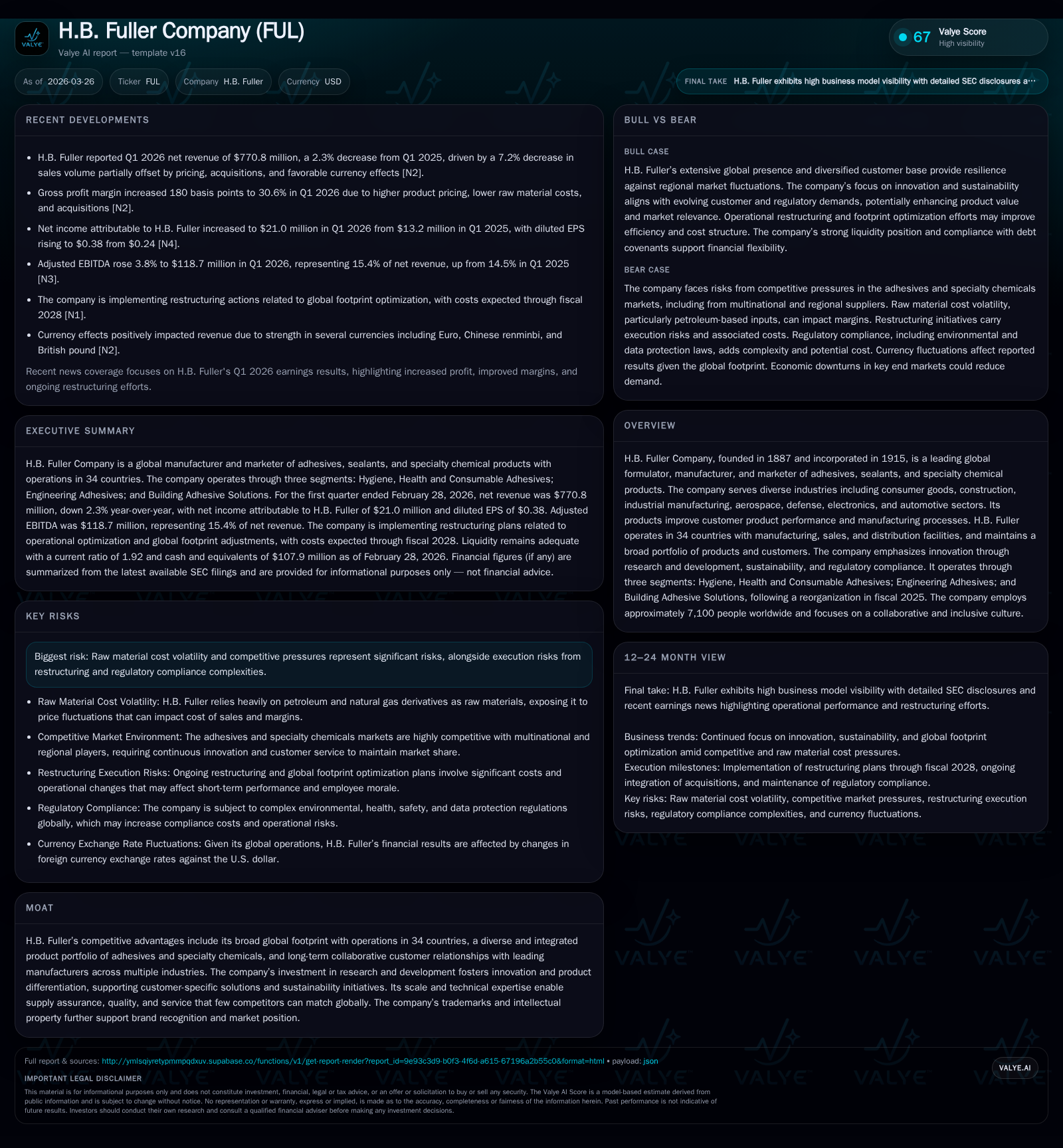

H.B. Fuller’s Evolving Adhesives Portfolio Drives Earnings Amid Restructuring and Market Pressures

The firm's strategic segment reorganization and innovation initiatives underpin earnings growth amid ongoing raw material cost volatility and restructuring expenses.

H.B. Fuller experienced a modest decline in revenue in fiscal 2025 driven by volume pressures and currency headwinds, yet expanded its gross margin through pricing power, lower raw material costs, and restructuring gains. The company’s 2025 segment realignment consolidated its Building Adhesive Solutions unit following the divestiture of its North America Flooring business, aiming to enhance operational efficiency. Despite a roughly 3 percent revenue drop year-over-year, net income rose by over 16 percent on improved product mix and cost controls. Raw material exposure remains high with about 75 percent of costs linked to petroleum derivatives, while foreign exchange fluctuations negatively impacted revenues by approximately $20 million last year. H.B. Fuller's global footprint, broad product suite including pressure-sensitive adhesives, and R&D-driven innovation remain key competitive advantages as it implements further restructuring through 2028. Capital allocation reflects a disciplined approach balancing dividends and increased share repurchases alongside investments in growth and operational optimization.

Historical Performance: Revenue Challenges Offset by Margin Expansion

H.B. Fuller's financials in fiscal 2025 illustrate a nuanced balance between top-line pressure and profitability gains. Total net revenue decreased approximately 3.8% year-over-year with sales volumes declining around 0.8%, acquisitions/divestitures accounting for a negative impact of about 2.1%, and foreign currency effects detracting roughly 0.6%. These declines were partially offset by increased product pricing of approximately 0.8%, emphasizing the company's ability to pass cost pressures onto customers during a challenging macro environment [F1][S1].

Despite softer revenues near $2 billion, gross profit margin expanded notably from 29.8% in 2024 to 31.1% in 2025 supported by formulation innovation enabling better pricing power, lower feedstock costs given softening petroleum prices versus prior periods, and benefits from the ongoing restructuring program that has streamlined operations [S1]. This upward shift in margin contributed materially to net income increasing by over 16% to $152 million with diluted EPS rising from $2.30 to $2.75 [F1][S1]. Operating income showed slight pressure but remained resilient due to these margin improvements.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 152 | 263 | 142 | +16.7% | |

| 2024 | 130 | 302 | 348 | 139 | -10.1% |

| 2023 | 145 | 378 | 355 | 119 | -19.6% |

| 2022 | 180 | 257 | 323 | 130 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 50 | 61 | 121 |

| 2024 | 48 | 40 | 163 |

| 2023 | 43 | 3 | 259 |

| 2022 | 39 | 4 | 127 |

Source: SEC companyfacts cache [F1].

Note: Data reflects annual trends; some prior years omitted if incomplete.

Operational Restructuring: Strategic Segment Reorganization and Cost Optimization

In fiscal year 2025, H.B. Fuller implemented a strategic reshaping of its operating segments aimed at optimizing focus areas while divesting less aligned assets. The North America Flooring business was sold off from the Construction Adhesives segment — this move yielded a leaner portfolio better focused on core competencies [S1]. Concurrently, three prior segments were consolidated into three new ones: Hygiene, Health and Consumable Adhesives; Engineering Adhesives; Building Adhesive Solutions.

Building Adhesive Solutions combines the previous insulating glass, woodworking composites (formerly part of Engineering Adhesives), commercial roofing systems and infrastructure businesses (previously under Construction Adhesives). This unification streamlines management oversight for sectors reliant on building envelope sealing technologies and infrastructure adhesives widely used in roads/highways and HVAC applications [S1].

Restructuring expenses recognized totalled about $83 million during prior phases with an additional $4.8 million incurred through Q1 FY2026 as new global footprint optimization actions began rolling out [S2]. These remodeling efforts are projected to complete only by FY2028 due to their extent but have already driven efficiency gains reflected in margin improvements despite short-term cash flow pressure.

Raw Material & Currency Impacts: Navigating Input Costs in a Global Footprint

Raw materials represent approximately three quarters of H.B Fuller's cost structure, predominantly depending on derivatives of crude oil and natural gas feedstocks such as polymers essential for adhesive formulations [S1]. Volatility in petroleum-based inputs exposes the company materially to fluctuations in global commodity supply-demand dynamics impacted seasonally or unexpectedly by events like hurricanes that disrupt production.

Currency translation risk is another sizable factor given that roughly half the company's revenues originate outside the United States across Europe, Asia Pacific, Latin America, India, Middle East and Africa [S1][S22]. Key currency exposures involve Euro, Chinese renminbi, British pound sterling among others—a mixed basket where movements can either dilute or inflate reported U.S.-dollar results.

In calendar year 2025 alone, adverse currency shifts contributed nearly a $20 million drag on net revenues owing mostly to foreign currencies weakening against the dollar despite some offsets from natural hedges via matched non-functional currency assets/liabilities or derivative instruments intended for transactional risk mitigation [S1][S2]. Sensitivity analyses indicate that a hypothetical one-percent change in foreign exchange rates could impact net income by roughly $9 million—highlighting ongoing vigilance required for FX risk.

Segment-Level Drivers: An Integrated View of Hygiene, Engineering, and Building Adhesive Solutions

The Hygiene, Health and Consumable Adhesives segment caters primarily to growing nonwoven markets such as hygiene products (diapers and wipes), packaging assembly lines employing pressure-sensitive adhesives for labeling or flexible packaging film lamination where bond strength matters under variable environmental conditions [S1][F1].

Engineering Adhesives is concentrated on high-value sectors requiring performance-grade bonding technologies—including aerospace composites assembly requiring thermal-resistant adhesives or electronics encapsulation adhesives critical for clean energy devices like solar panels or EV components.

Building Adhesive Solutions encompasses specialty products used extensively across roofing membranes involving tapes/sealants enabling weatherproof installations; commercial building envelope sealants addressing energy efficiency needs; as well as roadway infrastructure bonding materials vital for heavy civil construction projects including LNG plants—all benefiting from evolving polymer chemistry advancements for durability [S1][F1].

Each segment leverages H.B Fuller's technical expertise driving formulation innovation tailored precisely toward customer-specific manufacturing process enhancements while complying with stringent sustainability benchmarks increasingly demanded globally.

Outlook and Growth Prospects: Opportunities Amid Constraints

While explicit formal forecasts are not published beyond regulatory filings guidance extracts, recent earnings commentary suggests several key areas influencing growth trajectories over the medium term:

- Continued execution of restructuring plans expected through FY2028 aims to unlock operating leverage advancing margin expansion prospects despite anticipated incremental restructuring charges [N1][N2][S2].

- Raw material feedstock costs remain monitored closely amid evolving crude oil market scenarios; however recent downward trend aided cost containment efforts including supplier contract negotiations.

- Pricing capabilities supported by brand recognition alongside differentiated product offerings position H.B Fuller well against competitive pressures within selected end-markets.

- Geographical diversification provides resilience but also necessitates effective currency risk management strategies with emerging market exposure weighed carefully.

- Innovation pipeline linking adhesive chemistry improvements with sustainability initiatives—such as biodegradable polymers or reduced-VOC formulations—could provide entry points into expanding green construction segments or next-generation packaging solutions.

Overall growth may be constrained short term by economic uncertainties impacting discretionary consumer goods demand yet offset partly through industrial capital expenditure recovery phases especially infrastructure investment cycles supporting Building Adhesive Solutions demand.[N2]

Capital Allocation Priorities: Returns through Dividends and Share Repurchases

H.B Fuller exhibits disciplined capital deployment balancing shareholder returns with reinvestment needs amid transformation efforts:

- Dividend payments steadily increased over recent years totaling approximately $50 million in fiscal year 2025 corresponding with an annualized dividend per share increase from $0.856 in FY2024 to $0.928 in FY2025 highlighting commitment toward reliable income streams for shareholders [F1][S19].

- Share repurchase programs accelerated significantly during FY2025 with buybacks exceeding $60 million compared to $39 million prior year indicating proactive capital return policies when share price levels permit attractive repurchase opportunities aligned with financial flexibility goals [F1][S26].

- Operating cash flow generation stood strong albeit down roughly 12.9% year-over-year at $263 million partly influenced by working capital shifts coinciding with operational changes; capex stayed relatively stable near $142 million focusing on capacity maintenance plus selective expansion supportive of innovation strategy.

- Approximate return on equity is around 7.6% derived from FY2025 net income relative to equity base reinforcing moderate profitability relative to invested capital levels [F1].

Hence capital priorities appear calibrated toward sustaining dividend growth bolstered by opportunistic buybacks while preserving adequate liquidity to fund continued restructuring efforts plus organic innovation investments.

Key Metrics to Monitor: Margins, Pricing Power, and Restructuring Execution

Looking forward investors should track quarterly developments across several metrics signaling operational progress including:

- Adjusted EBITDA trends which incorporate non-GAAP adjustments reflecting improved earnings quality particularly post-restructuring milestones completion timelines referenced through FY2028 periods [N3][S2].

- Gross margins movement evidencing ability to sustain price mix gains while offsetting raw material volatility inherent within adhesive chemical supply chains.

- Organic revenue comparisons dissecting volume versus pricing contributions offering insight into end-market demand strength versus input cost pass-through effectiveness.

- Timing and magnitude of remaining restructuring expense realization impacting near-term profitability alongside net cash flow draws or savings achievements.

- Foreign currency exchange rate impacts affecting translation sensitivities notably relative weighting shift among European vs Asian currency exposures needing continual hedging assessment consistency.

Systematic evaluation of these indicators will clarify if H.B Fuller successfully balances medium-term earnings quality enhancement alongside top-line stability restoration amidst sector cyclicality challenges.

This report is intended solely for informational purposes based on publicly available data as of March 26, 2026; it does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments