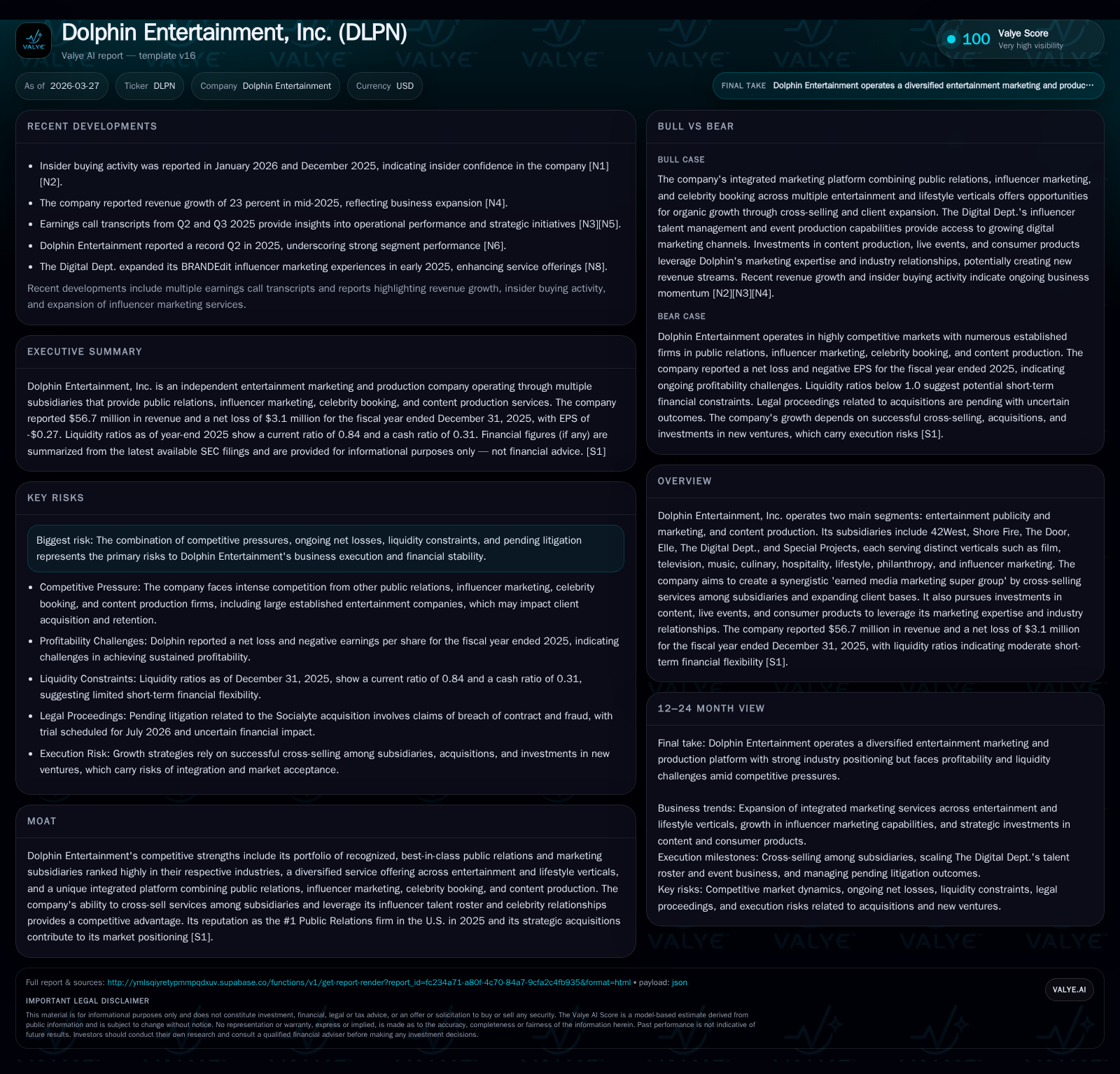

Dolphin Entertainment’s Cross-Selling Model Strengthens Market Position and Service Depth

Dolphin Entertainment leverages a consortium of specialized subsidiaries to fuel revenue growth while addressing profitability and litigation risks.

Dolphin Entertainment, Inc. has developed an integrated 'earned media marketing super group' model by consolidating leading public relations and influencer marketing agencies servicing diverse entertainment and lifestyle sectors. This approach propelled nearly 10% revenue growth in 2025, nearing operating breakeven despite sustained net losses. The company’s strategic cross-selling among subsidiaries enhances competitive positioning but faces challenges from liquidity constraints and pending litigation related to the Socialyte acquisition. Going forward, expansion in influencer talent management, event production, and selective investments underpin growth prospects, balanced against legal uncertainties and cash flow pressures.

Consolidated Performance: Growth Trends and Profitability Patterns

Dolphin Entertainment reported substantial revenue growth over the past several years culminating in $56.7 million for fiscal year 2025, marking a 9.7% increase compared to $51.7 million in FY2024 [F1]. This growth trajectory stems largely from the company’s strategic cross-selling initiative that leverages its portfolio of specialized subsidiaries to upsell and broaden services across clients’ multimedia needs.

While revenues have moved robustly upward through FY2022–FY2025 (a compound annual growth trend visible from $40.5 million in FY2022), operating income tells a story of transition; the operating loss contracted sharply from -$10.5 million in FY2024 to approximately break-even at -$39 thousand in FY2025 [F1]. This near-elimination of operating losses illustrates meaningful progress toward operational leverage as fixed costs are better absorbed by rising revenues.

Net income likewise reflects the trend toward improved profitability but remains negative at around -$3.1 million for FY2025 compared to a larger -$12.6 million loss in FY2024 [F1]. The scale-back in net losses—more than 75% year-over-year—is a positive signal that earnings pressure may moderate further if current strategies persist.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 57 | -3 | -2 | 0 | +9.7% | +75.5% |

| 2024 | 52 | -13 | 0 | -10 | +19.9% | +48.3% |

| 2023 | 43 | -24 | -5 | -20 | +6.5% | -410.4% |

| 2022 | 41 | -5 | -4 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -31.9 |

| 2024 | -108.2 |

| 2023 | -122.2 |

| 2022 | -14.0 |

Source: SEC companyfacts cache [F1].

Table provides explicit historic revenue growth rates and shows operating loss narrowing towards break-even along with improving net income trends.

Subsidiary Synergies and the Earned Media Marketing Super Group Model

Dolphin’s corporate strategy centers on assembling an "earned media marketing super group" composed of best-in-class public relations and marketing firms covering complementary verticals within entertainment and lifestyle domains [S1][S5][S6][S7]. This integrated platform includes:

- 42West: Public relations leader focused on film, television and gaming.

- Shore Fire: Specializes in music industry PR across major U.S markets.

- The Door: Culinary and hospitality-focused marketing with high-margin consumer products PR.

- Elle Communications: Philanthropy and social impact public relations.

- The Digital Dept.: Influencer marketing powerhouse offering talent management and campaign execution.

- Special Projects: Celebrity booking agency facilitating brand-events synergy.

Each subsidiary maintains depth of expertise within its niche while leveraging collective capabilities through cross-selling efforts [S6]. A prime example lies with The Digital Dept., which embeds influencer marketing campaigns seamlessly into broader PR strategies run by sister agencies like 42West or Shore Fire — essential underpinnings of contemporary earned media campaigns that drive social awareness beyond traditional outlets.

This model fosters client wallet share expansion as brands seek multi-channel promotion spanning social media influencer activations alongside classic publicity push [S7]. Moreover, the group achieved recognition as the #1 Public Relations firm in the U.S. during 2025 according to the New York Observer [S1], highlighting market validation of Dolphin’s approach.

Revenue Drivers: Public Relations, Influencer Marketing, and Content Production Dynamics

Public relations remains Dolphin’s core revenue engine via wide-ranging campaigns for film releases (42West), high-profile music artists (Shore Fire), celebrity chefs (The Door), charitable entities (Elle), plus celebrity endorsements enabled by Special Projects [S15].

Crucially though is The Digital Dept.'s role as an influencer marketing linchpin that taps over 300 market-leading Instagram-centric talents primarily spanning beauty, fashion and wellness verticals [S15][S18]. This division facilitates paid & organic brand campaigns bolstered by data analytics and also organizes high-touch influencer events (‘showrooms’) showcasing multiple brands simultaneously — formats successfully hosted since 2021 across major U.S cities [S13][S18].

While content production via Dolphin Films—led by an Emmy-nominated CEO—represents a smaller slice financially compared with marketing segments [S15], it adds differentiation through owned intellectual property like documentaries (e.g., 'The Blue Angels') and feature film reboots ('Youngblood') contributing ancillary revenues [S15].

Litigation and Risk Landscape: Impact Assessment and Legal Proceedings Update

Litigation stemming from Dolphin’s acquisition of Socialyte remains an ongoing risk factor with a trial scheduled for July 2026 [S4]. Allegations include breach of contract and fraud claims between Dolphin Entertainment and NSL Ventures (Socialyte seller). While this has injected some uncertainty into valuation considerations, management currently assesses no material financial impact expected based on advice from outside counsel [S1][S4].

Additional risks highlighted include competitive intensity across all subsidiaries' industries—from boutique firms to large agencies—and cybersecurity governance challenges addressed via dedicated management oversight and external audits [S8]. These factors necessitate continued vigilance but remain manageable within current frameworks.

Financial Health: Liquidity Position, Cash Flows, and Capital Structure

Dolphin's liquidity position exhibits cautionary signals; its current ratio stands at approximately 0.84 at year-end 2025 indicating current liabilities exceed current assets slightly [F1][S24]. Negative operating cash flow worsened markedly from about -$158 thousand in FY2024 to roughly -$2 million in FY2025 despite revenue gains [F1], suggesting working capital demands or investment activities exert pressure.

Equity declined steadily over recent years reflecting cumulative losses—$9.69 million as of end-2025 down from $11.65 million in prior year—but remains positive supporting balance sheet stability currently [F1]. Capital expenditures appear minimal with no significant changes recorded implying lean operational investment consistent with service-based business models [F1][S17][S18].

Capital Allocation Review: Absence of Dividends and Share Buybacks Explained

Consistent with ongoing net losses and tight liquidity profile demonstrated above [F1][S24], Dolphin Entertainment has suspended any dividend distributions or share repurchase programs [S25][S26]. Free cash flow remains negative due to operating cash flow deficits without offsetting capex reductions [F1], reinforcing the cautious stance prioritizing cash preservation for sustaining operations while investing selectively in growth initiatives such as acquiring complementary subsidiaries or expanding talent rosters.

Looking Ahead: Growth Catalysts, Market Challenges, and Analyst Watchpoints

Future expansion prospects hinge upon Dolphin further amplifying its cross-selling capabilities across existing subsidiaries while scaling The Digital Dept.'s influencer talent pool into new verticals like skin care/cosmetics/beauty targeting premium young adult segments via platforms TikTok and YouTube [S18]. Similarly boosting specialty units like Shore Fire into additional music genres/markets (e.g., Latin), The Door’s consumer product PR accounts expansion beyond hospitality niches into broader high-margin categories offers upside potential [S10][S16].

The company also plans to leverage integrated celebrity bookings via Special Projects alongside live event development promoting deeper client engagement providing diversified revenue streams beyond traditional PR campaigns [S13][S23]. Investments classified under 'Dolphin Ventures' focus on content creation/ownership plus consumer products present strategic avenues balancing risk with potential returns through proprietary assets [S17][S23].

Caution resides around resolution timing/outcome of Socialyte litigation due July 2026; any adverse ruling could affect confidence or financial assumptions though currently deemed immaterial to core operations [S4]. Operational margin improvement toward profitability break-even remains critical if sustainable capital returns or deleveraging are future priorities. Analysts will closely monitor quarterly progress on margin expansion coupled with cash flow stabilization alongside successful integration of new acquisitions added to the "super group" ecosystem.

Disclaimer: This analysis is based solely on information available as of March 27, 2026 from official SEC filings referenced herein ([F1],[S#]) without projections or investment recommendations. Readers should consider inherent risks including market competition and litigation outcomes when evaluating company prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments