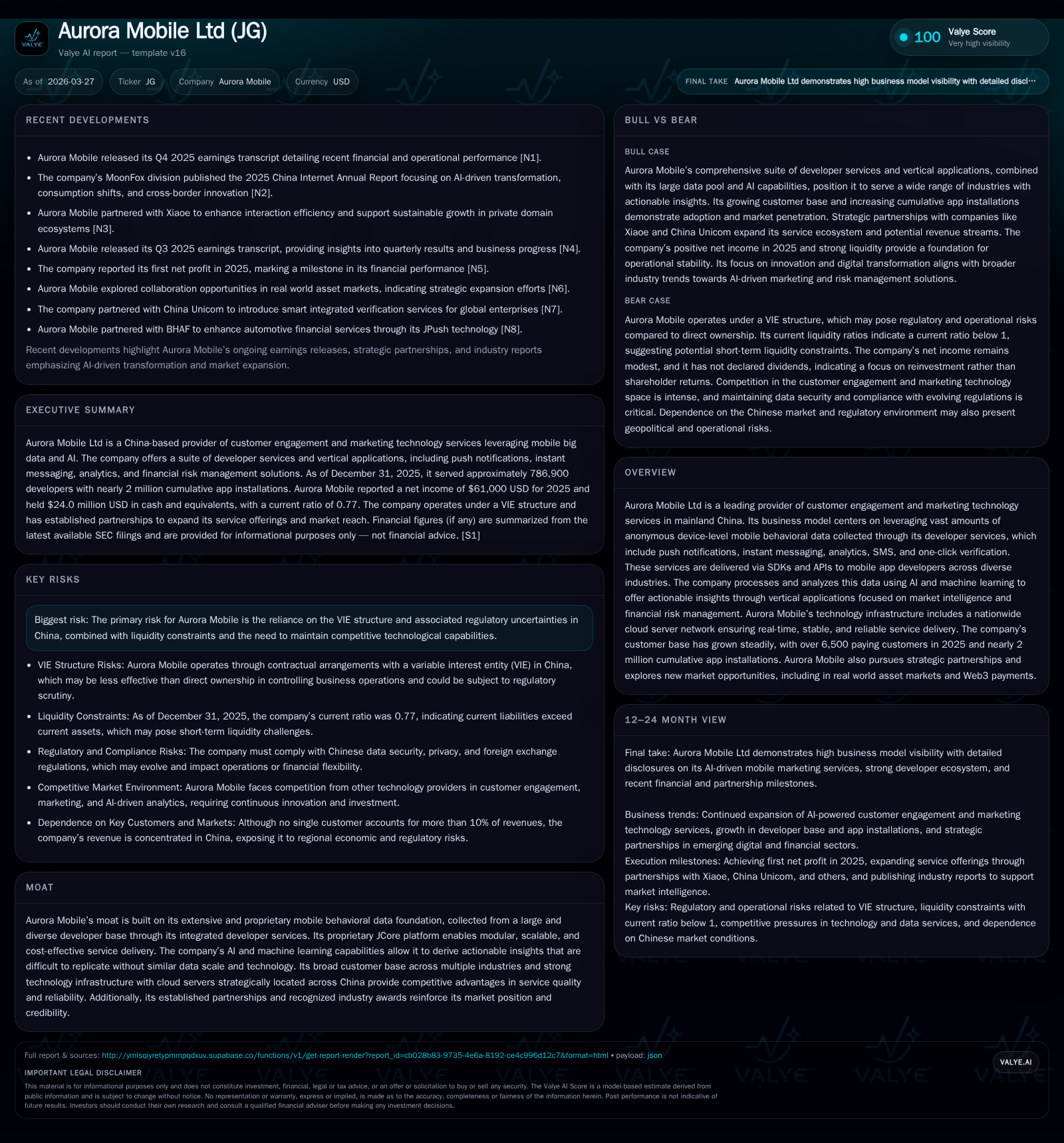

Data-Driven Growth and Capital Discipline Shape Aurora Mobile’s 2025 Performance

Aurora Mobile leveraged its proprietary mobile behavioral data platform to achieve positive operating income and robust cash flow in 2025 despite prior years of operating losses and regulatory complexities.

After enduring steep operating losses from 2022 through 2024, Aurora Mobile Ltd turned the corner in fiscal 2025, registering a modest positive operating income of $101,000 and net income of $61,000 [F1]. This turnaround was underpinned by strong operating cash flow growth to $9.28 million supported by disciplined cost management and expanding SaaS business offerings anchored on its proprietary mobile data aggregation and AI-driven analytics platform [S1][S4]. The company’s broad customer base exceeded 6,500 paying customers by 2025, with vertically tailored market intelligence and financial risk management applications driving subscription growth [S10]. While liquidity and capital allocation strategies remained cautious amid Chinese regulatory constraints governing the VIE structure and foreign currency flows, Aurora Mobile's ongoing investments in R&D and strategic partnerships position it well for sustained growth. Key catalysts to watch include warrant exercise timelines and customer expansion metrics [N1][S2].

From Struggles to Stability: Aurora’s Financial Journey Through FY2023 to FY2025

Aurora Mobile Ltd endured persistent operating losses between FY2022 and FY2024 before turning profitable in FY2025 with an operating income of $101,000 compared to a loss of -$1.36 million in FY2024 and a significantly deeper loss of -$7.17 million in FY2023 [F1]. Net income similarly improved dramatically from a loss of -$965K in FY2024 to a positive $61K in FY2025. The inflection reflects both top-line stabilization within the SaaS businesses as well as rigorous cost control including lower amortization charges.

Operating cash flow is an even more telling indicator of the operational turnaround, skyrocketing nearly sevenfold from $1.17 million in 2024 to $9.28 million in 2025 [F1][S1]. Non-cash expenses such as depreciation (down from RMB1.3M in 2024 to RMB0.9M) and amortization also eased slightly while working capital movements favored cash generation through reductions in accounts receivable and increases in deferred revenue balances.

Capex expenditures plunged sharply by over 90% YoY to just $36,000 reflecting completion of prior period infrastructure investments; this capital discipline fed into free cash flow which approximated CFO less capex at about $9.24 million for FY2025 [F1]. Combined with greater profitability, these dynamics mark Aurora’s first sustained shift away from prior years’ negative cash flow trends.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | 9 | 0 | 36000 | +106.3% |

| 2024 | -1 | 1 | -1 | 617000 | +89.0% |

| 2023 | -9 | -3 | -7 | 43000 | +43.6% |

| 2022 | -16 | -3 | -19 | 92000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1087000 | 9 | 0.6 |

| 2024 | 355000 | 1 | -10.4 |

| 2023 | 522000 | -3 | -84.4 |

| 2022 | 245000 | -3 | -83.8 |

Source: SEC companyfacts cache [F1].

Note: Operating Income year-over-year percentages reflect reduction magnitude for losses (improvement).

Leveraging Proprietary Data Assets: The Core of Aurora Mobile’s SaaS Business Model

Aurora Mobile’s competitive moat rests fundamentally on its vast proprietary mobile behavioral data obtained through its SDK integrations embedded within nearly two million mobile apps serving diverse sectors such as media, finance, e-commerce, gaming, education, and healthcare across China [S4][S14]. This data foundation enables the company’s Software-as-a-Service platforms for developer tools—covering push notifications (JPush), instant messaging (JMessage), SMS services (JSMS), verification APIs (JVerification)—and increasingly sophisticated vertical applications delivering actionable insights.

Its JCore platform facilitates modular, scalable delivery across multiple telecom operator networks with fault-tolerant active-active cloud architectures positioned strategically in Beijing, Guangzhou, Shanghai domestically as well as internationally via centers in Singapore, Hong Kong and Europe [S19]. This infrastructure ensures low-latency real-time communications critical for high message throughput volume.

Aurora applies advanced AI/ML algorithms on cleansed and anonymized device-level data sets stored on this platform to power its vertical solutions primarily targeted at market intelligence—such as app usage analytics via iApp—and financial risk management tools employed by licensed lenders including banks and insurance firms for credit assessments [S4][S15]. The breadth of anonymized behavioral tags combined with multi-model machine learning allows granular user profiling difficult for competitors lacking similar scale or integrated SDK presence.

Evolving Growth Drivers and Industry-Specific Applications Powered by AI Insights

Verticalization represents a crucial revenue driver where Aurora tailors AI-powered analytics products addressing specific industry pain points. Market intelligence suites subdivide into enterprise-grade dashboards offering app operational insights across competitive landscapes plus fund-oriented trend analyses aiding portfolio monitoring for investment firms [S14][S24].

Financial risk management leverages multi-dimensional tags drawn from payment behaviors and consumer finance app usage patterns refined into predictive models used for default risk classification and blacklist maintenance based on delinquency histories compiled with governmental or third-party data sets [S15]. These capabilities generate sticky recurring subscription revenues often priced per query volume or through annual tiered packages.

Additionally notable are newer offerings such as GPTBots.ai—a no-code/low-code AI agent platform integrating large language models which helps enterprises automate workflows enhancing customer support efficiency—representing growth avenues outside core mobile engagement tools [S5].

Aurora emphasizes cross-selling owing to the interconnectedness of its platform functionalities allowing customers access to suites covering full customer lifecycle needs—from user acquisition push campaigns using JPush through risk analytics on lending decisions—boosting both revenue depth per client and renewal rates.

Capital Allocation Strategy: Navigating Liquidity, Buybacks, and Investment Trends

Despite improving profitability the company faces restrictions on dividend distributions due to accumulated loss reserves at the subsidiary level under Chinese accounting regulations limiting upstream dividend payments until profits accumulate [F1][S9]. Nevertheless, Aurora generated strong operating cash flow (~$9.3 million) while curbing capital expenditures to only $36K USD in FY25 from over $600K the prior year demonstrating disciplined capital spending [F1][S12].

Notably share repurchases increased substantially reaching approximately $1.09 million versus prior years below $400K indicating board confidence that buybacks are an accretive use of capital amidst improving fundamentals [F1].

Research & development investments remained significant at roughly RMB104.7 million (~$15 million USD), underscoring continued prioritization of innovation especially around AI-powered enhancements including GPTBots.ai adoption scenarios supporting long-term competitiveness despite near-term margin pressures inherent to software platform upgrades [S10][S19].

Navigating Regulatory Nuances: Impact of VIE Structure and Chinese Foreign Exchange Rules

Aurora Mobile operates through a Variable Interest Entity (VIE) structure common among Chinese tech companies listing abroad but inherently carrying compliance risks given potential shifts in legality or enforcement interpretation surrounding foreign ownership of culturally sensitive or strategic data assets [S1][S11].

The company relies heavily on this structure maintained via contractual agreements enabling consolidated financial control but subject to regulatory uncertainty amid broader PRC tightening on digital economy governance including recent anti-monopoly law extensions targeting improper data use practices potentially relevant given Aurora's data monetization focus [S18][S20].

Transfers of funds out of mainland China subsidiaries require SAFE registration though routine current account payments like dividends may be made without prior approval if conforming procedural requirements are met; however dividends can only be paid from accumulated profits post-loss recovery with mandated reserve fund allocations restricting immediate repatriation opportunities further complicating liquidity deployment at the American Depositary Share parent level despite overall strong reported cash balances >$24 million at end-2025 [F1][S9].

Any M&A or capital raising activities overseas face additional scrutiny aligned with new security review regulations adding complexity toward strategic execution plans involving foreign investors or acquisitions deemed relating to "national security" concerns per Ministry of Commerce guidance noted recently [S11][S18].

Key Milestones Ahead: Warrants, Customer Base Expansion, and Market Indicators to Watch

A key forthcoming catalyst is the exercise window for PAG Pegasus Fund warrants issued Feb 11, 2026 allowing purchase up to approximately 725k ADS shares at a strike price ~$13.80 per ADS expiring Feb 10, 2029—an over +85% premium versus recent averages near $7.43—potentially providing incremental capital inflows if exercised supporting balance sheet flexibility amidst strategic growth investments [N1][S2].

Customer traction remains encouraging with reported paying customers surpassing 6,587 by end-2025 growing steadily year-over-year since inception; this base spans various SaaS offerings emphasizing cross-selling uptake within market intelligence subscriptions and financial risk management licensing critical for meaningful revenue expansion going forward [F1][S10].

Analysts should monitor renewal rate trends across vertical products together with average revenue per user metrics plus any shifts related to new regulatory policies impacting marketing or data services access within China’s evolving digital ecosystem.

Financial Health Snapshot: Profitability, Cash Flows, and Cost Management Metrics

Key financial indicators underscore improved operating leverage with operating income margins recovering into slight profitability after years below zero accompanied by net income turning mildly positive for the first time since fiscal losses began accumulating rapidly post-IPO period:

- Operating margin recovery reflects mix shift towards higher margin SaaS products coupled with effective expense rationalization especially reduced share-based compensation costs relative to revenue scale.

- Adjusted cash flows benefited strongly from working capital optimization reducing accounts receivable days alongside deferred revenue growth signaling improved billing discipline.

- Current ratio stands below unity around ~0.77 indicative of tight short-term liquidity given elevated current liabilities further confirming need for careful cash flow stewardship amid capital account transfer limitations enforced under Chinese capital controls.[F1][S12]

- Equity base shrank considerably following losses peaking around -$15M equity deficit but rebounded by end-2025 approaching $9.4M positive demonstrating balance sheet repair underway alongside sustained profitability effort.

- Capital expenditures minimized signaling shift from build-out phase toward operational efficiency focus going forward.[F1]

This snapshot mirrors a classic technology turnaround transition phase where intangible assets such as proprietary algorithms enriched by unique behavioral data sets combined with AI analytical expertise form entry barriers difficult for competitors lacking equivalent scale or ecosystem integration.

Disclosure: This write-up is prepared solely for informational purposes summarizing publicly available data from SEC filings ([F1], [S#]) and news reports ([N#]). It is not a recommendation or solicitation regarding any investment decisions related to Aurora Mobile Ltd or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments