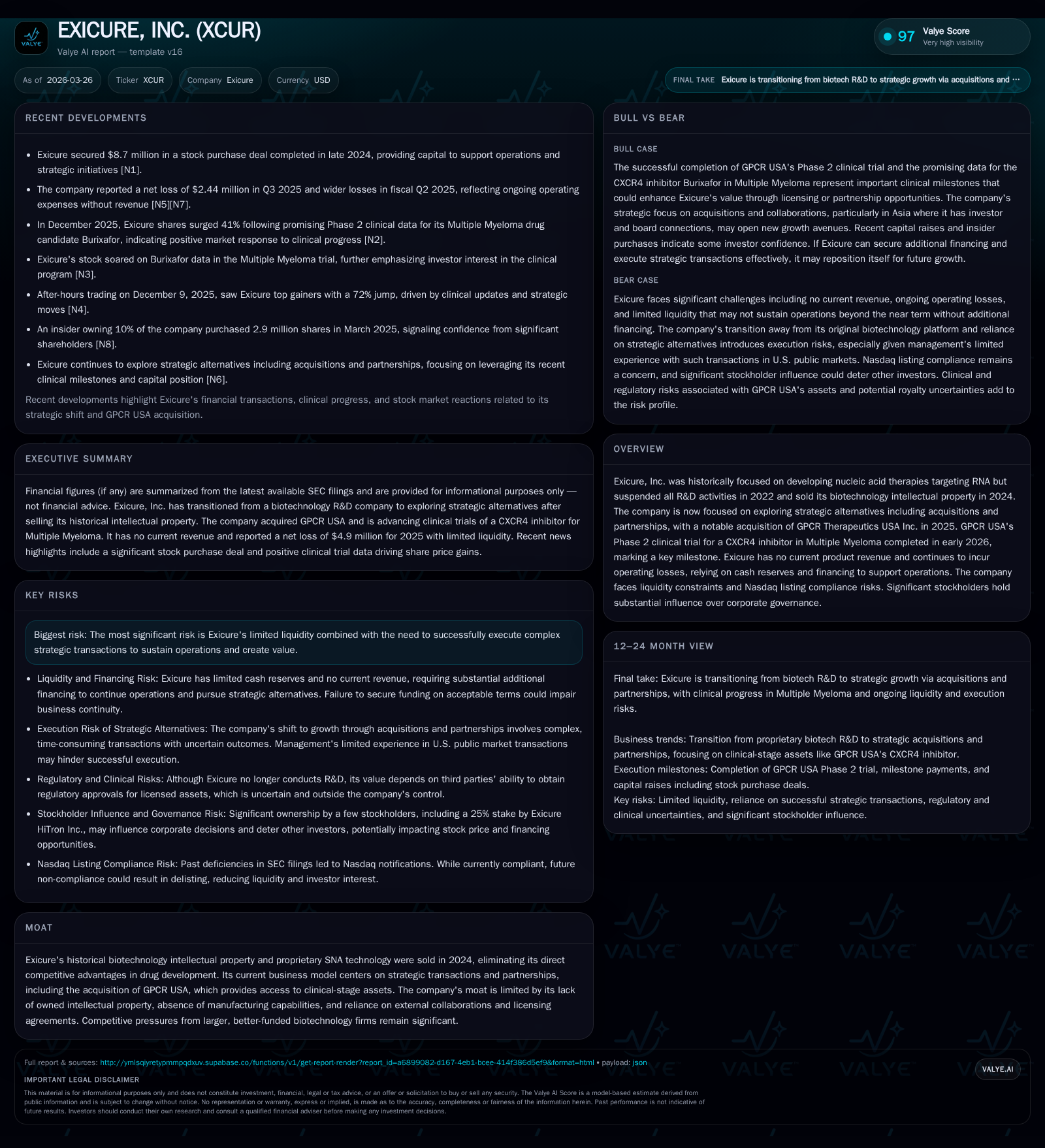

Exicure’s Reinvention: Transitioning from RNA Therapeutics to Strategic Acquisitions

After halting its pioneering RNA therapeutic research, Exicure has reshaped itself around acquisitions and strategic partnerships, facing significant liquidity pressures along the way.

Exicure, once focused on nucleic acid therapies targeting RNA via proprietary SNA technology, suspended R&D operations in 2022 and divested its biotechnology intellectual property in 2024, marking a decisive pivot away from internal drug development. The acquisition of GPCR Therapeutics USA Inc. in 2025 introduced clinical-stage assets, including a Phase 2 trial completion in early 2026 for a CXCR4 inhibitor targeting Multiple Myeloma. Despite this clinical milestone, the company generates no revenue, continues to record operating losses, and relies heavily on dwindling cash reserves and recent equity raises to fund operations. Nasdaq listing compliance risks and concentrated stockholder influence amplify governance and market uncertainties. With no explicit guidance issued, Exicure’s future rests on successful execution of strategic alternatives amid tight liquidity constraints.

From Biotech Pioneer to Strategic Transaction Vehicle: Historical Growth and Shift

Exicure entered the public markets as a biotech innovator developing nucleic acid therapies leveraging its proprietary spherical nucleic acid (SNA) technology platform aimed at RNA targets. This internally-driven R&D model positioned it among emerging nucleic acid therapeutic developers since inception in 2011. However, the trajectory changed markedly over recent years. The company’s annual revenue plummeted from $28.8 million in FY2022 to just $0.5 million in FY2024 before dropping to zero in FY2025 as it ceased active drug development [F1].

This collapse reflects the suspension of all research activities announced in September 2022 and a strategic move away from preclinical development toward monetization initiatives via licensing until fully divesting its biotechnology IP assets by mid-2024 [S1],[S20]. The associated operating losses narrowed from peak deficits near $18.9 million in FY2023 to about $4.23 million in FY2025 but remain deeply negative consistent with wind-down costs and general corporate overhead absent product revenues [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -5 | -9 | -4 | -100.0% | +49.0% |

| 2024 | 1 | -10 | -3 | -12 | +42.6% | |

| 2023 | 0 | -17 | -10 | -15 | -100.0% | -555.1% |

| 2022 | 29 | -3 | -36 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -9 | -126.0 |

| 2024 | -143.3 | |

| 2023 | -10 | -558.0 |

| 2022 | -36 | -17.3 |

Source: SEC companyfacts cache [F1].

Table: EXICURE Historical Key Financial Metrics FY2022-FY2025 [F1]

The precipitous revenue decline underscores how the cessation of R&D and sale of core IP extinguished direct product income sources. At the same time operating losses shrank due mainly to reduced R&D spend but not enough to approach profitability or positive cash flow.

Liquidity Challenges Shape Operational Realities

With no product revenues scenario looming since mid-2022 and minimal royalty income prospects following IP sale arrangements providing only uncertain future royalties per contract terms [S1], Exicure’s cash position has become critical.

As of December 31, 2025,the company reported cash and equivalents near $3.7 million with total current assets at approximately $4.62 million against current liabilities of about $3.89 million yielding a current ratio around 1.19 — indicating a narrow cushion for near-term liquidity demands [F1].

Operational cash flow trends are deteriorating rapidly; FY2025 operating cash outflows were approximately $8.56 million — a near doubling decline compared to negative $2.91 million during FY2024 — despite company cost-cutting measures implemented earlier reflecting limited scope for further staff or overhead reductions without impacting strategic exploration efforts [F1],[S9],[N1].

To bridge these gaps recently completed equity financings involving stock purchase agreements contributed about $8.7 million during late December 2024 which underpin survival through early- to mid-2026 pending execution of planned growth transactions or additional funding events [N1],[S13].

Risks surrounding liquidity are compounded by precarious Nasdaq listing status due to historic late filings noted as recently as Q1-Q3 2025 requiring rapid remediation efforts [S9],[S21]. Failure to maintain listing would impair trading liquidity further constraining capital access.

Leveraging GPCR USA Acquisition: Clinical Milestone and Strategic Imperatives

A centerpiece of Exicure’s reinvention strategy is acquiring promising assets via strategic transactions rather than organic development.Hard evidence lies in the January 19th ,2025 acquisition of GPCR Therapeutics USA Inc., which brought forward an active Phase 2 clinical asset focused on oncology – specifically hematopoietic stem cell transplant-eligible multiple myeloma patients treated with GPC-100,a CXCR4 receptor antagonist combined with propranolol for mobilization therapy.[S1]

GPCR USA successfully completed this Phase 2 trial by January 2026 signifying an important de-risking event aligning with Exicure’s goal to pivot into oncology therapeutics pipeline management despite lack of direct R&D capabilities.Simultaneously,the company assumed obligations under a License & Collaboration Agreement requiring milestone payments tied to clinical progression,target approvals,and sales royalties.These contractual commitments inject ongoing capital demands amidst constrained funds.[S1]

This shift transitions Exicure into a deal-driven model reliant on managing external clinical-stage programs versus traditional internal discovery platforms.Without manufacturing capability or owned IP,their competitive “moat” now entirely depends on effectively navigating these partnerships within a crowded biotechnology landscape dominated by larger players.[N1],[S20]

Capital Allocation under Pressure: Cash Flow, Equity,and Funding Needs

Exicure’s capital deployment over recent fiscal years confirms survival-focused spending patterns aligned with transformative objectives rather than growth investments.Capex was negligible at around $1k in FY2025 following the discontinuation of internal laboratory research reflecting minimal physical infrastructure needs.[F1]

Operating losses persist while net income remains firmly negative across years (-$4.95M net loss vs only $3.93M equity at FY-end 2025),yielding an approximate return-on-equity (ROE) metric of -126%, underscoring severe value erosion.

There have been no dividends or share repurchase programs as firm resources are devoted exclusively toward maintaining operational viability through equity dilution instead.[S13]

Equity has declined significantly from over $14.9 million at end-2022 down to less than $4 million as accumulated deficits mount—a reflection both of sustained operational shortfalls as well as issuance-related dilution.[F1]

Reliance on large stockholders such as HiTron owning approximately one-quarter of outstanding shares post-latest tradings adds complexity to both governance dynamics and perceptions around independence or controlling interests.[S13]

Governance Dynamics and Risk Exposure: Stockholder Influence & Litigation Environment

Concentrated ownership presents dual-edged implications.Under controlling stakes held by prominent investors like HiTron,Cand possibly others,[S13] decisions concerning future transactions may face internal alignment challenges amid competing agendas.Market perception often discounts shares influenced heavily by aligned interests reducing appeal among broad investors.[S22]

Legal exposure compounds risk profile.Exicure resolved securities class action litigation settled for $5.625 million with costs insured except for self-insured retainer exposure estimated near $1.1 million resulting in accrued liabilities recorded through mid-2025.[S6],[S7]

Further contentious issues include a dispute over approximately $0.7 million in unpaid rent relating to Redwood City facilities subleased by GPCR USA culminating in unlawful detainer proceedings filed March 9th , 2026,[S6],[S26] plus unresolved employee claims involving breach of contract cases with potential damages litigated into mid-2026 timelines.[S5]

Material weaknesses identified within internal controls against the backdrop of recent restatements jeopardize confidence among investors and regulators alike potentially influencing stock price volatility negatively.[S18]

Together these governance risks intersect materially with fragile liquidity positioning magnifying concerns regarding sustainable corporate stewardship going forward.

What to Watch Ahead: Milestones,Funding,and Business Model Validation

Looking forward investors should carefully monitor several critical catalysts shaping Exicure's trajectory.First is any update on GPCR USA clinical assets beyond Phase 2 completion—success here could attract partners or justify further capital raises.Second is progress closing additional acquisitions or forming strategic transactions confirming their pivoted business approach's scalability.[N1],[S1]

Additional financing rounds will likely be necessary given limited runway demonstrated by negative operating cash flows approaching nearly nine million annually.[F1]Watch also Nasdaq compliance measures including timely financial reporting deadlines which if missed could risk delisting.[S9],[S21]

Uncertainties loom around timing and quantum of royalties linked to former biotech IP licensing potentially delivering episodic income streams—these remain speculative without formal arrangements settled fully.[S20]

Operationally mitigating legal disputes without substantial cash drain will be crucial along with strategies to broaden shareholder base diminishing concentrated control concerns.[S6],[S22]

In sum Exicure stands at an inflection point where executing complex strategic transactions under considerable financial pressure is pivotal.The current lack of owned intellectual property compels reliance on external clinical assets such as those from GPCR USA.The path forward demands deft capital management allied with successful partnership integration and regulatory navigation within an intensely competitive sector.

This analysis draws entirely on publicly available information provided through official SEC filings and verified news sources up to March 26th , 2026.You should consider inherent limitations when assessing emerging biotech companies undergoing significant business model transformations.No investment advice or price forecasts are included herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments