Marchex Inc Faces Revenue Decline Amid Persistent Operating Losses and Customer Concentration Risks

Marchex leverages AI-driven conversational intelligence to optimize customer acquisition but faces headwinds from competitive pressures and financial losses.

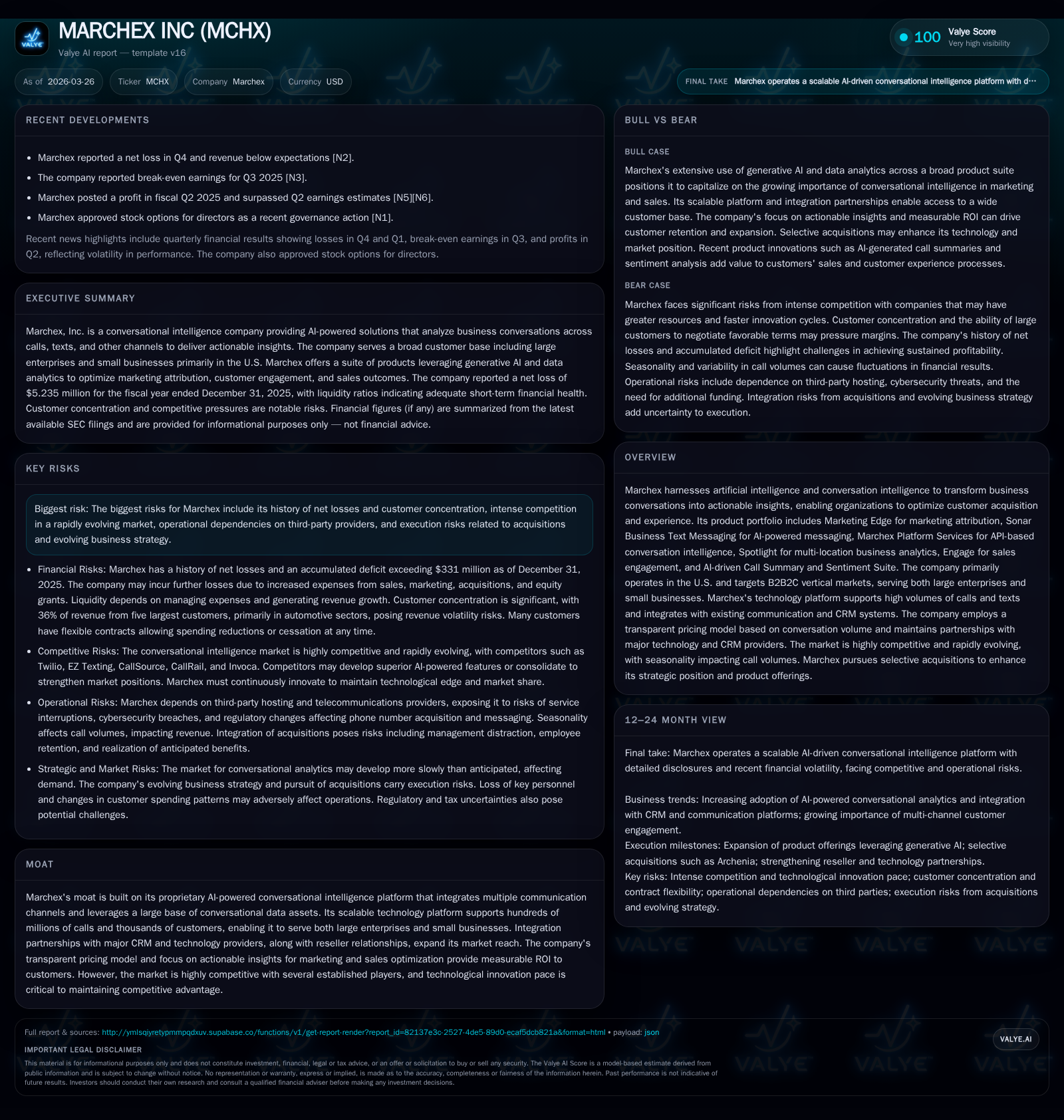

Marchex Inc, a conversational intelligence provider serving B2B2C verticals primarily in the U.S., has experienced a notable decline in revenue alongside persistent net losses. Its proprietary AI platform supports large-scale call and text analytics integrated with CRM systems, offering actionable insights to enterprises and small businesses. Despite ongoing product innovation and integration partnerships, its future growth is constrained by customer concentration, competitive intensity, and regulatory risks. The company’s financials reveal deteriorating operating income and negative cash flow, underscoring the need for operational efficiencies and strategic expansion.

Company Overview

Marchex Inc has positioned itself at the intersection of artificial intelligence (AI) and conversational intelligence to transform business communications into actionable insights. The company focuses primarily on U.S. markets and serves a broad B2B2C customer set ranging from large enterprises with distributed footprints to numerous small local businesses. Its technology platform processes vast volumes of calls and texts every day, integrating seamlessly with existing communication ecosystems and CRM software.

Central to Marchex’s value proposition is enabling clients to optimize customer acquisition funnels and improve sales outcomes through real-time insights into conversations leveraging generative AI. This includes products such as Marketing Edge for end-to-end marketing attribution analytics; Sonar Business Text Messaging which automates personalized two-way messaging workflows; API-driven Marchex Platform Services enabling integration across communication channels; Spotlight analytics tailored for multi-location businesses; Engage for improved sales engagement; plus AI-fueled Call Summary and Sentiment Suite that helps identify customer satisfaction trends.

Historical Performance

Over recent years, Marchex encountered significant headwinds reflected in both declining revenue and persistent operating losses. Reported revenues fell from $182.6 million in FY2014 down to approximately $90.3 million by FY2017—a collapse exceeding 50% during that period [F1]. More recently available figures detail further contraction relative to previous decades’ highs.

In terms of profitability, the company has largely operated in an unprofitable state since inception. Operating losses remained sizable at around $5.7 million for FY2025 despite efforts to innovate through AI integration [F1]. Net loss narrowed slightly to $5.2 million in FY2025 but still represents significant accumulated deficits north of $331 million as reported [S1/S7].

Operating cash flow demonstrated ongoing negative trends with -$1.4 million recorded in FY2025 after improvements from prior years’ wider deficits [F1]. Minimal capital expenditures recently—only roughly $36k in FY2025—indicate tight spending control possibly aimed at conserving cash.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -5 | -1 | -6 | 0 | -5.8% |

| 2024 | -5 | -1 | -4 | 0 | +50.1% |

| 2023 | -10 | -4 | -10 | 1 | -20.2% |

| 2022 | -8 | -2 | -8 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | -17.4 |

| 2024 | -2 | -15.2 |

| 2023 | -6 | -27.6 |

| 2022 | -5 | -18.7 |

Source: SEC companyfacts cache [F1].

¹YoY is extrapolated based on most recent data point vs prior quarter/year where applicable [F1]

Business Model & Product Portfolio

Marchex’s business model charges customers based mostly on conversation volume (calls or texts), creating a transparent scaling pricing mechanism aligned directly with client usage [S10]. This arrangement enables measurable ROI but also introduces volatility linked to client consumption patterns.

The company's technology platform underpins services supporting hundreds of millions of conversations while maintaining flexibility towards small businesses as well as enterprise accounts [S10]. Significant integration partnerships with Adobe, Google, Salesforce, among other CRM vendors empower seamless interoperability stimulating adoption [S5]. Moreover, reseller agreements expand distribution avenues beyond direct sales forces.

Key product offerings:

- Marketing Edge: Comprised of generative AI-backed analytics that trace inbound calls back to marketing campaigns closing the loop between marketing spend and sales outcomes.

- Sonar Business Text Messaging: An intelligent messaging workflow solution augmenting engagement via personalized two-way texting powered by AI automation.

- Marchex Platform Services: An API toolkit that allows incorporation of Marchex conversational intelligence regardless of clients’ underlying communication platforms.

- Spotlight: A robust analytics tool targeting multi-location enterprises helping track performance disparities across branches.

- Engage: Focuses on sales engagement improvement featuring call outcome analyses integrated within CRM platforms.

- Call Summary & Sentiment Suite: AI-enabled summarization of call content highlighting exceptionally positive or dissatisfied customers facilitating prompt action.

Competitive Environment & Risks

The conversational intelligence space is intensely competitive with established players including Twilio, Invoca for call analytics, EZ Texting for messaging platforms, as well as broader competitors like Google's own Ads call tracking capabilities [S19/S22]. Constant innovation is required merely to maintain parity given rapid technological evolution particularly in applying generative AI.

Customer concentration presents a material risk; about 36% of revenue stems from just five large customers heavily weighted toward automotive sectors [S4/S7]. These clients wield considerable negotiating leverage potentially mandating pricing concessions or demanding additional functionality under penalty clauses impacting margins.

Operational dependencies on third-party telecom providers introduce risk given regulatory uncertainties surrounding telephone number provisioning under FCC guidelines plus new mandates like 10DLC registration fees impacting cost structures [S26]. Furthermore, compliance complexities arise given evolving telemarketing laws including TCPA restrictions on automated calls/texts exposing Marchex to potential liabilities if customers fail adherence [S14/S18].

Intellectual property challenges also lurk as competitor patent consolidation may increase litigation frequency thereby diverting resources from core business activities [S8/S14]. Security breaches constitute another vector capable of causing customer attrition or material financial penalties [S21].

Future Growth Prospects & Strategic Focus

Management articulates a clear strategic imperative centered on expanding AI-driven conversational intelligence capabilities leveraging generative large language models throughout their portfolio [S22/S25]. Innovation includes broadening analytic coverage beyond voice calls into multifaceted communication streams encompassing texts plus enriched sales engagement functionalities.

There are ambitions to scale geographical footprint beyond U.S domestic markets long term but initial focus remains national due to regulatory complexity variations internationally [S10]. Growth drivers will likely hinge upon successful client acquisition complemented by upselling deeper analytic modules enhancing marketing efficiency validation plus sales uplift evidences delivered via product suites like Marketing Edge and Engage.

However, material growth impediments exist including heightened competition compressing pricing power; customer contract flexibility allowing abrupt spend reductions; regulatory cost escalations affecting gross margins; dependence on volatile call/text volumes tied directly to macroeconomic cycles; plus difficult capital access reflecting historical accumulated deficits exceeding $330 million restricting expansive investments without external funding injections [S1/S7].

Absent explicit forward guidance disclosed publicly recently, key monitoring points include trajectory of quarterly revenues especially new client wins or attrition rates; advancement pace integrating generative AI features; stabilization or reduction in operating losses; management’s ability to diversify customer base reducing concentration risks; along with regulatory developments around telecommunications compliance frameworks [N1][S3][S14][S20].

Capital Allocation & Financial Returns

Marchex has refrained from dividend distributions or share repurchase programs since at least FY2018 consistent with ongoing reinvestment into growth initiatives amidst financial constraints [F1]. Equity capital employed contracted moderately from approx $44 million in FY2022 down near $30 million by FY2025 correlating with substantive net losses sustained over multiple years.

Return on equity is negative around -17%, underscoring the lack of profitability despite efforts expended [F1]. Free cash flow remains negative roughly $1.4 million suggesting limited excess liquidity after operational demands though the company reported about $9.9 million cash & equivalents balance at year-end giving some runway buffer [F1].

Capital expenditures have been drastically curtailed recently (down over 90% YoY from prior years), possibly reflecting heavy completion or deferral of technology platform enhancements focusing instead on leveraging existing investments [F1]. Expenses likely skew heavily toward R&D personnel costs related to AI development plus incremental sales/marketing outlays needed for scaling customer acquisition amidst competitive friction.

Conclusion

Marchex Inc stands at a pivotal juncture deploying proprietary conversational AI technology amid fierce competition within dynamic regulatory landscapes while grappling with legacy financial challenges including sizeable accumulated deficits and reliance on concentrated large customers that influence revenue stability.

While management’s emphasis on generative AI integration promises incremental differentiation across its suite spanning marketing attribution to sales engagement analytics sustainably addressing B2B2C verticals requiring rich multi-channel conversational insight capture capability–realizing meaningful profitable growth depends critically on navigating operational scale efficiencies amidst tightening cost structures plus diversifying clientele mitigating concentration vulnerabilities.

Investors should track incoming earnings releases focusing keenly on sequential revenue trends given recent miss reported for Q4 fiscal year ended December 31, 2025 and ongoing expenses management efficacy alongside progress expanding product penetration within existing accounts or new partnership-driven customer wins [N1][N2]. Regulatory developments especially concerning telecommunications practices and data privacy remain important contextual variables potentially altering Marchex’s cost base or market opportunities going forward.

This analysis excludes any investment recommendations or price forecasts and is solely intended as an informational overview grounded in publicly available disclosures as of March 26, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments