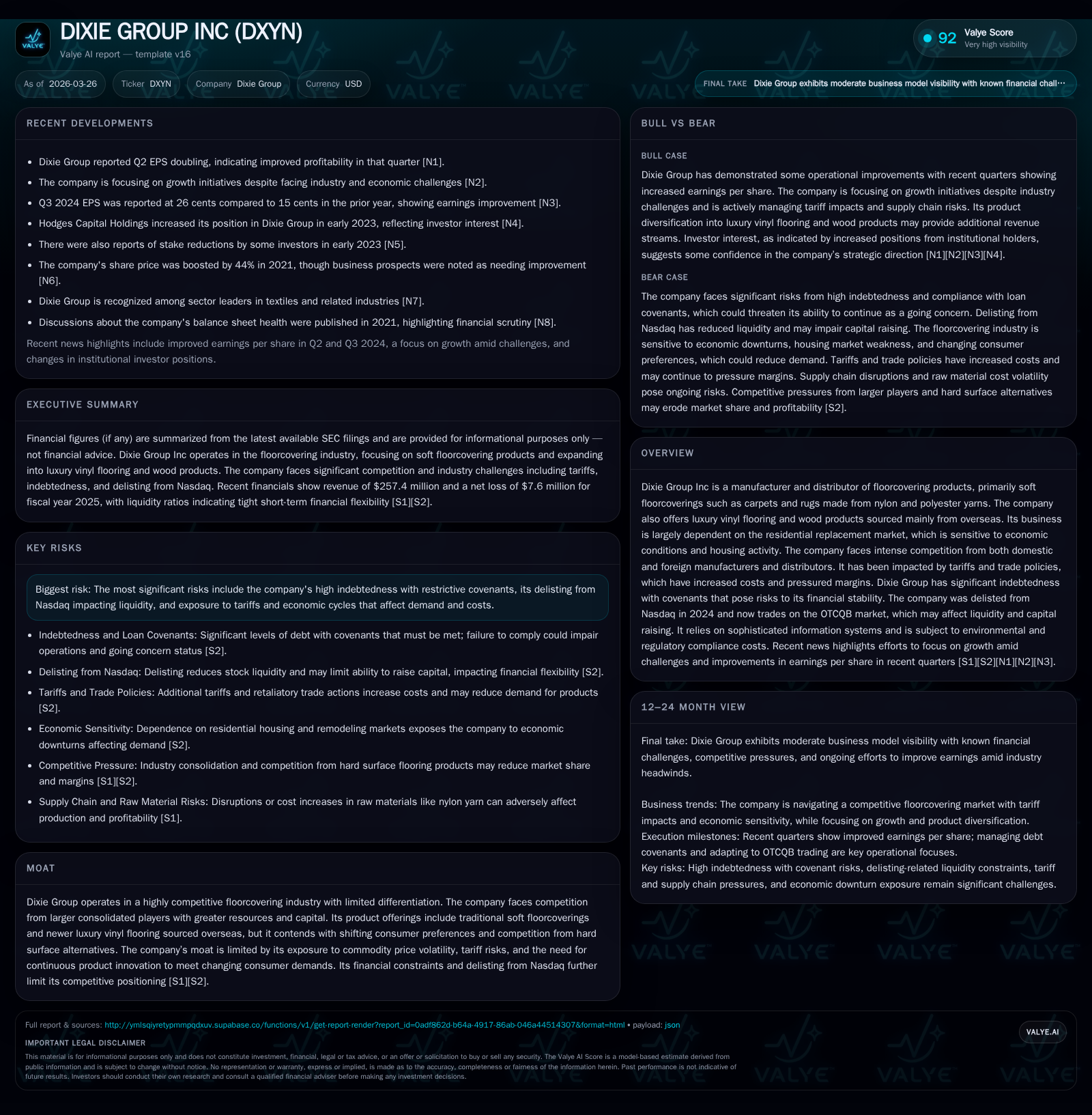

Dixie Group Inc Faces Margin Pressure and Debt Risks Amid Softening Consumer Flooring Demand

The company’s financials reflect industry headwinds from tariffs, high interest rates, and liquidity constraints despite cost-cutting efforts.

Dixie Group Inc operates in the competitive floorcovering sector, focusing on high-end carpets and rugs with additional luxury vinyl flooring offerings. Recent years have seen declining revenues pressured by macroeconomic challenges including inflation and tariffs, alongside significant indebtedness that introduces covenant compliance risks. While operating income improved slightly to near breakeven in 2025, net losses persist, driven largely by interest expenses. Liquidity remains tight with a current ratio below 1 and restricted access to capital markets following its Nasdaq delisting. Future growth hinges on a housing market recovery and effective tariff mitigation strategies, but these are clouded by ongoing economic uncertainties.

Company Overview

Dixie Group Inc primarily manufactures and markets soft floorcoverings including nylon and polyester carpets and rugs, complemented by luxury vinyl flooring (LVF) and wood products mainly sourced internationally [S1][S2]. The company targets the upper-end residential replacement market with brands such as Fabrica, Masland, DH Floors, and TRUCOR. International sales operate under Dixie International.

Historical Performance

From FY 2022 through FY 2025, Dixie Group's revenue declined steadily from $303.6 million to $257.4 million, reflecting weakening demand caused by inflationary pressures and high interest rates impacting housing market activity and remodeling spending [F1][S15][S16].

Operating income improved to a modest positive $118 thousand in FY 2025 after significant losses in prior years, supported by cost containment efforts including facility consolidation and productivity gains [F1][S24][S28]. Despite this operational progress, net income remained negative at -$7.62 million due primarily to elevated interest expenses tied to floating rate debt [F1][S28].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 257 | -8 | 0 | 1 | -2.9% | +41.4% |

| 2024 | 265 | -13 | -6 | 2 | -4.1% | -378.3% |

| 2023 | 276 | -3 | 5 | 1 | -9.0% | +92.3% |

| 2022 | 304 | -35 | -28 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 27000 | -86.6 |

| 2024 | 585000 | -80.2 |

| 2023 | 43000 | -9.3 |

| 2022 | 737000 | -111.3 |

Source: SEC companyfacts cache [F1].

Capital Structure & Liquidity

As of the end of FY 2025, Dixie Group reported current liabilities surpassing current assets resulting in a current ratio of approximately 0.97 with cash and equivalents totaling about $3.2 million against over $101 million in current liabilities [F1]. This tight liquidity position is exacerbated by roughly $53 million outstanding on its senior revolving credit facility classified as current due to subjective acceleration clauses permitting lenders to demand immediate repayment under adverse business conditions [S4][S5][S8][S10].

Management acknowledges the risk of covenant breaches despite having secured waivers previously; maintaining compliance remains uncertain without improved cash flows or refinancing options [S4][S10][S26]. The company's ability to continue as a going concern depends significantly on resolving these funding challenges.

Industry & Market Challenges

The floorcovering industry is highly sensitive to economic fluctuations linked to housing turnover rates and remodeling activity which remain subdued due to high mortgage rates and inflation dampening consumer discretionary spending [S15][S16]. Dixie Group’s core residential replacement segment faces delayed purchases impacting revenue.

Trade tensions have introduced tariffs on various imported materials essential for Dixie’s product lines including LVF components and carpeting inputs sourced globally [S17][S19]. Retaliatory tariffs by other countries further complicate supply chains.

Management is actively pursuing mitigation strategies such as reassessing sourcing origins, negotiating with suppliers, adjusting pricing strategies, and enhancing productivity although uncertainty around tariff persistence clouds outlooks [S19][S27].

Cost Efficiencies & Product Development

The East Coast Consolidation Plan aims to reduce manufacturing costs and improve operational efficiency; early results show some margin stabilization supported by lower input costs and reduced selling & administrative expenses [S24][S28]. Investment in extrusion equipment seeks greater vertical integration of yarn production enhancing supply chain control long-term [S21][S22].

Product innovation remains critical amidst shifting consumer preferences favoring hard surface flooring alternatives; LVF offerings provide diversification but remain vulnerable to tariff impacts [S27].

Future Outlook & Growth Considerations

Growth prospects hinge on an eventual decline in interest rates that could stimulate housing turnover and remodeling activity—key drivers for Dixie’s sales volumes given aging housing stock trends [S15][S29]. However, persistent inflationary pressures alongside macroeconomic uncertainties pose risks to demand recovery.

Financially, addressing debt covenant compliance through either improved operations or capital restructuring will be pivotal for sustaining operations beyond the near term [S26]. Prolonged tariff-related cost pressures could further compress margins.

Capital Allocation & Returns

With ongoing net losses constraining free cash flow distribution capacity, shareholder returns via dividends or buybacks remain minimal; share repurchases totaled approximately $27 thousand in FY 2025 reflecting a conservative capital preservation stance [F1].

Capital expenditures were tightly controlled at $598 thousand in FY 2025 compared with over $2 million the prior year as investment was curtailed amidst liquidity constraints; however operating cash flow remained positive enough to exceed capex by roughly $13 million indicating modest operational cash generation improvements [F1].

Return on equity remains deeply negative at approximately -86%, reflecting accumulated losses relative to shareholder equity levels though impacted by non-cash charges embedded within historical deficits [F1].

Material Risks & Contingencies

Dixie faces ongoing legal exposure related primarily to historical use of chemicals such as PFOA/PFOS surfactants involved in multiple lawsuits since the mid-2010s; while currently immaterial financially this requires continued management attention with potential contingent liabilities [S13][S20].

Cybersecurity risks pose threats of disruption affecting order processing or manufacturing controls potentially impacting customer confidence or operations continuity [S21][S22][S23].

Environmental regulations concerning material sourcing—particularly forced labor rules—may increase compliance costs adding pressure on international supply chains [S27].

Natural disasters impacting concentrated manufacturing facilities remain an external vulnerability capable of causing material operational disruptions or uninsured losses [S20].

Summary

Dixie Group operates within a challenging environment marked by cyclical economic headwinds suppressing demand for its core flooring products alongside structural issues including tariff-driven cost increases and significant leverage creating liquidity strains.

Operational improvements through cost containment have yielded modest margin stabilization yet revenue declines continue amid macroeconomic pressures affecting residential remodeling activities.

The company’s viability depends critically on managing debt covenant risks coupled with navigating evolving trade policies impacting input costs while monitoring signs of housing market normalization that could revive remodeling-driven sales.

Investors should closely track quarterly performance updates for shifts in sales trends within high-end segments along with any changes in trade policy or debt covenant status that may signal directional shifts.

This analysis reflects information available through March 26, 2026 based on SEC filings; it does not constitute investment advice or an offer to transact securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments