Instil Bio's Strategic Shift After Lead Candidate Discontinuation and Persistent Early-Stage Challenges

Instil Bio, Inc. faces a pivotal moment following the termination of its lead bispecific antibody program, maintaining focus on in-licensing novel therapeutics amid operational and financial hurdles.

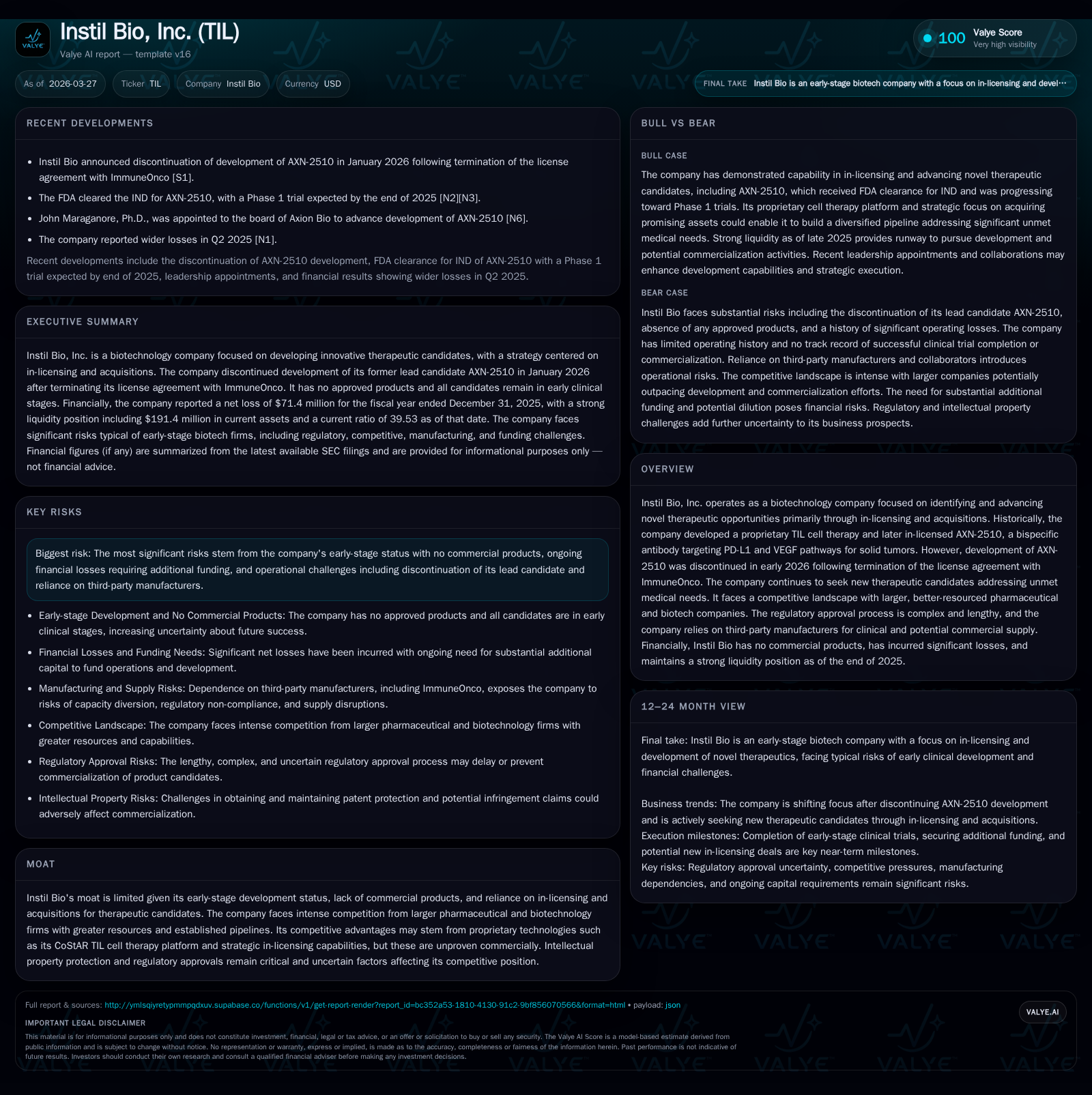

Instil Bio has historically concentrated on proprietary TIL cell therapy development before pivoting to in-licensed candidates like AXN-2510, whose development was discontinued in early 2026 following license agreement termination. The company operates without commercial products, depends heavily on third-party manufacturers, and competes against larger drug developers. Financially, Instil Bio continues to record substantial losses but maintains a strong balance sheet liquidity position. Future growth prospects hinge on successfully acquiring or licensing new therapeutic candidates that address significant unmet medical needs while navigating rigorous regulatory and commercialization complexities.

Company Overview and Historical Development

Instil Bio, Inc., operates as an early-stage biotechnology entity primarily engaged in discovering and advancing therapeutic candidates through in-licensing agreements and acquisitions rather than purely internal discovery efforts. Initially, the company concentrated its efforts on developing an innovative tumor infiltrating lymphocyte (TIL) cellular therapy dubbed CoStAR, engineered around targeting folate receptor alpha present on certain tumor types credited for their immunosuppressive microenvironment characteristics. However, demonstrating adaptability of its business model, Instil Bio shifted strategic direction toward externally sourced product candidates as exemplified by the August 2024 acquisition of licensing rights for AXN-2510 from ImmuneOnco—a bispecific antibody targeting PD-L1 and VEGF pathways aimed at solid tumor oncology indications.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -71 | -37 | -79 | +3.7% | |

| 2024 | -74 | -56 | -74 | 0 | +52.5% |

| 2023 | -156 | -82 | -159 | 21 | +30.1% |

| 2022 | -223 | -180 | -226 | 85 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -62.7 | |

| 2024 | -56 | -43.8 |

| 2023 | -103 | -69.1 |

| 2022 | -265 | -61.4 |

Source: SEC companyfacts cache [F1].

This latter program evolved into the company’s lead asset until the license agreement was terminated in January 2026 alongside cessation of AXN-2510 development [S1]. This transition underscores a significant inflection point: the company ceased advancing this bispecific antibody candidate that embodied a novel dual checkpoint/angiogenesis blockade mechanism intending to disrupt tumor immune evasion and neovascularization simultaneously—an approach increasingly crowded yet still promising within immuno-oncology.

Historical Financial Performance

Since inception through FY2025, Instil Bio has operated without revenue generation from commercialized products — typical for companies positioned predominantly within translational biopharma realms reliant on upfront financing rounds for development capital. The historical financial trajectory reflects steep losses initially coinciding with preclinical and early clinical research expenses followed by a moderation of these operating deficits:

| FY | OpInc (USD) | Net (USD) | CFO (USD) | Capex (USD) | Equity (USD) |

|---|---|---|---|---|---|

| 22 | -226.5M | -223.2M | -180.2M | 84.6M | 363.6M |

| 23 | -159.2M | -156.1M | -82.0M | 20.7M | 225.8M |

| 24 | -73.5M | -74.1M | -55.7M | 0 | 169.4M |

| 25 | -78.6M | -71.4M | -36.6M | 0 | 113.9M |

Despite continued losses totaling approximately $71 million net income loss in FY2025 [F1], improvements relative to prior years indicate refinements in cost control yet reflect ongoing investment consistent with drug development timelines typical of cell-based immunotherapies and biologics.

Operating cash flow remains negative (-$36.6 million in FY2025), although showing year-on-year improvement (+34% versus FY2024), indicative of reduced cash burn intensity possibly related to program discontinuation activities and operational streamlining [F1]. Capital expenditures ceased entirely by FY2024 after prior investments presumably related to infrastructure build-out and technology development plateaued.

The company's equity base contracted from $363 million at end-2022 down to just under $114 million by year-end 2025 [F1], signaling dilution effects through financing rounds combined with accumulated deficits impacting net assets.

Current Position & Operational Constraints

Financially sound short-term liquidity is evident from an exceptionally high current ratio around 39 [F1], driven primarily by large balances held as current assets ($191 million) against comparatively minimal current liabilities ($4.8 million), positioning Instil Bio comfortably able to meet near-term obligations.

Yet, absence of revenues places substantial pressure on capital markets access to fund continuing operations including discovery efforts and clinical trial funding commitments necessary for next-generation therapeutic candidates potentially acquired or licensed thereafter.

Operationally, the company is reliant upon third-party manufacturers for both clinical trial supplies and any future commercial production needs—a common industry practice but one introducing potential risks relating to supply chain reliability, quality assurance standards adherence, and cost structures [S1].

Additionally, cybersecurity is specifically highlighted as a material risk area with dedicated governance involving senior management oversight, indicatively reflecting heightened sensitivity given the data-intensive nature of biotechnology development activities [S1].

Growth Prospects and Strategic Outlook

Prospective growth opportunities are substantially dependent upon successfully identifying additional therapeutic candidates—either through acquisitions or exclusive licensing deals—that address diseases with high unmet medical needs [S1]. Given terminated collaboration with ImmuneOnco affecting AXN-2510's progression, Instil Bio must pivot effectively toward new pipeline assets capable of attracting investigator interest along with regulatory favor.

Intense competition from well-capitalized pharmaceutical giants and established biotech players compounds these challenges; these competitors possess significant advantages in R&D infrastructure scale, global regulatory experience, expansive intellectual property portfolios, manufacturing capabilities, clinical trial networks, and commercial reach [S1].

Consequently, Instil Bio’s moat fundamentally resides in technological differentiation offered by proprietary approaches such as their CoStAR platform coupled with strategic agility in deal-making rather than scale or broad market penetration so far unproven commercially.

The lengthy and costly regulatory approval process remains a formidable barrier; any delays or failures could drastically impact value realization [S2]. Moreover, reimbursement landscape uncertainties including increasing payor scrutiny over drug pricing dampen prospects further [S4].

Risk Profile Summary

Major risks confronting Instil Bio include:

- Continuation of operating losses necessitating substantial additional capital infusions subject to market conditions and investor appetite [S2].

- Absence of revenue-generating products magnifying reliance on pipeline success.

- Intellectual property challenges encompassing patent validity issues as well as competitor infringement risks .

- Compliance burdens due to evolving U.S., state and international healthcare regulations regarding marketing practices, data privacy/security laws such as HIPAA/HITECH amendments, pricing transparency mandates like the Physician Payments Sunshine Act, anti-kickback statutes among others .

- Political uncertainties tied to prior partnerships with Chinese entities expose potential geopolitical risk layers affecting collaboration continuity [S19].

- Product liability exposure intrinsic to clinical trial conduct escalating if/when commercial launch occurs [S24].

- Cybersecurity threats addressed through structured management oversight but remain inherent risks within modern biotech firms handling sensitive data sets .

Capital Allocation & Returns Considerations

With no revenues or product cash inflows at present stage, returns metrics such as ROE are negative (~-62% based on latest annual net loss divided by equity end-period value), as expected given developmental-phase biopharma economics [F1]. Free cash flow remains negative aligned with operational expenditures exceeding any investment inflows [-$36 million roughly equal to CFO minus Capex] [F1].

No dividend payouts or share repurchase programs exist given cash conservation needs described explicitly across filings.

Forward-Looking Milestones & What To Watch For (Analysis)

Absent explicit management guidance published post-license termination of AXN-2510 beyond corporate update disclosures expected around annual reports or investor communications, observers should monitor:

- Progression or announcements regarding new asset acquisitions or licensing deals reflective of strategic pipeline replenishment.

- Updates regarding advancement of remaining CoStAR TIL platform-based therapies if internally developed trials recommence or expand.

- Fundraising activities necessary to sustain operations including potential debt/equity transactions.

- Regulatory interaction outcomes especially IND filings acceptance or initiation of early phase clinical trials targeting distinct oncologic indications.

- Alterations or improvements in manufacturing partnerships addressing supply chain resilience concerns.

Collectively these factors will shape market perceptions regarding viability trajectory amidst a challenging competitive environment marked by scientific complexity requiring multidisciplinary expertise integration typical within contemporary cell therapy development ecosystems.

Conclusion

Instil Bio sits at a crossroads following abrupt cessation of its lead bispecific antibody program owing to contractual disputes but retains a foundational cell therapy technological asset originally cultivated internally prior to recent strategic pivots towards external innovation sourcing approaches. The path forward necessitates agile therapeutic candidate pursuit under considerable resource constraints typical for emerging biotechnology firms operating without commercial revenue streams while contending with intensifying competition from better-resourced peers. Financial stewardship evidenced through improved cash flow metrics contrasted against sustained net losses suggests controlled burn rate adjustment but ongoing capital dependency remains critical risk underpinning near-term sustainability considerations.

Looking ahead requires close attention toward deal flow velocity among novel immuno-oncology platforms plus successful navigation across regulatory hurdles integral for validation of proprietary technologies hoped to translate into viable clinical products that eventually can deliver differentiation within crowded treatment paradigms predominantly targeting aggressive solid tumors refractory to existing standard-of-care modalities.

Disclaimer: This report provides an informational overview based solely on publicly available documents without offering investment recommendations or opinions regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments