Humacyte Advances Symvess® Commercial Sales While Managing Losses and Debt Obligations

The company reports early revenue from its engineered vessel platform amid narrowed net losses, a $77.5 million term loan, and cost-cutting aimed at extending financial runway.

Humacyte’s lead product Symvess® leverages an innovative biologic platform based on acellular tissue-engineered vessels (ATEVs) targeting vascular trauma. While initial commercial sales have begun, the company continues to report substantial net losses driven by ongoing R&D and commercialization investments. To support operations, Humacyte secured a $77.5 million senior secured term loan facility with milestone-based tranche draws and implemented cost-saving measures including workforce reductions. Future growth depends on clinical and regulatory progress alongside effective execution of financial and operational strategies amid sector-specific risks.

Financial Performance Overview

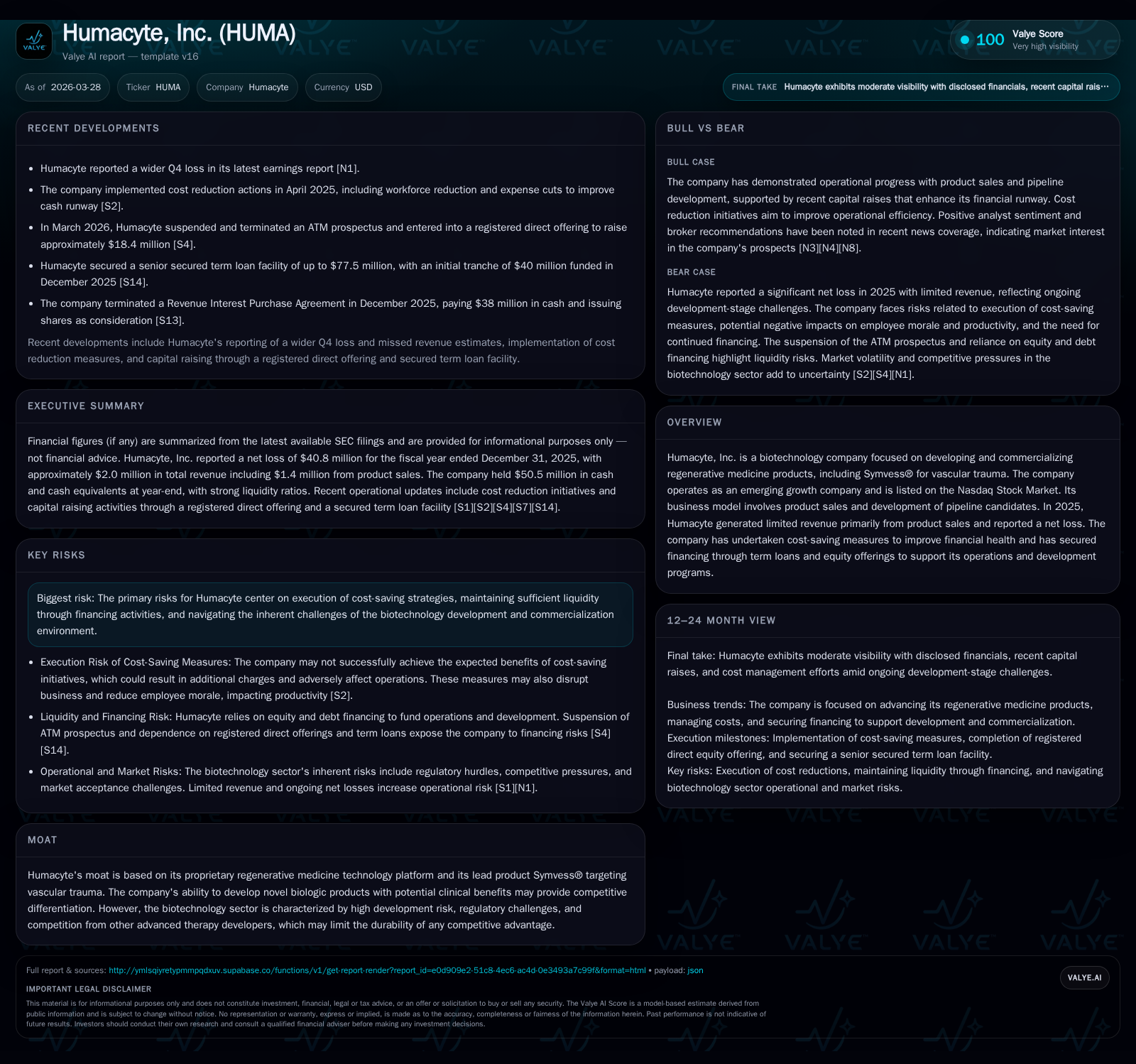

Humacyte remains in the early stages of commercializing its lead product Symvess®, which generated approximately $1.4 million in revenue during fiscal year 2025 as part of total revenues near $2.0 million [S28]. Despite this initial commercial activity, the company reported an operating loss of $108.1 million for FY2025, a modest improvement compared to $114.4 million in FY2024, reflecting continued substantial investments in research, development, and commercialization infrastructure [F1]. Net losses improved significantly year-over-year from $148.7 million in FY2024 to $40.8 million in FY2025 [F1].

Operating cash flow remained negative at approximately $105 million in FY2025 despite a reduction in capital expenditures by nearly 44% to $0.88 million, indicating persistent cash burn amid efforts to manage spending [F1]. The current ratio stood at roughly 3.7 at year-end, supported primarily by cash and equivalents totaling approximately $50.5 million [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -41 | -105 | -108 | 1 | +72.5% |

| 2024 | -149 | -98 | -114 | 2 | -34.2% |

| 2023 | -111 | -73 | -100 | 2 | -825.8% |

| 2022 | -12 | -71 | -85 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -106 | -1313.4 |

| 2024 | -100 | 282.3 |

| 2023 | -76 | -817.8 |

| 2022 | -72 | -10.2 |

Source: SEC companyfacts cache [F1].

Proprietary Technology and Market Position

Symvess® is based on Humacyte’s proprietary acellular tissue-engineered vessels (ATEVs), biologic grafts designed for off-the-shelf use in vascular trauma applications [S6]. This technology differentiates itself from synthetic grafts through a bioengineered matrix that integrates with patient vasculature while minimizing immunogenicity due to decellularization processes.

The manufacturing complexity underlying ATEVs creates barriers to entry; however, the regenerative medicine sector is characterized by high clinical risk and strong competition from other innovators developing tissue-engineered therapies or advanced biologics [S4][S5]. Regulatory approval pathways remain rigorous given the novel nature of these products.

Recent Earnings Update and Market Reaction

In Q4 2025 reporting periods covered by recent news releases [N1][N3], Humacyte missed revenue estimates with product sales falling short of expectations contributing to a wider quarterly loss than anticipated. The stock price declined more than 7% on the day following earnings release reflecting investor concerns about near-term commercialization execution.

Despite these challenges on a quarterly basis, annual results show meaningful improvement in net loss driven by operational efficiencies and cost containment.

Capital Structure and Debt Financing

To support its commercialization phase liquidity needs Humacyte secured a senior secured term loan facility totaling up to $77.5 million as of December 15th, 2025 [S7][S8][S9][S10][S11]. The facility includes:

- An initial fully funded tranche of $40 million.

- Two delayed draw tranches: $12.5 million available between late 2026/early 2027; $25 million between mid-2027/late-2028 contingent upon meeting revenue targets and regulatory approvals.

The loan bears interest at either a floor rate of 11.5% or the Wall Street Journal Prime Rate plus 4.5%, with amortization payments commencing December either late-2027 or late-2028 depending on tranche utilization [S7]. The debt is secured by substantially all assets except immaterial foreign subsidiaries.

Additionally, lenders received warrants exercisable for common stock shares at prices linked to recent funding rounds providing potential equity upside protection [S10][S16].

Cost Reduction Measures

In April 2025 Humacyte implemented cost-saving actions including reducing its workforce by approximately thirty employees and instituting hiring freezes for nonessential roles [S2][S12]. These steps aim to extend the company’s cash runway while aligning expenses with strategic priorities.

Management acknowledges potential risks such as increased severance costs impacting near-term cash flows; possible loss of institutional knowledge; reduced employee morale; and operational inefficiencies during transitions that could affect R&D productivity and commercialization efforts.

Outlook: Milestones and Risks Ahead

While specific regulatory approval timelines for Symvess® remain undisclosed publicly, key upcoming catalysts include pivotal trial readouts relevant to vascular trauma indications along with FDA or international agency decisions [N4][N5]. Progress with pipeline candidates beyond Symvess® may offer longer-term growth opportunities if developmental milestones are achieved.

Analyst sentiment reflects cautious optimism balancing technological innovation potential against clinical development uncertainties and ongoing financial challenges related to losses and financing dependencies.

Key risks include:

- Conditional nature of delayed tranche funding tied to achieving commercial and regulatory milestones.

- Execution risk associated with cost control initiatives impacting workforce stability.

- Competitive pressures within regenerative medicine possibly limiting market share or pricing power.

- Unpredictability of regulatory pathways for novel engineered tissue products affecting timelines.

Monitoring updates on clinical progress alongside liquidity status will be critical for assessing Humacyte’s trajectory.

DISCLAIMER: This analysis is for informational purposes only; it does not constitute investment advice or recommendations regarding any securities discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments