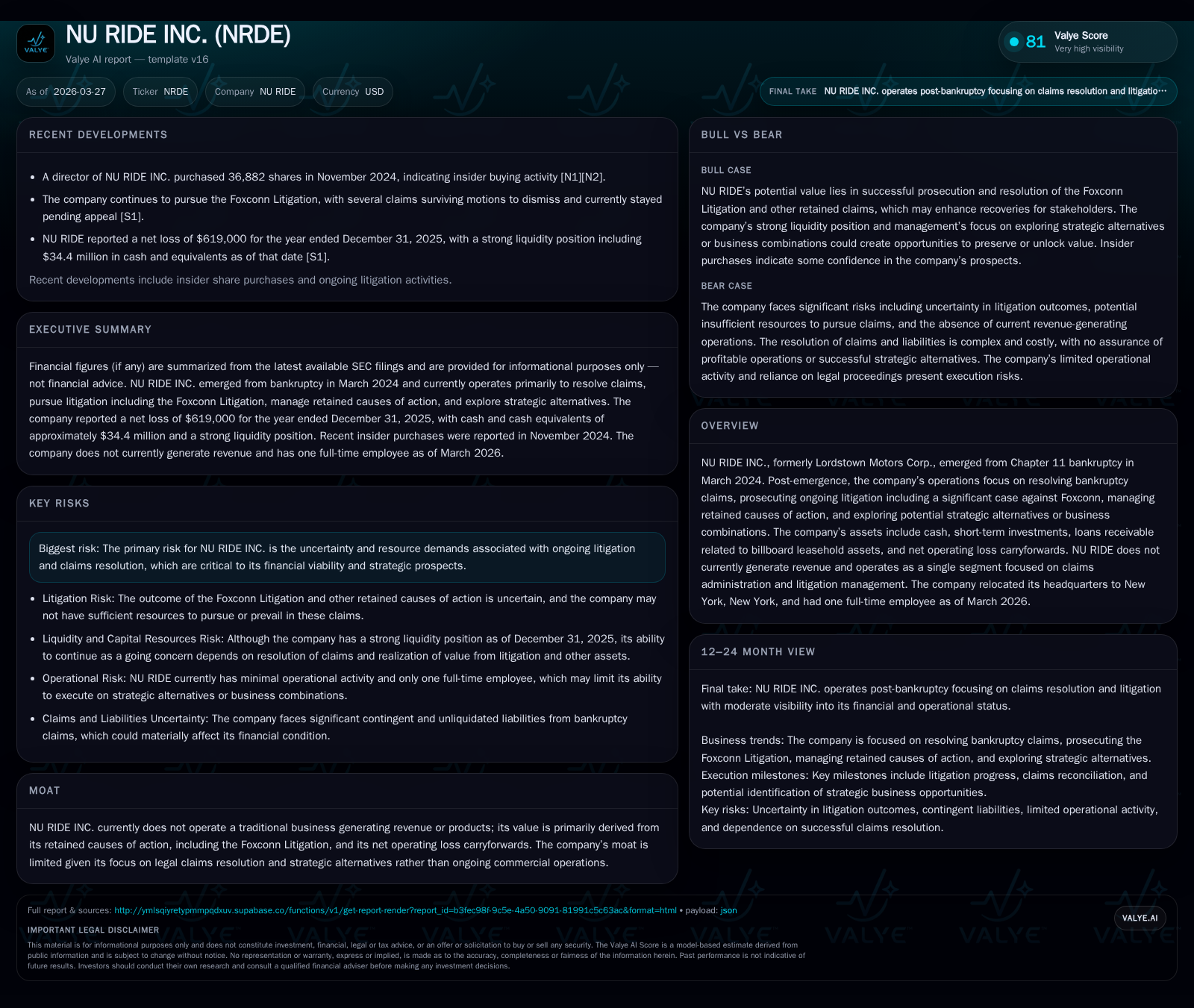

NU RIDE INC.’s Post-Bankruptcy Transition: From Motors to Litigation Management

NU RIDE Inc. has redefined its corporate identity, evolving from a manufacturing enterprise into a litigation-focused entity following Chapter 11 emergence.

After emerging from Chapter 11 bankruptcy in March 2024, NU RIDE INC., formerly Lordstown Motors Corp., shifted away from automotive manufacturing toward managing retained legal claims and exploring strategic alternatives. The company’s financial profile reveals markedly reduced operating losses and controlled expenses alongside ongoing reliance on litigation assets, such as the pivotal Foxconn case, to underpin value. Liquidity remains supported by cash reserves and loans receivable, although risks surrounding insurance coverage denial and litigation uncertainties pose significant challenges. With no revenue-generating business activities, NU RIDE’s near-term trajectory depends heavily on legal outcomes and asset monetization efforts.

From Lordstown Motors to NU RIDE: A Transformative Emergence

Once positioned as an electric vehicle manufacturer under the Lordstown Motors name, the company underwent a radical transformation after filing for Chapter 11 protection in June 2023 [S1][S26]. Emerging in March 2024 as NU RIDE INC., the company discontinued its manufacturing operations entirely. The confirmed bankruptcy plan reoriented NU RIDE toward administration of bankruptcy claims, prosecution of retained causes of action—including significant litigation against Foxconn—and exploration of potential strategic business combinations or alternatives [S1]. This shift repositioned NU RIDE not as an operating business but rather as a steward of legal claims and illiquid assets intrinsic to its restructuring legacy.

Cost Containment and Operating Losses: Quantifying the Trajectory

Financially, this pivot coincides with a dramatic reduction in operating expenditures and losses. Operating income improved substantially, contracting operating losses from $10.9 million in FY2024 to $3.76 million in FY2025—a nearly two-thirds improvement [F1][S1]. This reduction stems chiefly from cutting SG&A expenses nearly in half ($12.9 million down to $6.8 million), driven by lower personnel and professional fees absent accelerated stock-based compensation charges noted in prior years [S1]. Notably, the company incurred no reorganization expenses post-emergence in FY2025 compared to over $4 million in FY2024 related to bankruptcy proceedings [S1]. The narrowing loss profile demonstrates tight cost control focused on maintaining operations essential only to legal claim administration rather than commercial activity.

Legal Claims as Enterprise Assets: The Foxconn Litigation and Beyond

With no revenues or traditional products, NU RIDE’s enterprise value resides predominantly within its retained causes of action [S1]. Central is the ongoing Foxconn Litigation along with various other claims inherited through bankruptcy proceedings [S4][S5]. Such litigation assets require continued substantial professional fees to prosecute yet are often uninsured due to denials rooted in policy exclusions—namely retroactive date exclusions impacting coverage for SEC investigations and shareholder derivative suits [S4][S7]. Consequently, these factors create high uncertainty regarding ultimate recoveries and impose significant costs that could erode liquidity if favorable resolutions are delayed or adverse outcomes occur.

Loans and Strategic Alternatives: Managing Illiquid Asset Exposure

In an effort to generate alternative income streams post-emergence, NU RIDE engaged in several secured loan agreements totaling approximately $7.7 million (sum of $2.215 million loaned to FPI on December 30, 2025 [S18] plus $5.5 million loaned under Loan and Security Agreement with FPII on January 23, 2026 [S3]) collateralized by billboard leasehold assets in Florida. These loans bear interest at 15% per annum payable monthly and include embedded equity interests ranging from approximately 20% to 40%, conditioned on early repayment timing [S18]. While these investments add diversification away from pure legal claims exposure, they represent early-stage illiquid ventures with inherent execution risk given FPI entities’ nascent operational profile [S18]. These arrangements underscore NU RIDE’s attempts at capital preservation via secured lending plus equity stakes albeit outside traditional cash-generating business models.

Assessing Liquidity, Capital Structure, and Cash Flow Dynamics

At December 31, 2025, NU RIDE held $34.4 million in cash and cash equivalents alongside current assets of approximately $44.8 million versus current liabilities under $1 million—yielding an exceptionally strong current ratio around 45:1 supportive of short-term solvency [F1][S6]. However, operating cash flow remained negative at $7.23 million despite improvements relative to the prior year’s $35.1 million outflow [F1][S6]. Absent financing transactions post-emergence highlights a self-financing model reliant on existing liquidity reserves balanced against ongoing costs primarily related to legal prosecutions [F1][S6]. Capital expenditures ceased following manufacturing discontinuation but investment spending remains notable historically due to prior operational fixed asset needs [F1]. Equity shareholders’ deficit persists at about $2.6 million recorded equity with net loss attributable roughly -$0.62 million leading to estimated return on equity near -24% based on latest data [F1], signaling continued erosion despite better cost discipline.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | -7 | -4 | +92.4% | |

| 2024 | -8 | -35 | -11 | 10 | +97.6% |

| 2023 | -343 | -137 | -349 | 10 | -21.5% |

| 2022 | -282 | -214 | -387 | 55 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -23.8 | |

| 2024 | -45 | -120.0 |

| 2023 | -147 | -2532.0 |

| 2022 | -268 | -80.3 |

Source: SEC companyfacts cache [F1].

Operating loss narrowed drastically after bankruptcy emergence reflecting cost-cutting measures.

Risk Landscape: Insurance Coverage Challenges and Litigation Uncertainties

NU RIDE confronts pronounced risk factors centered on denial of insurance coverage for several significant litigations including government investigations and securities class actions arising from pre-bankruptcy disclosures [S4][S5][S7][S14]. Policies excluding coverage for events predating retroactive date have shifted entire cost burdens onto NU RIDE’s balance sheet risking materially increased liabilities outside current accrual estimates [S7]. Moreover, protracted litigation timelines inherently amplify expense uncertainties compounded by complex claims reconciliation processes mandated under the bankruptcy plan [S4][S17][S19]. The existence of substantial unliquidated contingent liabilities further clouds financial prospects while management remains dependent on judicial outcomes which remain unpredictable [S17][S19].

Outlook and Key Milestones: What to Watch Going Forward

While explicit forward guidance is not provided [N/A], critical upcoming developments will hinge on resolution status of the Foxconn Litigation—a principal source driving potential recoveries—and completion of claims reconciliation efforts overseen by the Claims Ombudsman appointed per the Plan [S1][S17][S26]. Parallel pursuits involve evaluating strategic alternatives that may encompass business combinations or asset monetization opportunities; however success remains highly uncertain given diminishing operational scope [S1]. Investors should monitor updates tied to settlements or trial dates linked to core litigations alongside progress deploying loan portfolio yields.

Capital Allocation and Shareholder Returns: A Post-Operating Business Reality

In line with its operational pivot away from revenue generation toward legal claim management, NU RIDE has not declared dividends or pursued buybacks since emergence; capital allocation emphasis lies chiefly on minimizing administrative costs [F1]. Negative net income combined with minimal equity base constrains capacity for shareholder returns presently (ROE near -24%) [F1]. The company’s strategy effectively focuses on capital preservation while awaiting fruition of varied litigation claims or strategic asset dispositions that could someday restore positive returns or fund distributions.

Disclaimer: This analysis is based solely on information available through March 26, 2026. It does not constitute investment advice or recommendations regarding securities associated with NU RIDE INC., nor does it incorporate any non-public information that may exist about the company or its litigations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments