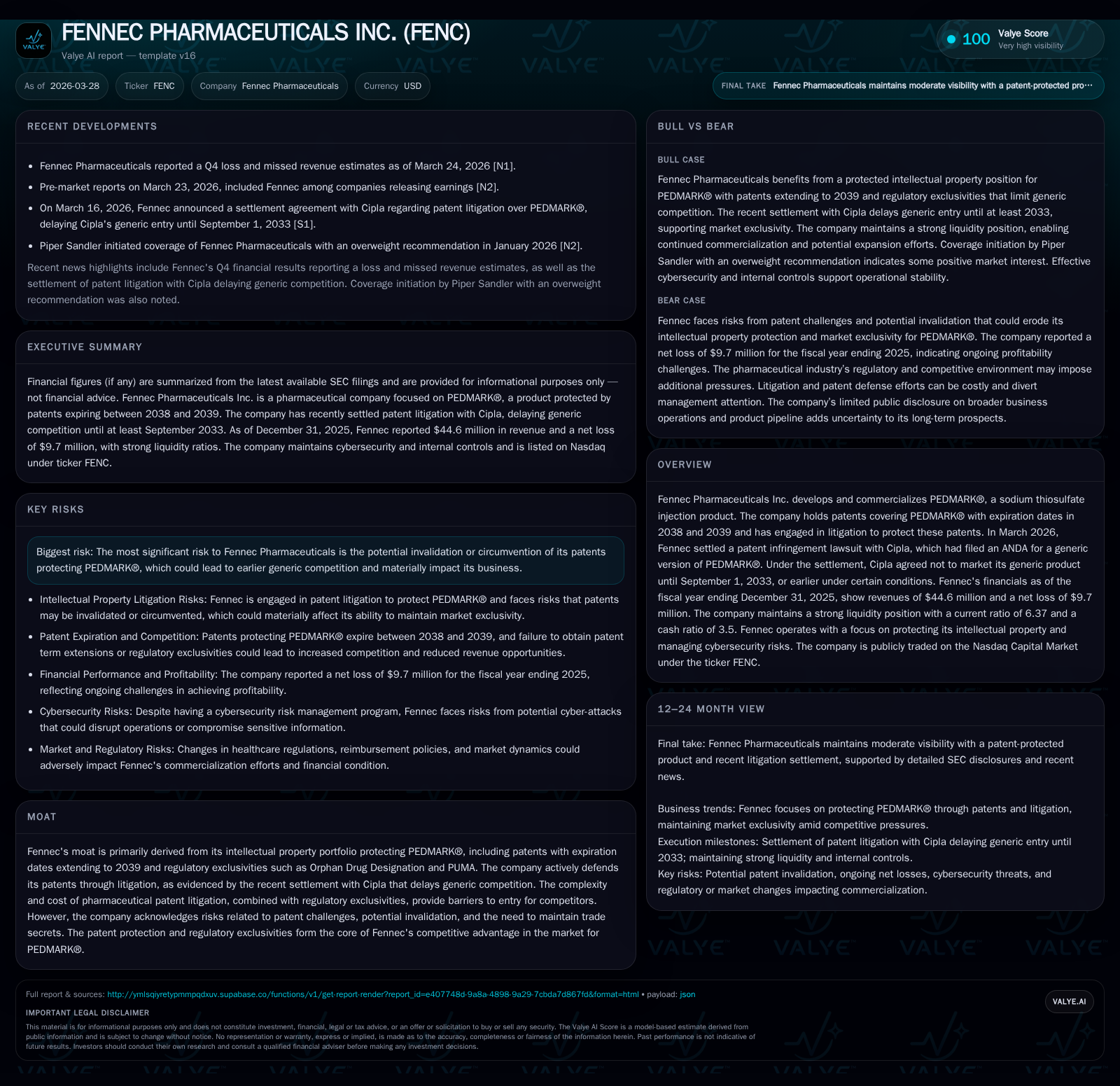

Fennec Pharmaceuticals’ Patent Settlement with Cipla Extends PEDMARK® Exclusivity to 2033 Amid Profitability Challenges

Fennec Pharmaceuticals secured a patent litigation settlement delaying generic entry but faces operational losses and cash flow deficits.

Fennec Pharmaceuticals Inc. develops and commercializes PEDMARK®, protected by patents expiring in 2038-2039. In March 2026, it settled patent infringement litigation with Cipla, postponing generic competition until at least September 2033. Despite continued revenue growth since 2021, Fennec remains unprofitable with a net loss of $9.7 million in FY2025 and operating cash flow deficit of $12.5 million. The company’s moat relies heavily on its patent portfolio and regulatory exclusivities, but ongoing risks from patent challenges and healthcare pricing pressures persist. Monitoring future patent defenses, commercialization progress outside the U.S., and cash burn will be critical for assessing its trajectory.

Company Overview

Fennec Pharmaceuticals Inc. is a pharmaceutical company specializing in the development and commercialization of PEDMARK®, a proprietary sodium thiosulfate injection intended to prevent ototoxicity caused by cisplatin chemotherapy. The product benefits from a robust intellectual property portfolio featuring U.S. patents expiring in January 2038 (US ‘190 patent) and July 2039 (US ‘728 patent), supplemented by orphan drug designation and pediatric exclusivity (PUMA), which collectively create substantial market protection [S1].

In recent years, Fennec has focused on defending these IP rights vigorously during generic challenges. A notable development occurred in March 2026 when Fennec settled ongoing patent infringement litigation with Cipla Limited and Cipla USA Inc., who had submitted an Abbreviated New Drug Application (ANDA) seeking approval to market a generic version of PEDMARK®. Under the settlement terms, Cipla agreed not to launch the generic product until September 1, 2033, barring some predefined conditions permitting earlier entry [S1][S27]. This agreement dismisses active litigation pending since late 2022 and preserves the commercial exclusivity window.

Historical Financial Performance

Fennec's financial trajectory over the past few years shows material growth in revenues aligned with increased commercialization of PEDMARK®. Revenue advanced sharply from negligible levels pre-2022 to $44.6 million in FY2025 [F1]. However, profitability has remained elusive:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 45 | -10 | -12 | -6 | -6.1% | -2134.2% |

| 2024 | 48 | 0 | 27 | 3 | +123.7% | +97.3% |

| 2023 | 21 | -16 | -17 | -13 | +32.3% | |

| 2022 | -24 | -18 | -23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -27.5 |

| 2024 | 7.4 |

| 2023 | 138.1 |

| 2022 | 923.1 |

Source: SEC companyfacts cache [F1].

(Figures per fiscal year ended December 31; sourced from [F1])

The revenue increased nearly twofold between FY2023 and FY2024 but declined slightly by about 6% into FY2025, suggesting some market headwinds or pricing pressures [F1]. Operating income swung from a modest profit back into loss territory in FY2025 (-$6.3M), while net losses widened substantially versus the prior year.

Operating cash flow also reversed strongly from positive $27 million in FY2024 to negative $12.5 million in FY2025, indicating significant expenditure likely tied to expanded sales efforts or international development programs [F1]. Meanwhile, the company's liquidity profile remains strong with $67 million in current assets against about $10 million in current liabilities (current ratio ~6.37), affording a considerable buffer to fund near-term operations without immediate financing [F1][S8].

Intellectual Property Moat and Litigation Landscape

Fennec's competitive moat hinges critically on its intellectual property protections surrounding PEDMARK®. Patents held or licensed cover composition, use methods, and formulation aspects with staggered expiration dates into late-2030s [S1][S4]. These patents are listed in the FDA Orange Book conferring statutory protections against certain generic entries.

The company has actively enforced these patents via litigation—in particular against Cipla’s ANDA filings alleging invalidity or non-infringement—which culminated recently in a favorable settlement delaying generics until at least September 2033 [S1][S27]. Such settlements are common pharmaceutical industry mechanisms balancing costly patent litigation risks against assured market exclusivity timelines.

Nevertheless, residual risks remain palpable: ongoing uncertainties around potential patent invalidation through administrative review procedures (e.g., USPTO inter partes reviews) or district court claims could erode exclusivity prematurely [S4][S11][S14]. Additionally, trade secret protection complements patents but is inherently vulnerable especially given reliance on third-party manufacturers that require information sharing [S24].

Further complexity arises from evolving U.S. patent jurisprudence post-Leahy-Smith America Invents Act with narrower patent scope interpretations challenging enforcement strength for biotech firms like Fennec [S11]. These dynamics necessitate vigilant IP management including licensing strategy refinement.

Market Dynamics and Future Growth Prospects

PEDMARK® addresses an unmet need for preventing cisplatin-induced hearing loss among cancer patients receiving platinum-based chemotherapy—a niche indication offering orphan drug incentives that typically limit competition [S1]. Its expansion potential lies not only in deeper penetration within approved therapeutic areas but also geographic roll-outs beyond the U.S., where regulatory approvals are being pursued [S8][N2].

Growth drivers include increasing oncologic indications adopting platinum regimens globally coupled with heightened awareness amongst clinicians regarding toxicity mitigation strategies.

Conversely, growth caps stem from multiple factors:

- Pricing pressure due to healthcare cost containment initiatives prevalent across developed markets can squeeze reimbursement margins [S19][S22].

- Regulatory uncertainties outside established markets may delay broader access.

- Emerging competitive technologies or off-label substitutes could dilute PEDMARK®’s unique positioning if they gain traction.

- Potential early erosion if unforeseen patent challenges succeed despite current settlements.

Investors should monitor commercialization milestones internationally, real-world clinical adoption trends, potential licensing deals that might supplement revenues beyond U.S.-centric sales, and any new data supporting label expansion.

Financial Outlook and Capital Allocation

While explicit management guidance is not disclosed for upcoming periods in provided materials, key focus areas for evaluation include managing operating losses as scale increases, sustaining sufficient liquidity amid negative operating cash flows, and funding strategic initiatives such as international regulatory submissions.

To date, Fennec has not declared dividends nor initiated share repurchase programs given reinvestment priorities toward product commercial expansion [S16][F1]. Cash is allocated primarily toward sales infrastructure build-out within North America alongside pipeline advancement efforts abroad.

The company may require external capital infusions through equity offerings or debt instruments to extend runway beyond existing cash reserves if operating losses persist at current magnitudes [S8][S18]. Such transactions could introduce dilution risk as noted by outstanding warrants and stock options that expand share count when exercised [S18].

Return metrics remain negative due to consistent net losses relative to shareholder equity (~-27.5% ROE calculated on trailing figures), reflecting the developmental stage nature typical of specialty pharma enterprises investing ahead of mature earnings generation [F1].

Risks Summary

Primary risks confronting Fennec encompass:

- Patent invalidation or circumvention undermining PEDMARK® exclusivity before expected horizons leading to reduced pricing power and lost revenues [S4][S9][S12].

- Difficulty maintaining comprehensive intellectual property protection internationally given varying legal environments [S28].

- Healthcare reforms targeting drug pricing coupled with payer pushback impacting sales volume or reimbursement levels adversely affecting margins [S19][S22].

- High litigation costs even when successful diverting resources away from core operations and creating reputational risk [S7][S10][S13].

- Dependence on third-party manufacturing exposing product supply chain vulnerabilities.

- Operational cash burn requiring additional capital raises which may dilute ownership stakes or increase leverage burden.[S8][S18]

Conclusion: Key Factors To Watch

In absence of explicit guidance statements for coming quarters or years within available disclosures (/), observers should gauge Fennec’s progress based on:

- Outcomes or developments from ongoing or future IP enforcement actions influencing competitive landscape.

- Uptake levels of PEDMARK® addressing physician acceptance and payer coverage dynamics domestically and abroad.

- Additional regulatory approvals enabling expansion into new markets.

- Quarterly financial results revealing any trend shifts in revenue growth trajectory versus operational expenditures.

- Capital raising activities signaling financial runway sufficiency.

- Any announcements surrounding licensing collaborations or partnerships enhancing geographic reach or portfolio breadth.

- Management commentary on cybersecurity protocols given increased emphasis on data privacy alongside operational digitalization risks reported by company [S23][S26].

This profile illustrates a company balancing solid IP-defended asset commercialization against typical risks intrinsic to emerging pharmaceutical players endeavoring sustained profitable scaling amidst evolving legal and regulatory settings.

This analysis is based solely on information publicly available as of March-April 2026 including SEC filings ([F1],[S#]), recent news disclosures ([N#]), without speculative projections beyond documented facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments