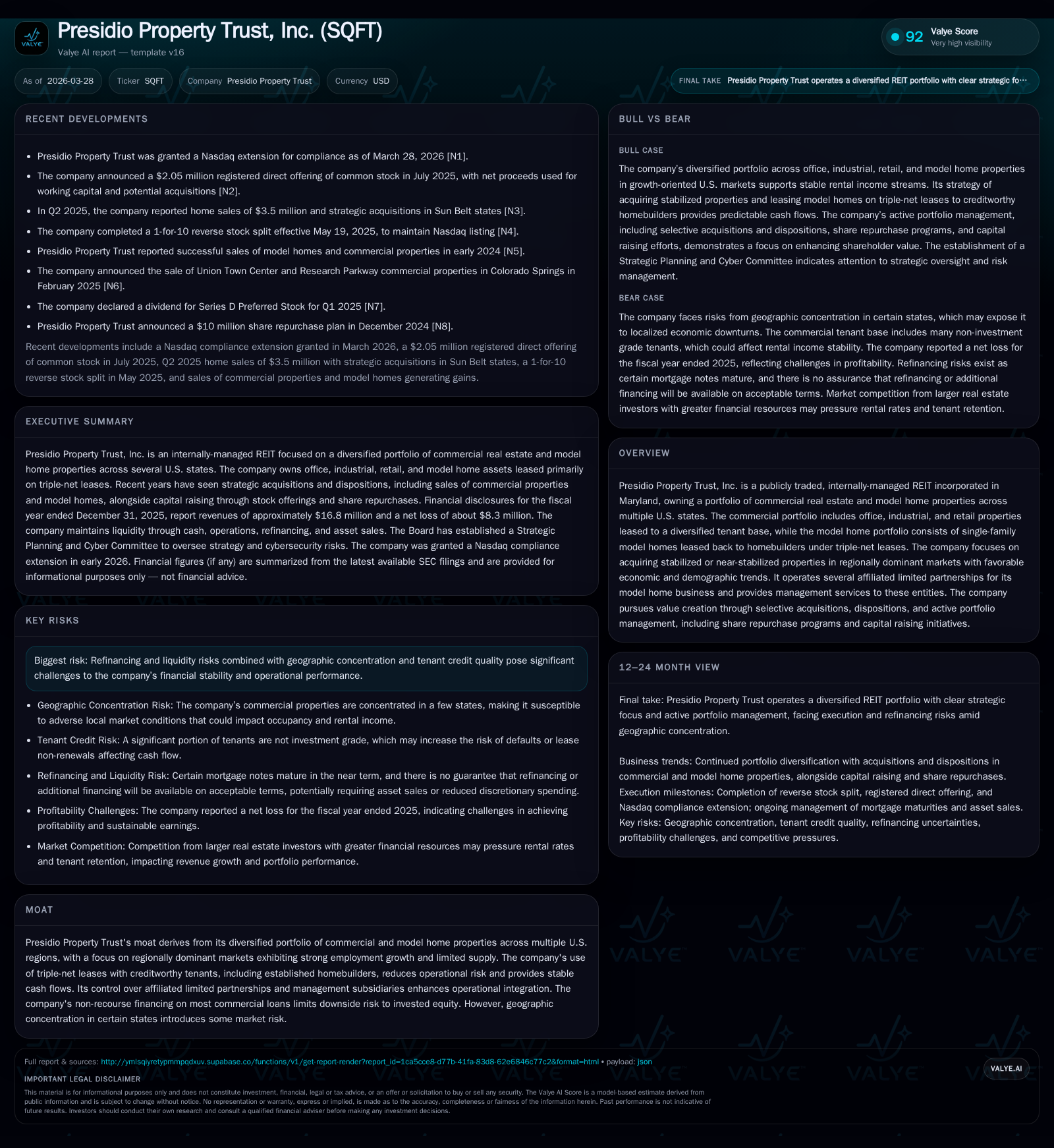

Presidio Property Trust's 2025 Financial Shift Reflects Portfolio and Liquidity Challenges

2025 saw Presidio Property Trust recalibrate its asset portfolio amid a backdrop of refinancing pressures and liquidity constraints.

Presidio Property Trust, an internally-managed REIT with a diverse commercial and model home lease portfolio, experienced an 11.2% revenue decline and a 15.9% drop in operating income in 2025, alongside a significant narrowing of net losses. The company’s concentrated geographic footprint and tenant base provide some cash flow stability via triple-net leases, especially in its model home segment, but expose it to refinancing risks as substantial mortgage maturities loom. While operational cash flows improved into positive territory, liquidity remains tight with approximately $7.4 million in cash, prompting selective asset sales and cautious capital allocation focused on dividends and modest share repurchases. Future growth hinges on successful refinancing, strategic dispositions, and managing tenant quality within key U.S. markets.

Evolution of Presidio’s Asset Portfolio and Financial Performance Through 2025

Presidio Property Trust’s financial results for fiscal year 2025 reveal a recalibration amid a challenging commercial real estate environment and evolving portfolio focus [F1], [S1]. Total revenue contracted by approximately 11.2% to $16.8 million from $18.9 million the prior year [F1]. This decline stems from targeted dispositions of certain commercial properties coupled with dampened rental collections reflecting market dynamics influencing office and industrial segments.

Operating income decreased by nearly 15.9% year-over-year to around $10.7 million [F1]. Despite this operational pressure on earnings, net loss narrowed substantially—from approximately negative $25.6 million in 2024 to negative $8.3 million in 2025—representing a 67.7% improvement although still negative [F1]. The net income trajectory reflects prior impairments or one-time losses related to asset disposals or valuation resets mitigated somewhat by improved core operations.

The company’s strategy focuses on Office/Industrial properties alongside its model home asset class leased under triple-net structures designed to generate steady income with minimal operational burden [S1]. Notably, sales of model homes (6 in 2025 versus 18 previously) influenced non-controlling interests' income allocations at roughly $0.7 million compared to $2.5 million earlier [S1]. Tax impacts related to capital gains from model home sales shifted from a minor benefit ($61k) in 2024 to an expense ($23k) in 2025 [S1].

Geographic and Tenant Diversification: Strengths and Concentration Risks

Presidio’s commercial portfolio consists of ten properties aggregating approximately 768,675 square feet dominated by Colorado (35% of sqft, 41% base rent) and North Dakota (52% sqft, ~33% base rent), supplemented by properties in California (7.5%), Maryland (4%), and Texas (1.4%) [S1], [S18]. This geographic concentration provides exposure to regionally dominant markets with favorable economic traits like employment growth; however, it elevates susceptibility to local economic shifts.

Tenant diversification features about 131 distinct commercial tenants with an average weighted lease duration near three years [S18], providing some stability amid volatility common for CRE portfolios where leasing renewals can be unpredictable. The largest single tenant accounts for almost 6.9% of annualized rent while the top ten tenants cumulatively represent nearly 38%, indicating moderate concentration that requires ongoing monitoring [S18].

Triple-net leases prevalent across both commercial and model home sectors shift costs such as maintenance and taxes onto tenants—a mitigating factor against expense volatility though not eliminating market risk [S18].

Model Home Franchise: Triple-Net Leases as a Stability Lever amid Market Shifts

Presidio maintains a sizeable model home property segment governed through affiliated limited partnerships controlled by the company itself [S1], [S18]. The model homes are primarily leased back on triple-net terms to leading homebuilders—in particular one tenant commanding roughly 69% of model home annualized rents—across Alabama, Texas, Tennessee, and Arizona [S1], [S18]. This contractual structure reduces operating risk but concentrates dependency on cyclical residential construction trends exposed to interest rate shifts and consumer demand fluctuations.

Model homes cycle through leaseback sales when builders conclude projects [S16]. Presidio’s vertical integration via wholly owned subsidiaries managing these partnerships allows enhanced operational control including acquisition financing, asset disposition timing, and fee generation through active management services [S16]. This niche provides recurring cash inflows relatively insulated from tenant turnover costs but creates sensitivity tethered directly to housing market health.

Liquidity Positioning and Debt Maturity Pressures: Navigating Near-Term Refinancing

Liquidity emerged as an acute challenge throughout FY2025 with cash and equivalents totaling roughly $7.4 million at year-end along with restricted balances sufficient primarily for capital expenditures tied to existing property upkeep [S9], [S17]. The Company confronts notable debt maturities amounting to about $30 million due during calendar year 2026—most prominently a $16.4 million non-recourse loan secured by the Shea Center II property in Colorado which matured early January and has since entered receivership following default notification [S9], [S20].

Proceeds from recent property sales partly alleviated refinancing pressures—for example, the Dakota Center disposal yielded approximately $5.1 million contributing over $4 million toward loan settlement with no residual liability due under non-recourse terms [S9], [S20]. Ongoing discussions with lenders target refinancing or extending maturity terms for remaining loans while management anticipates additional proceeds will come from further model home sales backed by historically demonstrated refinance success on such assets [S7], [S8].

Operating cash flow recovery—from negative $0.73 million last year to positive approximately $0.42 million this past year—reflects improved day-to-day performance but overall free cash flow post-capex remains negative given continued investments capped near prior-year levels ($1.2 million annually) [F1], [S10]. These factors underscore persistent liquidity tightness requiring continuous evaluation of capital deployment priorities.

Presidio benefits from non-recourse financing structures that restrict equity downside risk associated with specific assets; however, these arrangements do not fully insulate against corporate-level liquidity stress brought on by clustered upcoming principal obligations requiring active management attention [S20], [N1]. Nasdaq granted an extension on listing compliance related to continuing operational and liquidity challenges further corroborating near-term capital pressure facing the Trust [N1].

Capital Allocation Trends: Dividend Strategy, Buybacks, and Equity Movements

Despite earnings headwinds marked by multi-million dollar net losses compressed relative to previous years, Presidio maintained commitment to shareholder distributions within sustainable coverage parameters inferred from available cash flow sources [F1], [S4], [S7]. Dividend policy remains a pillar of shareholder return alongside conservative share repurchase activity: total Series A common stock buybacks approximated $77 thousand during fiscal year 2025 excluding tender offer repurchases executed earlier that year totaling over $1.4 million; preferred stock repurchases aggregated about $344 thousand illustrating measured capital recycling into equity under favorable price points offered by management initiatives designed to enhance per-share metrics without excessive leverage buildup [S4], [S6], [S13].

Equity book value diminished substantially—from over $50 million reported several years ago down toward approximately $16.8 million at FY2025 end largely reflecting accumulated net losses and impairment-related adjustments resulting from asset sales or mark-to-market declines reflective of real estate cycle pressures seen broadly across small-cap REIT segments over recent periods—highlighting balance sheet contraction risks demanding strategic prudence going forward [F1].

Outlook Insights: Factors Influencing Presidio’s Growth Trajectory

Forward-looking commentary acknowledges that while selective acquisitions remain part of the growth pipeline complemented by active disposition efforts designed to optimize portfolio composition, macro-market uncertainties constrain robust top-line expansion visibility especially given tenant credit variability alongside regional economic cycles peculiar to concentrated states like Colorado or North Dakota where major holdings reside; compounded by financing market conditions impacting debt availability or cost [(N1), (S2)]. Maintaining occupancy levels coupled with prudent lease expiration management will be pivotal as weighted average lease durations hover near three years nationally restricting runway for extended income visibility unless renewals or new signings counterbalance expirations promptly.

Recent disclosures do not include explicit revenue or EBITDA guidance but identify milestones such as refinancing outcomes on maturing loans (notably Shea Center II), volumes of model home sales potentially accelerating liquidity generation streams, alongside occupancy monitoring forming key indicators warranting close surveillance among stakeholders evaluating operational resilience ahead of anticipated macroeconomic fluctuations.

Key Metrics Snapshot: Historical Financials and Cash Flow Dynamics

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 17 | -8 | 417870 | 11 | -11.2% | +67.7% |

| 2024 | 19 | -26 | -728060 | 13 | +7.3% | -352.6% |

| 2023 | 18 | 10 | 1489839 | -0.7% | +577.0% | |

| 2022 | 18 | -2 | 928817 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($) | ROE% |

|---|---|---|---|

| 2025 | -49.1 | ||

| 2024 | 140416 | -1928060 | -96.6 |

| 2023 | 0 | 289839 | 19.9 |

| 2022 | -4.9 |

Source: SEC companyfacts cache [F1].

Note: Capex data only available for FY2023-24; CFO = Operating Cash Flow; OpInc = Operating Income; Net Income all values USD.

This analysis synthesizes sourced financial disclosures emphasizing Presidio Property Trust’s dual-portfolio strategy incorporating stabilized office/industrial assets alongside its distinctive model home leaseback franchise hinged on triple-net arrangements providing insulation amid sector-wide headwinds while confronting tangible refinancing stresses projected into near term horizon compounded by concentrated geography/tenant profiles requiring deft liquidity navigation going forward.

Investors should consider these factors holistically recognizing absence of explicit forward projections beyond qualitative guidance necessitating ongoing monitoring of refinancing developments plus asset management outcomes before revising expectations materially.

Disclaimer: This report is produced for informational purposes only based on publicly filed SEC documents and verified news sources without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments