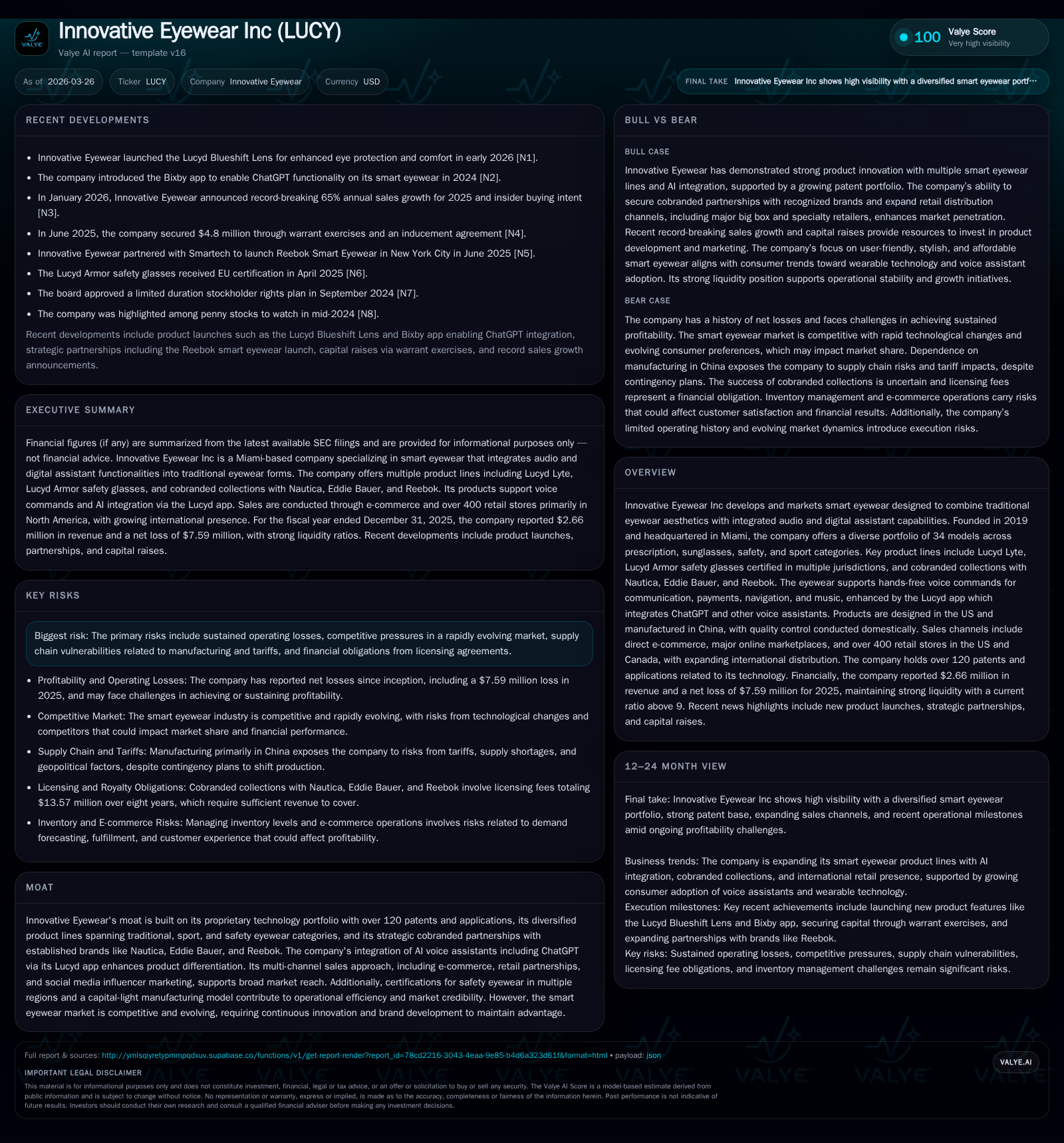

Innovative Eyewear Expands Product Portfolio and Retail Presence Amid Continued Losses

Innovative Eyewear Inc pursues growth through product diversification and channel expansion while managing ongoing operating deficits and supply chain complexities.

Founded in 2019, Innovative Eyewear Inc (LUCY) develops smart eyewear integrating traditional design with digital assistant capabilities, distributing products via over 400 retail stores and multiple e-commerce platforms. Revenue increased from $0.66 million in 2022 to $2.66 million in 2025, driven by product innovation including the Lucyd Armor safety glasses and cobranded collections. Despite revenue growth, the company reported a net loss of $7.59 million in 2025, reflecting investments in product development, marketing, and scaling amid competitive pressures and supply chain risks. Manufacturing is primarily offshore with contingency plans for tariff-related disruptions. The regulatory environment includes FDA device oversight and evolving privacy laws.

Company Overview and Historical Performance

Innovative Eyewear Inc (LUCY), headquartered in Miami and founded in 2019, designs smart eyewear that combines classic styles with integrated audio features and voice assistant technologies [S1][S14]. Its product lineup includes prescription eyeglasses, ready-to-wear sunglasses, sport glasses, and the Lucyd Armor safety glasses certified for multiple international safety standards [S11][S22].

Revenue has grown steadily from $659,788 in FY2022 to $2.66 million in FY2025, reflecting expansion of its product range and increased market penetration supported by cobranded collections launched since early 2024 [F1][S11]. The Lucyd Lyte line remains the core offering since its introduction in 2021.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3 | -8 | -7 | 72513 | +62.6% | +2.3% |

| 2024 | 2 | -8 | -7 | 62203 | +42.0% | -16.6% |

| 2023 | 1 | -7 | -6 | 78463 | +74.7% | -17.3% |

| 2022 | 1 | -6 | -3 | 121561 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -83.7 |

| 2024 | -7 | -85.4 |

| 2023 | -6 | -119.9 |

| 2022 | -3 | -141.2 |

Source: SEC companyfacts cache [F1].

Note: Negative net income reflects ongoing investments; operating cash flow remains negative despite revenue growth[F1].

Business Model & Product Strategy

LUCY targets consumers transitioning from traditional eyewear by emphasizing familiar styles priced comparably with designer glasses [S12][S19]. Frames weigh between one to just under two ounces for all-day comfort with battery lives ranging eight to twelve hours supporting extended use without mid-day recharge [S19].

The company integrates AI voice assistants such as ChatGPT into its Lucyd app ecosystem enabling hands-free interaction for calls and other smartphone functions [S11]. This software-centric approach avoids heavier hardware like cameras or microdisplays that increase cost and reduce wearability [S12].

Manufacturing is outsourced primarily to Chinese factories for cost efficiency combined with domestic quality control before distribution [S18]. In response to tariffs introduced in April 2025 amounting to up to approximately 27.5%, LUCY expanded fulfillment centers internationally and maintains contingency plans for alternative sourcing from Taiwan or Vietnam [S5][S9].

Sales Distribution & Marketing Channels

The company employs a multi-channel approach including:

- Direct e-commerce via Lucyd.co offering customized prescription options.

- Online marketplaces such as Amazon.com and others including Walmart.com and Target.com [S17][S21].

- Over 400 physical retail stores across North America including independent optical retailers and chains like Best Buy and Dick’s Sporting Goods [S6][S18].

- Safety eyewear distribution through partnerships with home improvement retailers (Home Depot) and PPE distributors (Grainger) leveraging ANSI/CSA/EN ISO certifications for the Lucyd Armor line launched late 2024 [S6][S18].

- Social media marketing supported by influencer collaborations and affiliate programs driving community engagement [S11][S17].

Marketing campaigns are segmented by verticals targeting daily wear users needing AI functionality; sun/sport lines for active lifestyles; and safety products for industrial users requiring certified protection [S11].

Intellectual Property & Competitive Positioning

LUCY holds over 120 patents central to its technology platform covering frame designs and software integration modules . The competitive landscape includes large players such as Ray-Ban with greater resources and brand recognition [S10][S24]. The company competes mainly in audio-enabled smart glasses against some camera-enabled devices but prioritizes accessible fashion-forward form factors over hardware-heavy devices that may hinder adoption due to complexity or cost [S13][S24].

Supply chain reliance on contract manufacturers exposes risks related to tariffs and international trade uncertainties requiring active mitigation efforts [S18][S20][S9].

Financial Performance & Capital Allocation

Despite robust revenue growth (+62.6% YoY for FY25), LUCY continues operating at significant net losses ($7.59 million FY25), similar in magnitude to prior years [F1]. Operating cash flow remained negative at $7.28 million in FY25 reflecting investments essential for scaling sales efforts and research & development. Capital expenditures were modest at about $72K annually consistent with a capital-light manufacturing model [F1].

Equity capital rose moderately to approximately $9 million by end-FY25 through equity financings supporting operations due to lack of profitability so far [F1][S16]. Approximate return on equity stands near -84%, indicating current unprofitability relative to invested shareholder equity.

The company does not pay dividends or repurchase shares prioritizing reinvestment into growth initiatives amid competitive dynamics [F1]. Licensing obligations related to cobranded collections carry payment commitments totaling $13.57 million over eight years which may affect future margins if revenue growth does not keep pace [S27].

Risks & Regulatory Environment

Key risks include:

- Ongoing losses without clear path to profitability amid competition from larger incumbents with greater resources [S3][S10][S24].

- Exposure to tariffs on Chinese imports causing cost pressures despite mitigation measures; supply disruptions could impact customer fulfillment adversely affecting reputation [S9][S18][S20].

- FDA medical device regulations impose manufacturing compliance requirements potentially impacting production timelines or sales authorizations [S4][S27].

- Privacy regulations including CCPA/CPRA impose legal compliance costs related to user data collected via the Lucyd app encompassing health information [S4][S15].

- Litigation risks tied both to intellectual property enforcement and possible third-party claims present costly uncertainties that may divert management focus or result in settlements [S25][S26].

Outlook & Monitoring Criteria

Growth prospects depend on broadening mass-market adoption by converting traditional eyewear users through fashion-forward designs paired with embedded AI voice assistants enhancing user experience [N summary; S22]. Trends favoring wearable tech convergence support potential expansion opportunities.

Key factors to watch include:

- Ability to scale production while maintaining quality amid manufacturing dependencies.

- Success of cobranded collections generating incremental revenues sufficient to offset royalty expenses.

- Margin resilience amid evolving tariff environments.

- Access to capital resources enabling sustained marketing investments without excessive dilution.

- Regulatory developments affecting medical device classification impacting time-to-market.

Conclusion

Innovative Eyewear shows promise through diversified smart eyewear offerings distributed via expanding e-commerce platforms complemented by growing physical retail presence including industrial PPE channels enabled by certification milestones. However persistent unprofitability driven by operational expenditure necessary for mainstream consumer adoption alongside complex regulatory landscapes creates challenges. Supply chain vulnerabilities particularly tariff exposure require ongoing vigilance.

Success will hinge on translating expanding market awareness fueled by patented technologies coupled with AI-enhanced software into scalable revenues exceeding licensing costs while managing global manufacturing complexities efficiently enough to progress toward long-term profitability.

This report is based exclusively on publicly filed documents as of March 26th, 2026 and does not constitute an offer or recommendation regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments