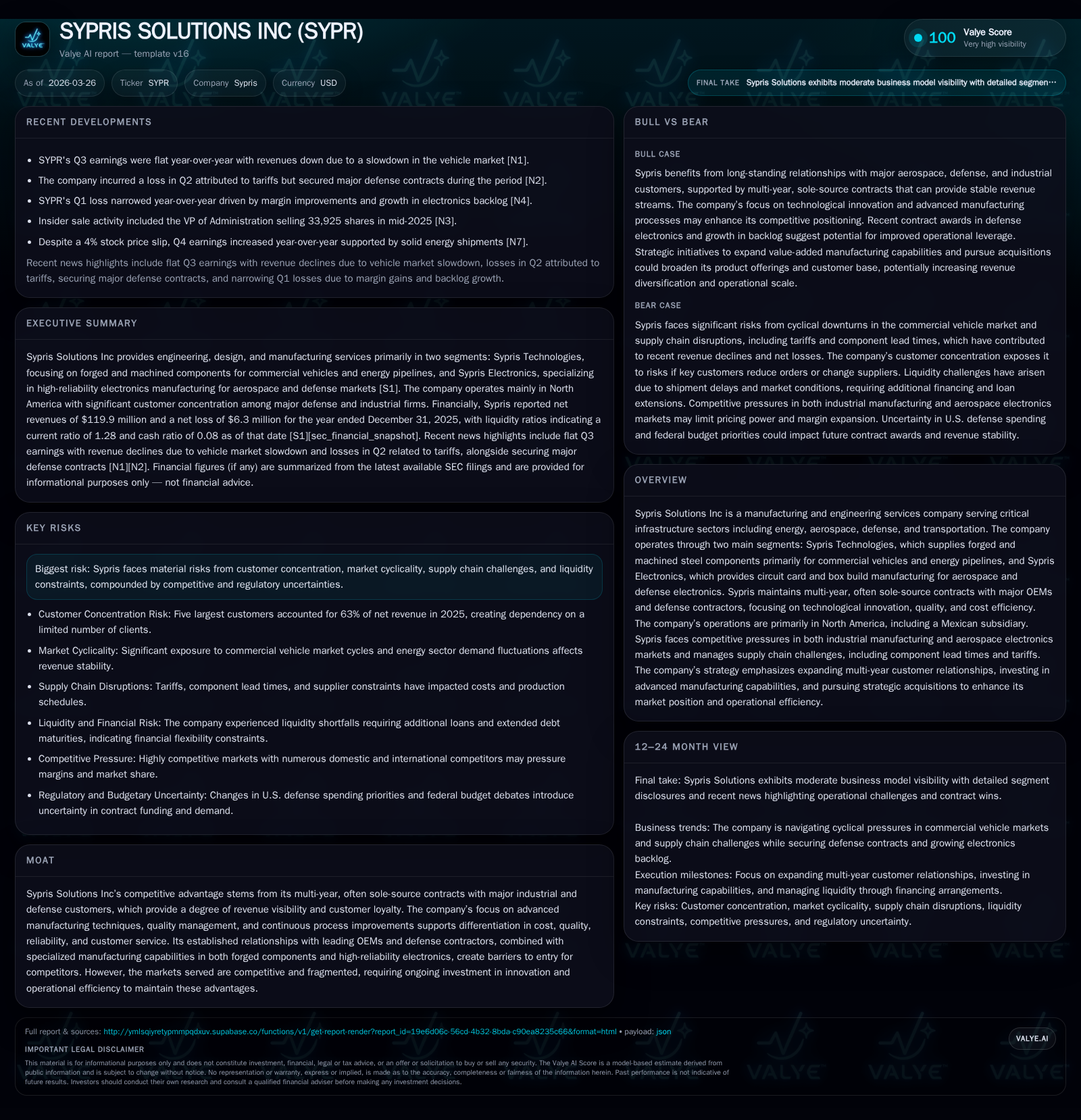

Sypris Solutions Endures 2025 Revenue Decline and Operating Loss Amid Market Cyclicality and Supply Challenges

The company’s segmented exposure to cyclical commercial vehicle markets and defense electronics shapes both growth prospects and financial volatility.

Sypris Solutions, Inc. reported a 10.4% revenue decline to $119.9 million in 2025 with an operating loss of $6.6 million, reversing prior years’ modest profits. The downturn was driven by a significant drop in the North American Class 8 truck market, affecting Sypris Technologies, coupled with supply chain disruptions delaying aerospace and defense electronics shipments within Sypris Electronics. Although the company holds multi-year sole-source contracts that provide some visibility, its concentrated customer base and exposure to macroeconomic pressures—including inflation and geopolitical tensions—pose ongoing risks. Liquidity challenges prompted additional related-party financing and deferred interest payments, while management focuses on operational improvement, enhanced contract wins, and new value-added manufacturing capabilities for future growth.

Company Overview

Sypris Solutions Inc serves critical infrastructure sectors spanning energy pipelines, heavy commercial vehicles, aerospace, defense electronics, and transportation through two distinct segments: Sypris Technologies and Sypris Electronics [S1][S9]. The company emphasizes long-term strategic partnerships often secured via sole-source multi-year contracts with key OEMs and government agencies that create barriers to entry based on advanced manufacturing capabilities and strict quality standards.

Historical Performance Highlights

Sypris experienced considerable top-line volatility over the past decade with peaks above $350 million in 2014 followed by steady contraction culminating in $119.9 million revenue for fiscal 2025—a decline of approximately 10.4% from $140.2 million in 2024 [F1]. This decline marks a reversal after modest revenue stabilization post-2020.

Operating results deteriorated sharply to an operating loss of $6.6 million in 2025 from operating income of $2.9 million in the prior year [F1]. Similarly, net losses widened to $6.3 million compared to a loss of $1.7 million in 2024 [F1]. The swing is attributable largely to volume declines amidst fixed-cost operation leverage.

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -6 | -6 | -7 | 1 | -277.3% |

| 2024 | -2 | 2 | 3 | 1 | -5.3% |

| 2023 | -2 | -11 | 1 | 2 | +36.0% |

| 2022 | -2 | 14 | 0 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -35.6 |

| 2024 | 1 | -8.6 |

| 2023 | -13 | -7.1 |

| 2022 | 11 | -12.7 |

Source: SEC companyfacts cache [F1].

Operating cash flow also declined markedly turning negative by $5.7 million in 2025 from positive $2 million in 2024; after capex ($0.76 million), free cash flow was approximately negative $6.5 million [F1]. These figures underscore working capital strains due to extended aerospace contract shipment delays within Sypris Electronics as well as cyclical volume drops impacting Sypris Technologies.

Segment Performance Drivers

Sypris Technologies:

This segment focuses on forged, machined steel components mainly for heavy commercial vehicles (Class 8 trucks) and energy pipelines [S1][S24]. The North American Class 8 truck production declined by about 24% year-on-year into 2025 causing sizeable volume contraction for Sypris given its industrial customer base that includes Detroit Diesel, PACCAR, Volvo, among others [S1][S21]. However, diversification efforts towards automotive, sport utility vehicles (SUVs), off-highway vehicles as well as oilfield Tube Turns® partly mitigated volatility [S1].

The oil & gas-related Tube Turns® product line faces uncertainty due to geopolitical issues (Middle East conflicts, Russia-Ukraine war), inflationary cost environment and evolving regulatory frameworks [S1]. These factors have affected capital spending patterns of exploration companies.

Sypris Electronics:

Accounting for approximately 57% of total revenues in 2025 ($68.1 million), this segment provides circuit card assemblies, box builds, high reliability manufacturing mainly for aerospace and defense prime contractors such as Northrop Grumman [S8][S22]. It has largely operated under sole-source multi-year contracts sustaining revenue visibility.

However, supply chain constraints caused delays in deliveries which significantly affected working capital by slowing inventory conversion into cash during prior years’ periods [S7][S15][S23]. Despite this disruption, aerospace/defense electronic demand remains strong amid ongoing US government investment priorities.

Customer Concentration & Geographic Exposure

Top customers accounted for a substantial portion of revenues: Northrop Grumman (23%), Detroit Diesel (13%), SubCom (~11%) combined constituted nearly half of net revenues in 2025 [S4][S18]. This concentration creates significant revenue dependency risks should any large client change sourcing strategies.

Operations are centered geographically in North America with notable manufacturing presence through a Mexican subsidiary which delivered roughly one-quarter of consolidated revenue but swung from profits in earlier periods to marginal losses recently reflecting operational challenges there [S5][S19]. Currency fluctuations remain muted given most transactions are USD-denominated.

Financial Position & Capital Allocation

As of December 31, 2025, Sypris held roughly $6.8 million cash against current liabilities exceeding $62 million yielding a current ratio near 1.28x—indicating tight liquidity but manageable short term coverage [F1][S19].

The company faced liquidity pressures triggered by volume declines and supply chain-induced working capital surges dating back to late-2023 continuing into early-2026 [S7][S15]. This compelled issuance of additional secured promissory notes totaling $12 million from Gill Family Capital Management (GFCM), an entity controlled by company insiders—extensions on maturities reaching April 2030 were implemented along with interest payment deferrals allowing cash conservation [S7][S10][S16][S20].

Capital expenditures remain modest relative to depreciation supporting lean Capex discipline ($0.76M in FY25 vs over $1M prior years) reflecting focus on incremental productivity improvements rather than asset-expanding investments [F1]. No dividends or share repurchases occurred over recent years indicating prioritization of operational stability.

Forward-Looking Considerations

Management acknowledges prevailing economic headwinds including inflationary input costs across raw materials such as steel—critical for forging operations—alongside logistics and labor cost increases impacting margins despite pricing adjustments and lean initiatives [S1][S8].

The cyclical nature of Class 8 truck demand suggests near-term volume pressure may persist but industry forecasts predict gradual recovery starting late-2026 extending into a more robust rebound by FY28 allowing Sypris Technologies potential topline stabilization [S1].

Simultaneously, defense-sector spending continuity coupled with new program awards offers runway for growth within Sypris Electronics; however ongoing component lead time issues necessitate sustained coordination with suppliers and customers particularly due to sole-source dependencies for certain parts [S16][S24]. Preserving these exclusive relationships will be critical to sustaining the company’s competitive position.

Strategic aims include increasing multi-year customer partnerships focused on contract longevity and innovation-driven cost reduction efforts including adoption of advanced manufacturing techniques like Six Sigma quality control measures and continuous-flow methodologies which are sector-preferred efficiency drivers [S13][S24].

Risks Summary

Risks stem from customer concentration intensity making revenue streams vulnerable, natural cyclicality inherent within heavy commercial vehicle markets, going supply chain challenges especially impacting aerospace electronic assembly programs, and liquidity constraints evidenced by reliance on related party financing which may limit future capital flexibility [S26]. Regulatory shifts especially relating to defense procurement policies also loom as an uncertainty factor given evolving federal budget dynamics stated at length by management without precise forecast clarity [S21].

Conclusion

Sypris Solutions operates at the intersection of industrial manufacturing cyclicality and specialized aerospace-defense electronics production requiring adaptation amid economic headwinds compounded by high customer concentration risk profile. The pronounced dip in revenues and reversion to operating losses in fiscal year 2025 primarily reflect external sectoral softness particularly within heavy-duty truck demand alongside ongoing execution challenges around supply chains within electronics.[N1]

While the company benefits from unique contractual structures granting partial revenue visibility thanks to long-term sole-source arrangements across its segments—the extent of macroeconomic uncertainty warrants cautious observation focused on signs of sustained booking momentum from defense-related programs alongside improvements in working capital efficiency.

Liquidity remains manageable but constrained; balance sheet support from insider financing underscores necessity for tight operational cash management going forward.

Investors who follow industrial-supply chains or aerospace-defense manufacturing sectors will find Sypris illustrative of mid-sized firms navigating persistent competitive pressure through targeted value creation while grappling with structural market cyclicality plus short term execution variables.

Disclaimer: This analysis reflects information available as of March 26th, 2026 extracted solely from cited SEC filings ([F1],[S#]) and referenced news sources ([N#]). It is intended exclusively for informational purposes without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments