Acumen Pharmaceuticals' Clinical-Stage Focus on Sabirnetug Propels Growth Amid Persistent Losses

Developing a novel Alzheimer’s treatment targeting soluble amyloid-beta oligomers, Acumen advances toward Phase 2 results with funding secured through early 2027.

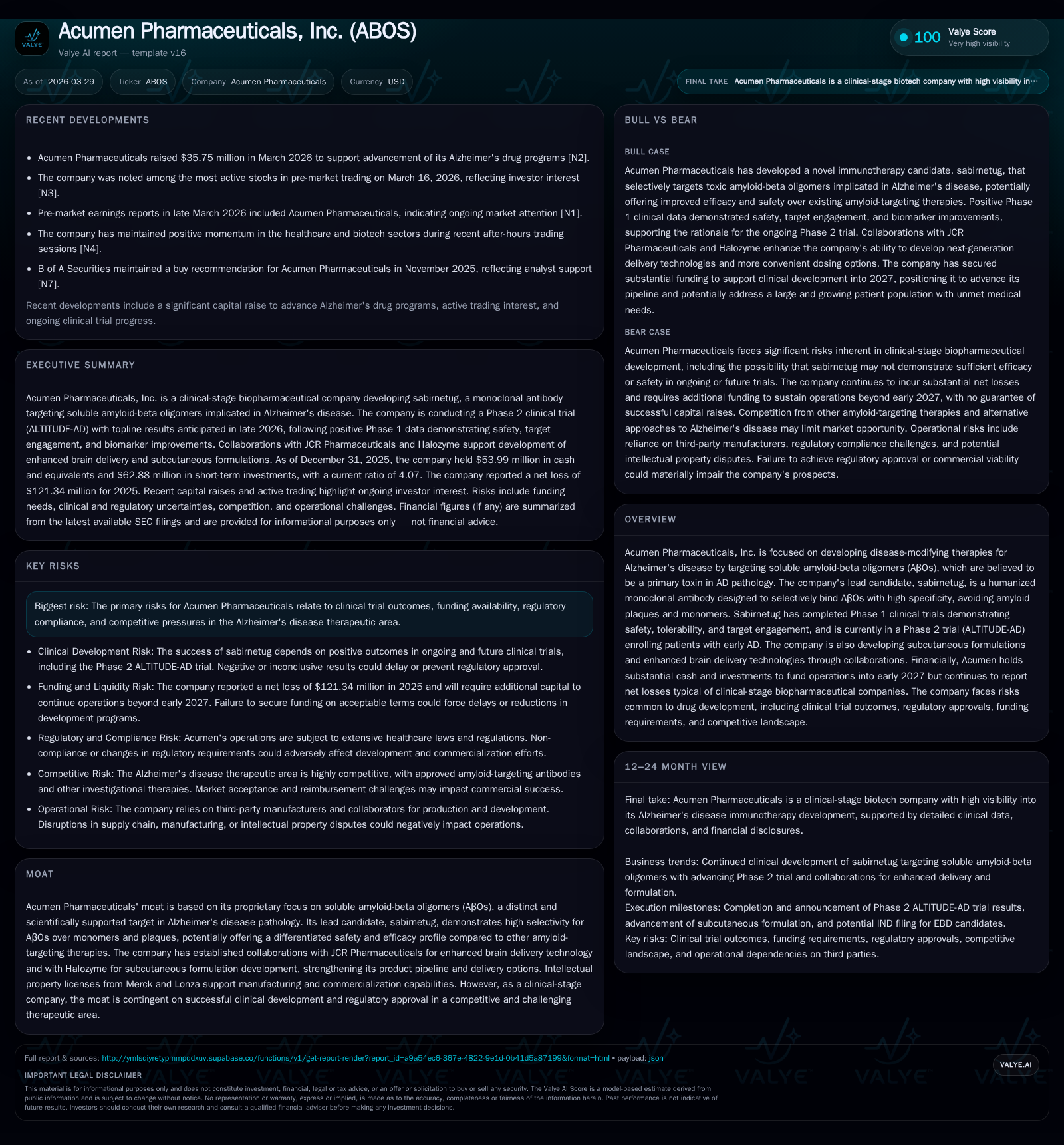

Acumen Pharmaceuticals is advancing sabirnetug, a selective monoclonal antibody targeting soluble amyloid-beta oligomers, as a potentially differentiated approach to Alzheimer's disease. Since its institutional fundraising began in 2018, the company has incurred steady operating losses typical of clinical-stage biopharmas but maintains ample liquidity to fund operations into early 2027. Its lead Phase 2 trial (ALTITUDE-AD) enrolls patients with early Alzheimer’s, with top-line results expected by late 2026. Strategic collaborations aim to enhance delivery and administration, though commercialization remains contingent on clinical success and regulatory approvals in a challenging therapeutic area.

Company Overview and Scientific Rationale

Acumen Pharmaceuticals operates as a clinical-stage biopharmaceutical entity pioneering a focused immunotherapy for Alzheimer’s disease (AD) built around the underexplored but scientifically compelling target: soluble amyloid-beta oligomers (AβOs). These oligomers represent globular assemblies of the amyloid-beta peptide believed increasingly to be principal neurotoxins driving the initiation and progression of AD pathology, distinct from traditional targets like insoluble plaques or monomeric forms.

Founded in 1996 with research licensed exclusively from Merck & Co., Acumen reenergized operations post-2018 capital raises to develop sabirnetug (ACU193), a humanized IgG2 monoclonal antibody. This molecule was crafted for high affinity and selectivity toward AβOs while sparing plaques and monomers—potentially refining therapeutic window and safety profiles relative to prior amyloid-targeting antibodies [S1].

Historical Performance and Development Milestones

Acumen's clinical development initiated in mid-2021 with Phase 1 trials (INTERCEPT-AD) evaluating sabirnetug's safety, tolerability, pharmacokinetics, pharmacodynamics, and target engagement in early AD patients. Enrollment completed by early 2023 with topline data announced mid-year confirming safety and target engagement [S1].

The pivotal Phase 2 ALTITUDE-AD trial launched in May 2024 is a randomized, double-blind placebo-controlled study across approximately 540 subjects with mild cognitive impairment or mild dementia due to AD. Two intravenous doses—35 mg/kg and 50 mg/kg every four weeks—were selected based on prior modeling. Enrollment finished by March 2025; topline results are expected late 2026 [S1], [N3].

Parallel efforts include alternative delivery mechanisms via collaborations targeting subcutaneous formulations with Halozyme (Phase completion mid-2024) and enhanced blood-brain barrier penetration technologies partnered with JCR Pharmaceuticals since July 2025 [S1]. These aim to broaden clinical convenience and improve therapeutic profiles.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -121 | -116 | -124 | 88000 | -18.6% |

| 2024 | -102 | -86 | -114 | 16000 | -95.4% |

| 2023 | -52 | -43 | -61 | 21000 | -22.2% |

| 2022 | -43 | -35 | -45 | 161000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -116 | -172.3 |

| 2024 | -86 | -56.3 |

| 2023 | -43 | -19.6 |

| 2022 | -35 | -22.7 |

Source: SEC companyfacts cache [F1].

Table: Acumen Pharmaceuticals Annual Financial Summary [F1]

Financially, the company remains unprofitable as typical for clinical-stage biopharma. Operating losses increased from approximately $45 million in FY22 to nearly $124 million in FY25 due mainly to escalating R&D expenditures supporting multiple clinical programs. Net losses deepened similarly; operating cash flow remained negative at roughly $116 million for FY25 minus modest capital expenditures.

Cash and equivalents totaled about $54 million at year-end December 31, 2025 [F1], supporting operations into early next year. A recent equity financing raised $35.75 million in March 2026 further bolsters capital availability for continued development [N3], [S10], [S11]. The accumulated deficit reached $446.5 million by end-2025 reflecting ongoing investment without product revenues.

Forward Growth Prospects

The near-term value driver will be successful completion of ALTITUDE-AD Phase 2 data anticipated late calendar year 2026 [S1], [N1]. Positive efficacy signals could materially impact valuation given limited current options specifically targeting AβOs.

Additional growth opportunities reside in innovations around administration routes—subcutaneous dosing reducing patient burden—and proprietary brain delivery technologies aiming to enhance pharmacodynamics through improved blood-brain barrier penetration [S1]. Collaborations with JCR Pharmaceuticals and Halozyme underline strategic pipeline diversification that mitigates limitations of IV-only dosing.

However, expansion potential remains constrained by Alzheimer's field challenges: historically high clinical trial failure rates due to complex pathophysiology; regulatory hurdles including stringent FDA scrutiny; growing payer resistance demanding cost-effectiveness; and intense competition from both biopharma incumbents and newer modalities.

Upcoming Milestones

Key upcoming catalysts include the projected release of Phase 2 ALTITUDE-AD topline results expected late calendar year 2026 [S1], [N1]. These data will assess sabirnetug’s efficacy leveraging integrated outcome measures after approximately eighteen months of treatment.

The company has not yet initiated pivotal Phase 3 studies or commercial preparation pending Phase 2 outcomes [S1]. Revenue generation is not anticipated until regulatory approval is secured.

Additional milestones may arise from ongoing formulation development progress alongside regulatory interactions concerning breakthrough therapy designation or accelerated pathways if preliminary evidence supports such approaches [S18].

Capital Allocation and Returns

As a pre-revenue development-stage company focused fully on advancing its drug candidate pipeline through clinical stages, Acumen shows characteristic negative operating cash flows intensifying annually due to escalating R&D activities. No dividends or share repurchases have been declared or executed as all capital is directed toward drug development progression [F1].

Shareholders’ equity declined markedly from prior years reflecting accumulated losses absorbing capital despite recent financing efforts aimed at extending operational runway beyond immediate availability [F1], [N3]. The current ratio stood above four at year-end indicating sufficient short-term liquidity for operational payables but continued reliance on external funding persists [F1].

With net income deeply negative relative to shareholders’ equity ($70 million equity versus $121 million net loss for FY25), return metrics such as ROE are strongly negative (~-172%) consistent with developmental stage biotech characteristics focused on capital consumption rather than profit generation [F1].

Industry Context and Strategic Positioning Analysis

The Alzheimer’s drug sector is highly specialized with immense scientific complexity compounded by decades-long failures predominantly targeting amyloid plaques yielding marginal benefits often paired with adverse events related to off-target effects. Acumen’s focus on soluble Aβ oligomers aligns well with emerging scientific consensus identifying these oligomers as key neurotoxic species driving synaptic dysfunction.

Few competitors target AβOs selectively with an approach comparable to sabirnetug’s specificity and safety profile ambitions. This confers differentiation but hinges critically on positive demonstration of clinical benefit where many have historically failed.

Risks persist including regulatory approvals beyond safety considerations; payer skepticism about cost-effectiveness; reimbursement challenges especially if biomarker surrogates lack clear clinical translation; intellectual property enforcement complexities given licensed technology origins; and compliance costs related to healthcare regulations covering promotion and distribution practices [S4]-[S29].

Risk Profile Summary

Primary risks include:

- Clinical trial outcome uncertainty affecting program viability;

- Ongoing financing needs amid persistent cash burn;

- Regulatory compliance demands spanning pre-approval through post-marketing phases;

- Competitive pressures requiring rapid innovation;

- Intellectual property litigation risks impacting commercialization;

- Evolving healthcare reimbursement environment influencing pricing dynamics nationally and internationally.

Conclusion Notes for Monitoring

Investors should watch closely:

- Timing and content of ALTITUDE-AD topline results expected by end-2026;

- Progress toward regulatory designations such as breakthrough therapy status;

- Capital raise execution extending operational runway beyond current levels;

- Developments in partnerships enhancing delivery platforms (JCR/Halozyme);

- Competitive landscape shifts affecting therapeutic standards;

- Regulatory environment changes impacting biologic approval pathways.

Acumen represents a high-risk/high-reward clinical-stage biopharmaceutical company pursuing an innovative strategy centered on novel biological targets within an immense global disease burden awaiting critical data readouts that will shape its future trajectory.

Disclaimer: This analysis summarizes publicly available information up to March 29th, 2026 without providing investment advice or recommendations. Readers should conduct comprehensive due diligence before making financial decisions involving Acumen Pharmaceuticals or peer entities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments