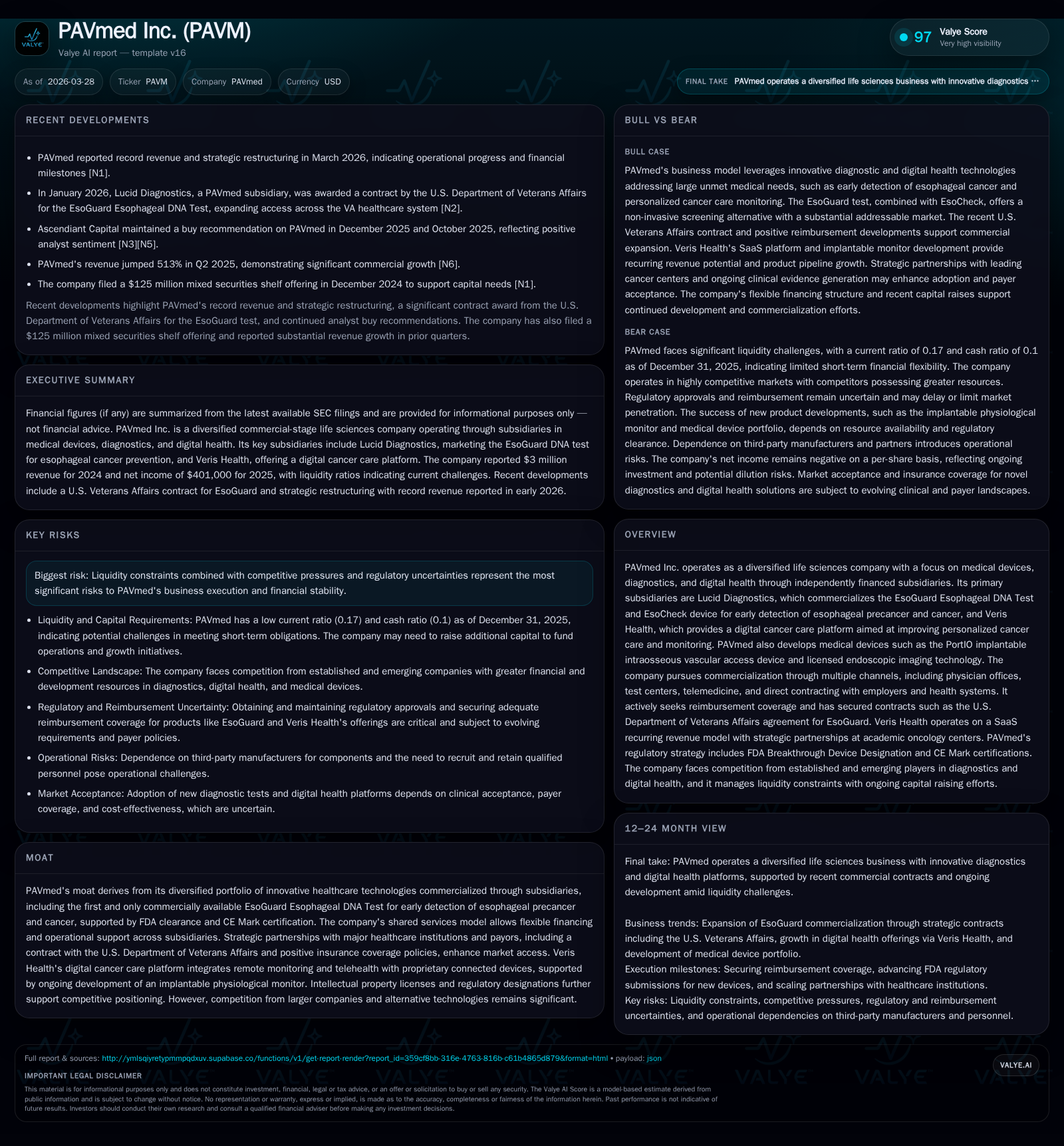

PAVmed’s Strategic Expansion and Persistent Capital Challenges Shape 2025 Performance

The diversified life sciences firm advances commercialization amid restructuring, yet grapples with liquidity and competitive risks.

PAVmed Inc. operates through subsidiaries focused on medical devices, diagnostics, and digital health, notably Lucid Diagnostics’ EsoGuard Esophageal DNA Test and Veris Health’s Cancer Care Platform. After reporting revenue growth in 2024 driven by broader EsoGuard adoption and digital health partnerships, the company continues to face significant operating losses and liquidity pressures, reflecting ongoing investments in product development and commercialization efforts. Its capital structure evolved notably with a preferred stock conversion and debt refinancing, though working capital remains constrained. Regulatory and reimbursement dynamics alongside competitive pressures remain key operational risks moving forward.

Company Overview

PAVmed Inc. is a diversified life sciences holding company operating primarily through independently financed subsidiaries under a shared services model [S1]. Its strategic focus spans medical devices, diagnostics, and digital health technologies aimed at early disease detection and management.

Key subsidiaries are:

- Lucid Diagnostics: Markets the EsoGuard Esophageal DNA Test alongside the EsoCheck Esophageal Cell Collection Device. This combination represents the only FDA-cleared noninvasive diagnostic assay capable of early detection of esophageal precancerous conditions and cancer in gastroesophageal reflux disease (GERD) patients [S1].

- Veris Health: Focuses on digital cancer care platforms integrating telehealth solutions and connected physiological monitoring devices during cancer treatment and survivorship [S1].

PAVmed also pursues internal development projects such as the PortIO implantable intraosseous vascular access device and has acquired endoscopic imaging technology licensed from Duke University [S1].

Historical Financial Performance & Drivers

Recent financial history shows modest revenue growth but persistent operating challenges:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -5 | -22 | -99.0% | ||

| 2024 | 3 | 40 | -34 | -44 | +20.0% | +162.0% |

| 2023 | 3 | -64 | -52 | -69 | +27.9% | |

| 2022 | -89 | -71 | -91 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | 1.2 |

| 2024 | -34 | -1594.8 |

| 2023 | -52 | 119.2 |

| 2022 | -73 | 919.2 |

Source: SEC companyfacts cache [F1].

Revenues reflect sales primarily from Lucid Diagnostics’ EsoGuard test with year-over-year growth of approximately 20% between FY23–24 [F1].

Operating losses have narrowed sharply from nearly $91 million in FY22 to about $21.8 million in FY25, driven by scaled commercialization efforts and cost control initiatives [F1]. The swing to a positive net income figure in FY25 contrasts with prior years’ heavy losses but appears influenced by non-operating factors including equity-related transactions rather than sustained operational profitability given continued negative operating cash flows [F1].

Operating cash flow losses improved markedly in FY25 to about -$5.2 million but remain negative reflecting ongoing investments in research & development and commercialization infrastructure [F1]. Capital expenditures are modest relative to historical levels indicating restrained fixed asset investment consistent with PAVmed’s technology licensing/commercialization focus.

Shareholders’ equity improved substantially from negative territory through FY24 to a positive $34 million by FY25 reflecting successful capitalization events including equity issuances [F1].

Growth Prospects & Strategic Initiatives

PAVmed’s growth outlook is anchored on several fronts:

- EsoGuard test adoption: Lucid Diagnostics leads with the FDA-cleared EsoGuard test for early esophageal cancer detection using its proprietary DNA methylation sequencing assay on samples collected by EsoCheck — the only commercially available noninvasive device for this indication [S1]. Expanding insurance coverage including contracts with the U.S Department of Veterans Affairs supports revenue potential [N1].

- Digital health for oncology: Veris Health is developing a digital cancer care platform combining remote patient monitoring devices with telehealth capabilities targeting personalized care coordination during active treatment phases into survivorship [S1].

- Medical device pipeline: The PortIO implantable intraosseous vascular access device aims to address vascular access challenges; along with licensed endoscopic imaging technologies from Duke University featuring multi-modal optical coherence tomography supports pipeline diversification [S1]. These programs require continued funding before commercial impact.

Commercialization channels include physician offices, test centers, direct payor contracts, employer groups, and telemedicine platforms offering multiple routes for market penetration [S1].

Financial Condition & Capital Structure

Liquidity remains a critical constraint despite recent capital raises:

- PAVmed completed a recapitalization involving issuance of Series D Preferred Stock raising net proceeds near $7.6 million after redeeming Series C Preferred Stock and refinancing approximately $8.4 million of senior secured convertible notes (the "2022 Note") into an amended note due later ("2026 Note") on terms reducing principal outstanding to $15 million [S15].

- Subsequent conversion of all Series D Preferred shares into common stock simplified equity structure but reflects continuing dilution concerns among shareholders [S15].

- Cash & equivalents stood at roughly $1.54 million as of end-FY25 with current liabilities exceeding current assets by nearly sixfold—current ratio about 0.17—indicating tight near-term liquidity coverage [F1].

- Negative operating cash flows around $5.2 million plus modest capex left free cash flow deeply negative circa -$5.2 million in FY25 illustrating ongoing cash burn requiring replenishment through equity or debt markets [F1].

Capital allocation focuses on sustaining commercialization investments while managing debt service obligations amid challenging market conditions for raising additional equity or credit facilities; no dividends or share repurchase programs were reported consistent with early-stage commercialization status [F1][S14][S15][S17].

Regulatory & Competitive Environment Considerations

The company operates within highly regulated frameworks influencing product commercialization trajectories:

- Regulatory approvals like FDA clearance and CE marking are essential milestones achieved for main products like EsoGuard/EsoCheck but ongoing compliance under post-marketing surveillance obligations remains demanding [S26].

- Reimbursement landscape is evolving; PAVmed seeks broader insurance coverage while facing pricing pressure risks per healthcare reform initiatives targeting Medicare/Medicaid cost containment impacting payor policies for diagnostic testing reimbursements [S21][S6].

- Stringent legal requirements under Anti-Kickback Statute, False Claims Act, Physician Payment Sunshine Act necessitate robust corporate compliance programs affecting sales/marketing practices; risk exists for penalties or adverse operational impacts if violations arise [S4][S9][S22].

- Product liability claims represent inherent business risk given medical device exposure though no material litigation is currently reported [S7][S11][S25].

- Privacy regulations such as HIPAA (U.S.) and GDPR (EU) impose data protection disciplines particularly relevant for Veris Health’s digital platform handling sensitive patient information [S16][S21].

- Competitive landscape features established players developing cancer diagnostics or care platforms; PAVmed’s differentiation derives from proprietary assay technology (DNA methylation NGS), integrated device/platform approach by Veris Health, plus strategic institutional partnerships including federal government entities enhancing market access barriers.

What To Watch / Analysis

Absent explicit near-term financial guidance disclosures post-Q3 2025 [N1], key milestones include:

- Pace of EsoGuard test adoption measured by volume growth trends across clinical channels including payor contracting expansion.

- Progression in Veris Health’s platform deployment especially integration of implantable monitors facilitating remote oncology care metrics.

- Pipeline advancement updates on PortIO device development timelines leading toward regulatory submission or pilot commercial rollouts.

- Management’s ability to secure incremental financing at sustainable terms ensuring continuation as a going concern given low liquidity ratios.

- Changes to reimbursement codes or healthcare regulation shifts impacting pricing models for both diagnostics testing and digital health services.

Maintaining differentiated clinical evidence demonstrating EsoGuard’s impact on esophageal cancer mortality reduction could cement payer support – critical since diagnostics reimbursement markets often shift quickly on policy re-evaluation.

Conclusion

PAVmed’s portfolio centered around Lucid Diagnostics’ pioneering noninvasive esophageal DNA testing platform coupled with an emerging digital oncology care offering positions it within niche but growing market segments targeting early cancer detection and personalized treatment monitoring.

However, financial results through FY25 underscore enduring commercial scale-up challenges emblematic of diagnostic/device startups: heavy operating losses improving slowly but offset by liquidity bottlenecks necessitating frequent recapitalizations potentially dilutive to existing stakeholders.

Continued execution rigor will be required to translate innovative intellectual property into sustainable revenues while navigating complex regulatory regimes and evolving reimbursement landscapes that collectively define long-term viability.

This analysis is based purely on publicly available information as filed with regulatory authorities and reported news media as of March 28, 2026 without projecting or speculating beyond disclosed facts or offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments