ELTEK’s Capacity Expansion Drives 11% Revenue Growth but Compresses Margins in 2025

The company advances high-end flex-rigid PCB production amid rising costs and geopolitical risks.

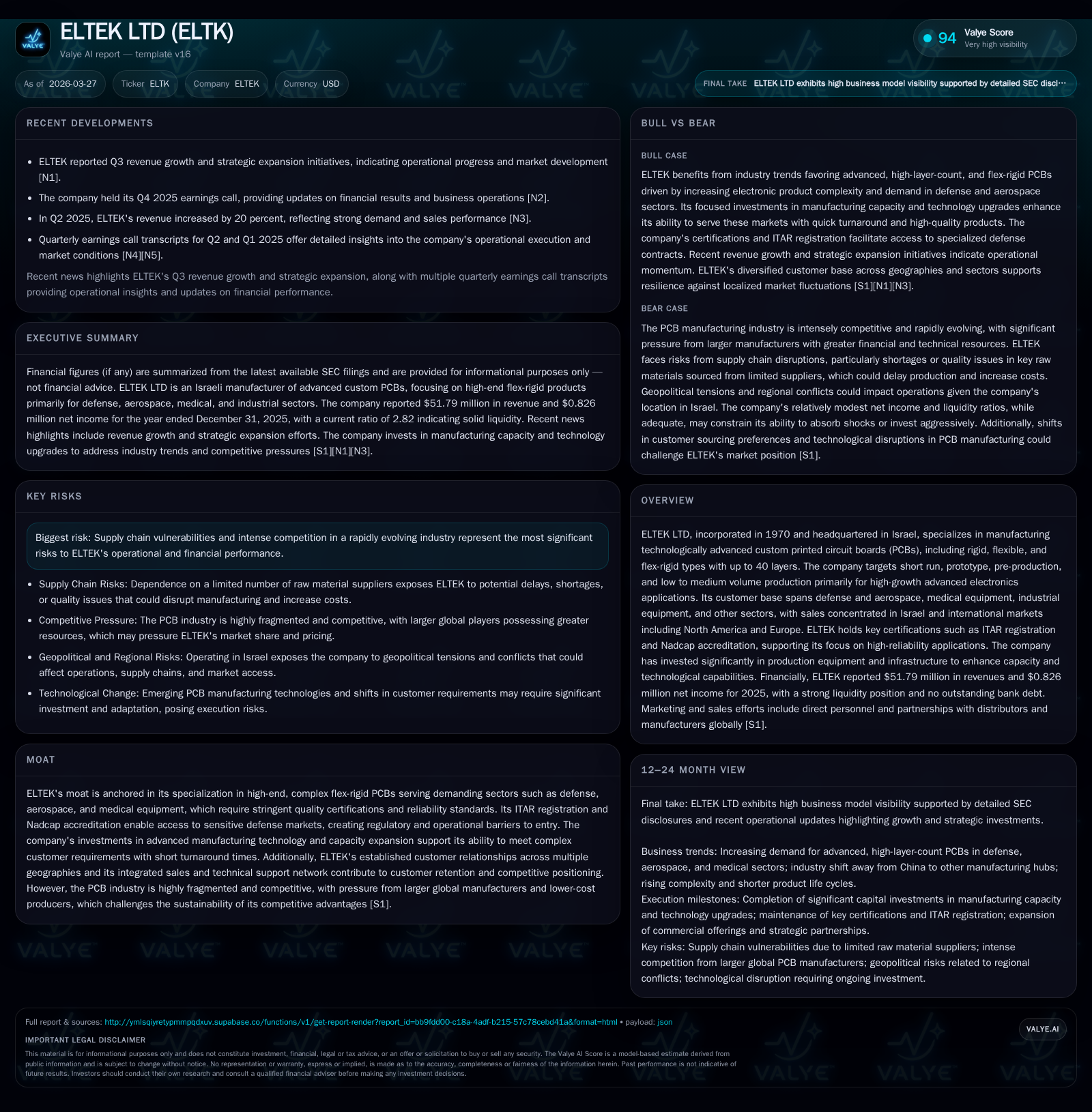

ELTEK LTD, a niche player in sophisticated printed circuit boards (PCBs), reported an 11% revenue increase to $51.79 million in 2025, supported by investments in capacity expansion and strong demand from defense and medical sectors. However, operating profit declined by over 46%, driven by higher employee costs, production inefficiencies linked to ongoing plant upgrades, and adverse currency movements. The company faces supply chain vulnerabilities and competitive pressures from Asian manufacturers while maintaining a healthy balance sheet with no outstanding bank debt. Looking ahead, ELTEK plans $5 million capex in 2026 aiming to further enhance manufacturing capabilities, with close attention warranted on operational efficiency and market penetration in sensitive defense applications.

Company Overview

Founded in 1970 and headquartered in Israel, ELTEK LTD specializes in technologically advanced custom PCBs primarily for markets requiring high reliability such as defense, aerospace, medical equipment, and industrial applications [S1]. ELTEK's product portfolio emphasizes short-run and prototype production of complex rigid, flexible, and flex-rigid PCBs up to 40 layers deep, catering largely to high-growth electronics segments that demand rapid turnaround times [S1]. The firm's ability to manufacture these specialized boards is supported by certifications including ITAR registration—which permits participation in sensitive U.S. defense supply chains—and Nadcap accreditation tied to aerospace industry quality standards [S9][S13].

ELTEK operates principally out of its Israeli manufacturing facility along with marketing subsidiaries including Eltek USA to target North American customers [S1][S8]. Its business model includes direct sales staffs supplemented by local representatives across Europe and Asia [S8][S9]. With around 175 employees at end-2025 [F1], the company has systematically expanded production capacity via heavy investment in new machinery and infrastructure over recent years.

Historical Financial Performance

Over the past four years (2022-2025), ELTEK has demonstrated top-line growth fueled by elevated customer demand primarily from defense-related sectors combined with increased operational capacity enabled by capital expenditures:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 52 | 1 | 1 | 2 | +11.3% | -80.4% |

| 2024 | 47 | 4 | 5 | 4 | -0.4% | -33.5% |

| 2023 | 47 | 6 | 9 | 7 | +17.8% | +98.9% |

| 2022 | 40 | 3 | 4 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1276000 | -4 | 1.8 |

| 2024 | 0 | -5 | 10.3 |

| 2023 | 1321000 | 6 | 23.6 |

| 2022 | 994000 | 1 | 15.2 |

Source: SEC companyfacts cache [F1].

Table shows financial results sourced from SEC filings (20-F for fiscal years ended Dec-31) compiled by companyfacts snapshot [F1].

Notably, despite robust revenue growth averaging mid-teens percentage gains since fiscal year end-2022—primarily driven by rising demand for flex-rigid PCBs in defense and aerospace—the company’s profitability metrics have shown considerable volatility.

Operating income peaked at $7.3 million in FY23 before retreating sharply by nearly half in FY24 to $4.39 million; FY25 saw an even steeper roll-back to $2.35 million [F1]. This trend mirrors net income fluctuations which more than halved year-over-year from $4.22 million in FY24 down to under $1 million last fiscal year [F1]. The contraction arises largely due to increasing production costs correlated with labor expenses, inefficiencies introduced by ongoing capacity expansions, plus exchange rate impacts given ELTEK’s operations are Israeli shekel–based but financials reported in dollars [S16].

Cash flow data corroborates margin compression: operating cash flow dropped dramatically from $8.86 million in FY23 down to $1.15 million last year after outlays exceeding $5 million on capital expenditures aimed at enhancing manufacturing technologies [F1][S16][S23]. This cash crunch underscores the transitional cost burden associated with investments aiming at mid-term scalability.

Dividends resumed modestly at $1.28 million in FY25 after a pause in FY24 indicating some shareholder return even as earnings softened [F1].

Drivers of Past Growth & Operational Dynamics

The historical revenue growth was largely powered by:

- Strong Demand from High-Barrier Sectors: Defense & aerospace accounted for

73% of PCB production revenues last fiscal year (up from ~65% the prior year) providing resilient sales even amid broader macroeconomic uncertainty [S13]. Medical equipment (7%) and industrial segments also supplied steady demand. - Capacity Expansion: A focused capital expenditure program totaling approximately $17 million over three years increased production capability enabling fill rates for larger or more complex orders though causing temporary output inefficiencies during installations [S16][S23].

- Certification Advantages: ELTEK's ITAR registration since early ‘09 enables participation in regulated U.S.-defense projects while Nadcap accreditation confirms adherence to rigorous aerospace quality systems that competitors struggle to match [S9][S13].

- Geographic Diversification: Israeli customers dominate sales (~68%), but international clients contributed about one-third of revenues spanning North America, Europe (notably Netherlands & Italy), India, and other regions for broader market exposure albeit with variable contribution levels [S6][S8][F1].

Challenges included:

- Production Inefficiencies During Plant Upgrade: Temporary relocation within the factory caused disruptions affecting margins notably during FY25 [S16].

- Currency Volatility Impact: Devaluation of dollar relative to NIS disadvantaged reported dollar earnings despite stable operational performance domestically given NIS is functional currency [S16].

- Rising Employee Compensation Costs: Wage inflation pressured gross margins particularly acute within Israel’s tight skilled labor market segment supporting PCB manufacturing.

Future Growth Prospects & Outlook

Potential Growth Drivers:

- Continued Investment in Manufacturing Technology: ELTEK signaled expectations to invest approximately $5 million again during FY26 primarily targeting equipment upgrades aimed at capacity scaling as well as improving process efficiencies [N1][S16][F1].

- Growing Defense Budgets & Aerospace Renewed Demand: Heightened geopolitical tensions have resulted in increased orders consistent with ongoing enhancements of military hardware globally fostering uplift demand for sophisticated PCBs integrated into electronic warfare systems, avionics, missile guidance, etcetera [S18].

- Expansion into Commercial Markets: While still defense-heavy currently (~73%), targeted efforts since recent years on medical devices and industrial equipment segments provide diversification potential possibly reducing cyclicality risk inherent in defense spending cycles [S13].

- Leveraging Quality Certifications & Export Approvals: ELTEK's ITAR status positions it uniquely among Israeli PCB suppliers able to service critical U.S defense contractors; sustaining these certifications could open incremental contracts [S13].

- Strategic Partnerships & Outsourcing Facilitation: The company has been forming alliances with far eastern manufacturers since around FY21 allowing selective sourcing strategies balancing proprietary manufacturing with outsourced volume runs ensuring flexibility against cost competition [S9].

Constraints & Risks:

- Supply Chain Vulnerabilities: Dependency on limited raw material suppliers—copper laminates, prepregs etc.—carries risk if shortages or quality issues arise disrupting delivery schedules especially under global logistics turmoil continuing post-pandemic effects [S9][S18].

- Competitive Pressures From Low-Cost Producers: Asian giants including Indian and South Korean manufacturers offer lower prices potentially capturing share especially outside tightly controlled defense niches requiring certification adherence where ELTEK excels [S10][S11].

- Operational Disruptions From Environmental Compliance: Pending soil contamination investigations and environmental penalties pose compliance risks that may impact operations or add unforeseen costs related to remediation or permit controls set forth by Israeli authorities currently under review with hearings expected later this year [S19][N2].

- Currency Exchange Exposure: Continued fluctuations between NIS/USD create unpredictability impacting reported earnings given mismatch between operating currency base (NIS) versus reporting currency (USD) [S16].

What To Watch Forward (Analysis):

- Quarterly updates on progression towards efficient use of newly installed equipment would be critical given prior year's inefficiency hit margins significantly.

- Customer order trends particularly international defence contracts could be early indicators of sustained underlying demand.

- Environmental regulatory outcomes scheduled for hearings this spring remain material potential disruptors or cost additions.

- Dollar/NIS exchange rates should be monitored closely influencing earnings translation.

Returns & Capital Allocation

ELTEK's return profile displays challenges linked mainly to margin pressure amid ongoing investments:

- Approximate Return on Equity (ROE), calculated as net income divided by average equity stood near a low ~1.8% for FY25 reflecting tight profitability despite healthy equity base growth related primarily to equity injections including public offerings since FY23 [F1].

- Operating cash flow after deducting capital expenditures reveals negative free cash flow position (approximately -$4.2 million), highlighting heavy reinvestment phase although part mitigated by increased dividend payout resuming at $1.28 million after skipping FY24 [F1].

- No bank debt outstanding at end-FY25; access remains via revolving credit lines providing financial flexibility unencumbered by significant leverage constraints [S7][F1].

Historically dividends were modest but consistent when profitable; management appears balancing between shareholder returns while prioritizing strategic reinvestment into capacity expansion given strong market growth opportunities identified particularly within defense sectors.

Continued execution on efficient manufacturing ramp-up will be critical for enhancing returns sustainably beyond near-term reinvestment cycles.

Industry Context & Competitive Positioning (Analysis)

The global PCB market is intensely fragmented yet technology-driven where advanced flex-rigid multi-layer offerings command premium pricing mainly servicing aerospace/defense niches requiring certifications like AS9100/Nadcap standards held by ELTEK.

While many competitors operate globally with scale advantages particularly across low-cost production bases such as China shifting more recently towards Southeast Asia (Thailand/India/South Korea), the specialized nature of ELTEK’s products combined with regulatory barriers such as ITAR limits direct substitution creating defensible niche protection points despite price competition risks.

Manufacturers are trending towards consolidation through providing turnkey one-stop solutions encompassing prototype through volume production stages—a space where ELTEK’s strategy aligns well through complementary partnerships securing flexibility across volume ranges while retaining control over sensitive technologies locally.

Supply continuity challenges remain a shared industry headwind stemming from constrained raw materials market pricing pressures impacting margins universally.

Conclusion

ELTEK LTD stands out as a niche supplier specializing in complex flex-rigid PCB manufacturing targeted predominantly at demanding sectors such as defense and aerospace where certified quality is a mandatory entry criterion. Recent investments have propelled top-line growth through capacity expansion yet introduced margin compression driven by inefficiencies during ramp-up phases combined with external currency impacts. Liquidity is robust without outstanding debt although free cash flow remains negative due to continuation of capital expenditures aimed at future scalability. Forward-looking success hinges critically on how effectively ELTEK can translate new capacity into operational efficiency gains while navigating competitive pressures from lower-cost producers alongside managing environmental regulatory uncertainties intrinsic to its factory location. Stakeholders should closely track quarterly operational performance improvements, backlog dynamics notably international contract developments, regulatory progress regarding environmental compliance matters slated for upcoming hearings, and currency fluctuation impacts on reported results. Ultimately, ELTEK’s combination of specialized capability sets coupled with accreditations grants it valuable positioning despite the structural challenges pervasive across the global PCB manufacturing landscape.

This analysis is based solely on publicly available information from SEC filings ([F1],[S#]) and recent news reports ([N#]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments