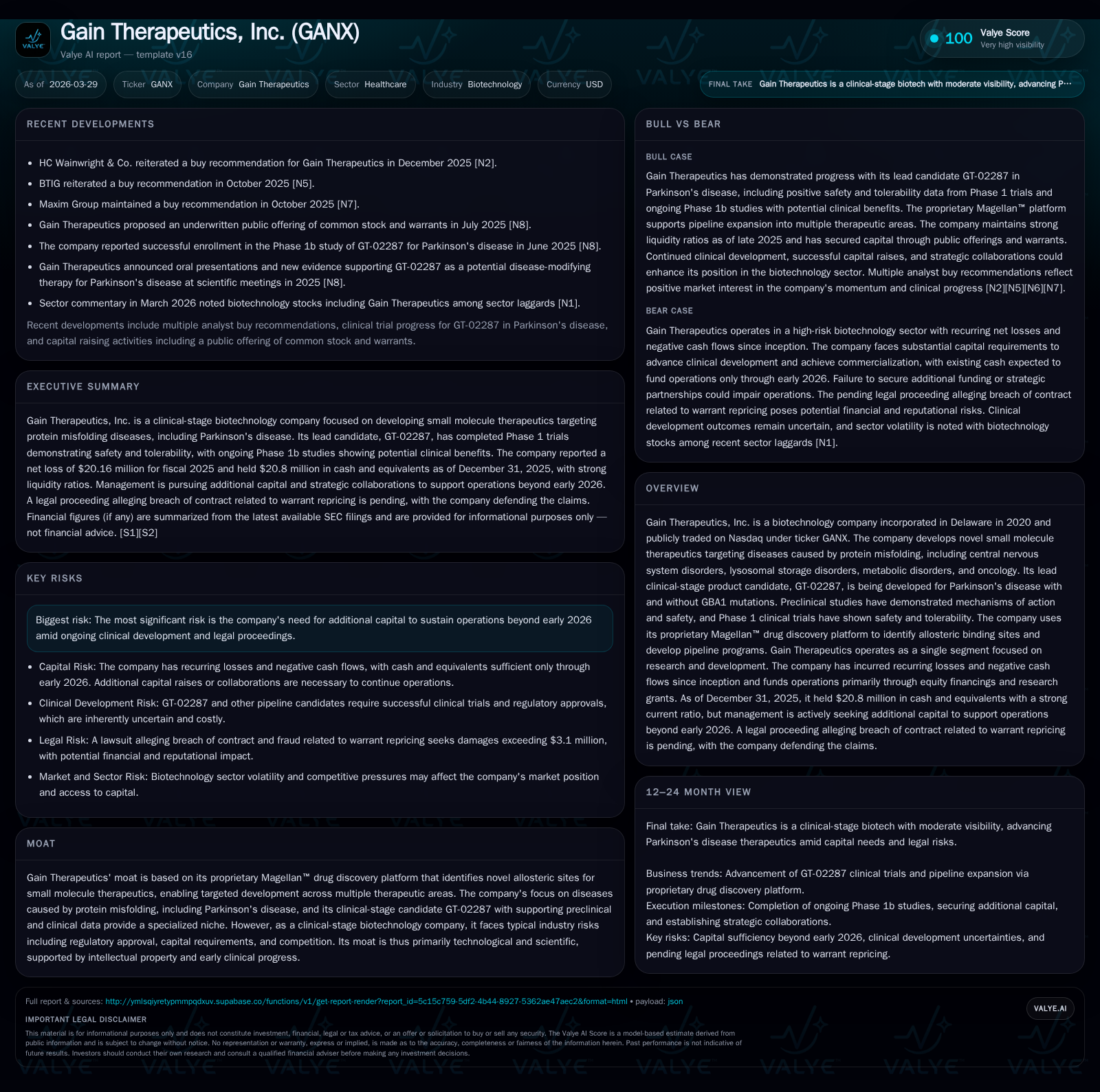

Gain Therapeutics, a clinical-stage biotech focused on small molecule therapeutics targeting protein misfolding diseases, advances its lead Parkinson’s candidate GT-02287 with positive Phase 1 safety data. The company leverages its proprietary Magellan™ drug discovery platform to identify novel allosteric sites critical for pipeline development. Despite scientific progress, Gain faces sustained negative operating profitability and cash flows, with a cash burn necessitating additional capital to fund operations beyond early 2026. Litigation risks related to warrant repricing claims add uncertainty to its financing outlook. Monitoring clinical milestones and partnership developments is essential to assess progress amid these financial constraints.

Historic Financial Trends: Operating Losses Amid Early-Stage Innovation

Gain Therapeutics exhibits typical clinical-stage biotech financials: minimal revenues paired with significant operating losses driven by research and development investments. Revenue remained unchanged at $55,180 for both FY2023 and FY2024, underscoring the absence of commercial products or sales [F1]. Operating losses improved modestly from approximately -$20.4 million in FY2024 to -$18.7 million in FY2025, an 8.1% reduction, though losses remain considerable [F1]. Net income followed a similar pattern with persistent losses around -$20 million annually.

Operating cash flow outflows slightly improved from -$18.87 million in FY2024 to -$18.47 million in FY2025, consistent with ongoing investment in clinical programs and platform development [F1]. This sustained negative cash flow highlights dependence on external funding.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -20 | -18 | -19 | +1.2% | ||

| 2024 | 55180 | -20 | -19 | -20 | 0.0% | +8.3% |

| 2023 | 55180 | -22 | -19 | -22 | -60.6% | -26.6% |

| 2022 | 140108 | -18 | -15 | -18 | -15.1% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -108.6 |

| 2024 | -278.1 |

| 2023 | -177.0 |

| 2022 | -93.2 |

Source: SEC companyfacts cache [F1].

Flat revenue reflects Gain’s developmental stage without marketed products; the ongoing net losses emphasize the need for prudent capital management pending potential commercialization.

Magellan™ Platform as a Differentiator in Small Molecule Drug Discovery

Central to Gain Therapeutics’ innovation is its proprietary Magellan™ platform designed to identify novel allosteric binding sites—non-active regulatory pockets on proteins that modulate function when targeted by small molecules [S1]. This structure-guided approach targets diseases caused by protein misfolding such as central nervous system disorders including Parkinson’s disease.

Allosteric modulation offers potential advantages like increased selectivity and favorable safety profiles compared to traditional active-site targeting strategies. By exploiting these regulatory sites identified through Magellan™, Gain aims to establish a technological moat differentiating its pipeline across therapeutic areas including lysosomal storage disorders and oncology beyond CNS indications [S1].

Magellan™ also accelerates discovery timelines via computational simulations of structural dynamics—advancing beyond conventional screening methods common in small molecule research.

Lead Candidate GT-02287: Progress and Clinical Viability in Parkinson’s Disease

Gain’s lead candidate GT-02287 addresses glucocerebrosidase (GCase) dysfunction implicated in Parkinson’s disease—including forms associated with GBA1 mutations that impair lysosomal enzyme activity [S1]. Preclinical data demonstrate restoration of GCase function within lysosomes, reduction of toxic lipid substrates and alpha-synuclein aggregates linked to neurodegeneration, decreased endoplasmic reticulum stress markers, improved mitochondrial health, enhanced dopaminergic neuron survival, and normalization of biomarkers such as neurofilament light chain (NfL).

In a Phase 1 first-in-human trial involving seventy-two participants across escalating doses, GT-02287 showed favorable safety and tolerability without dose-limiting toxicities—clearing an important regulatory milestone enabling further patient-focused studies [S1]. Early Phase 1b results presented at an international neurology congress aligned with prior findings.

These data position GT-02287 within neurodegenerative disease R&D aiming at modifying underlying pathology rather than symptomatic treatment alone—a highly competitive but scientifically promising arena.

Capital Structure Dynamics and Liquidity: Navigating Funding Needs Through 2026

Despite recent capital raises increasing liquidity—with cash and equivalents reported at approximately $20.8 million at fiscal year-end 2025—Gain faces pressing funding requirements extending into early 2026 [F1]. The company held a strong current ratio near 6.6x due to limited current liabilities ($3.35 million) relative to current assets ($22.2 million) at year-end [F1], signaling short-term solvency.

Nonetheless, operational burn rates exceed available resources given quarterly cash outflows primarily tied to R&D activities without offsetting revenues. Management is actively reviewing organizational costs aiming to streamline expenditures while maintaining innovation momentum; it also pursues licensing agreements or strategic collaborations as alternative capital sources beyond equity markets [S4][S23][S26].

This liquidity challenge coincides with legal uncertainties from litigation initiated January 2026 concerning alleged warrant repricing agreements seeking damages over $3.1 million—introducing additional financial risk pending resolution [S1][S14].

The company remains reliant on equity issuances or convertible debt financings timed before existing funds are depleted , highlighting typical early-stage biotech capital market vulnerabilities.

R&D Spending Profile and Cost Optimization Efforts

Research & development expenses encompass scientific personnel costs, preclinical studies including contract manufacturing for trials, intellectual property legal fees expensed as incurred rather than capitalized, plus software amortization supporting the drug discovery platform [S23][S26][F1].

While line-item granularity is limited in filings reviewed here, overall operating expenses reflect pipeline advancement consistent with clinical phase transitions; management emphasizes balancing robust R&D investment against cost discipline through organizational adjustments designed to reduce operating leverage without compromising scientific progress—a critical equilibrium prior to commercialization capability [S2][S23][F1].

Maintaining strong R&D intensity remains essential for advancing candidates like GT-02287 while preserving financial sustainability amid finite capital runway projected into early next year absent new funding.

Key Risks Including Ongoing Litigation and Financing Uncertainty

Key risks include the urgent need for additional funding beyond early 2026 due to persistent cash burn inherent in clinical development alongside lack of revenues—exacerbated by ongoing litigation alleging breach of contract and fraud related to warrant repricing agreements claiming damages exceeding $3.1 million plus related costs [S13][S14].

Such legal challenges create operational uncertainties potentially impacting investor sentiment or imposing contingent liabilities if judgments are adverse. Management has stated intent to vigorously defend itself while concurrently engaging multiple funding avenues—including equity placements or strategic partnerships—to support continuing operations beyond imminent liquidity deadlines [S14].

These factors heighten typical sector risks characteristic of early-stage biotechs where outcomes hinge on successful trials balanced against limited financial resources.

Future Milestones to Monitor: Clinical Readouts and Strategic Partnerships

Though specific timing for pivotal clinical trial readouts or partnership deals remains undisclosed publicly through latest filings reviewed here, key value inflection points include Phase 2 efficacy data for GT-02287 in Parkinson’s patients and potential expansion into broader neurodegenerative or other indications leveraging Magellan™ platform discoveries [N1][S3].

Additionally,the search for strategic collaborations or licensing arrangements may provide non-dilutive funding sources plus validation endorsements enhancing credibility within pharmaceutical ecosystems—a relevant catalyst given current liquidity constraints.

Updates on litigation proceedings affecting stockholder value prospects should also be closely monitored.

Valuation Considerations and ROE Analysis for a Clinical-Stage Biotech

From an asset return perspective Gain Therapeutics displays deeply negative return on equity around -108%, calculated using latest annual net loss divided by shareholder equity—typical for biopharma firms investing heavily in R&D prior to product commercialization [F1]. This reflects an investment phase prioritizing pipeline maturation over profitability common within this sector.

Given negligible revenues so far, valuation largely derives from technological promise embedded within the Magellan™ platform combined with clinical progression rather than earnings multiples applicable for mature companies.

Disclaimer:

This analysis is based solely on publicly filed financial data and corporate disclosures as of March 29, 2026. It does not constitute investment advice or recommendations regarding any securities. Outcomes depend materially on future clinical trial results, regulatory approvals, capital market conditions, and other risk factors detailed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments