Cato Corp’s Narrowing Losses Despite Revenue Pressure and Supply Chain Challenges

Cato Corp reported modest revenue growth but continued net losses in fiscal 2025, reflecting persistent operational headwinds amid improving margins.

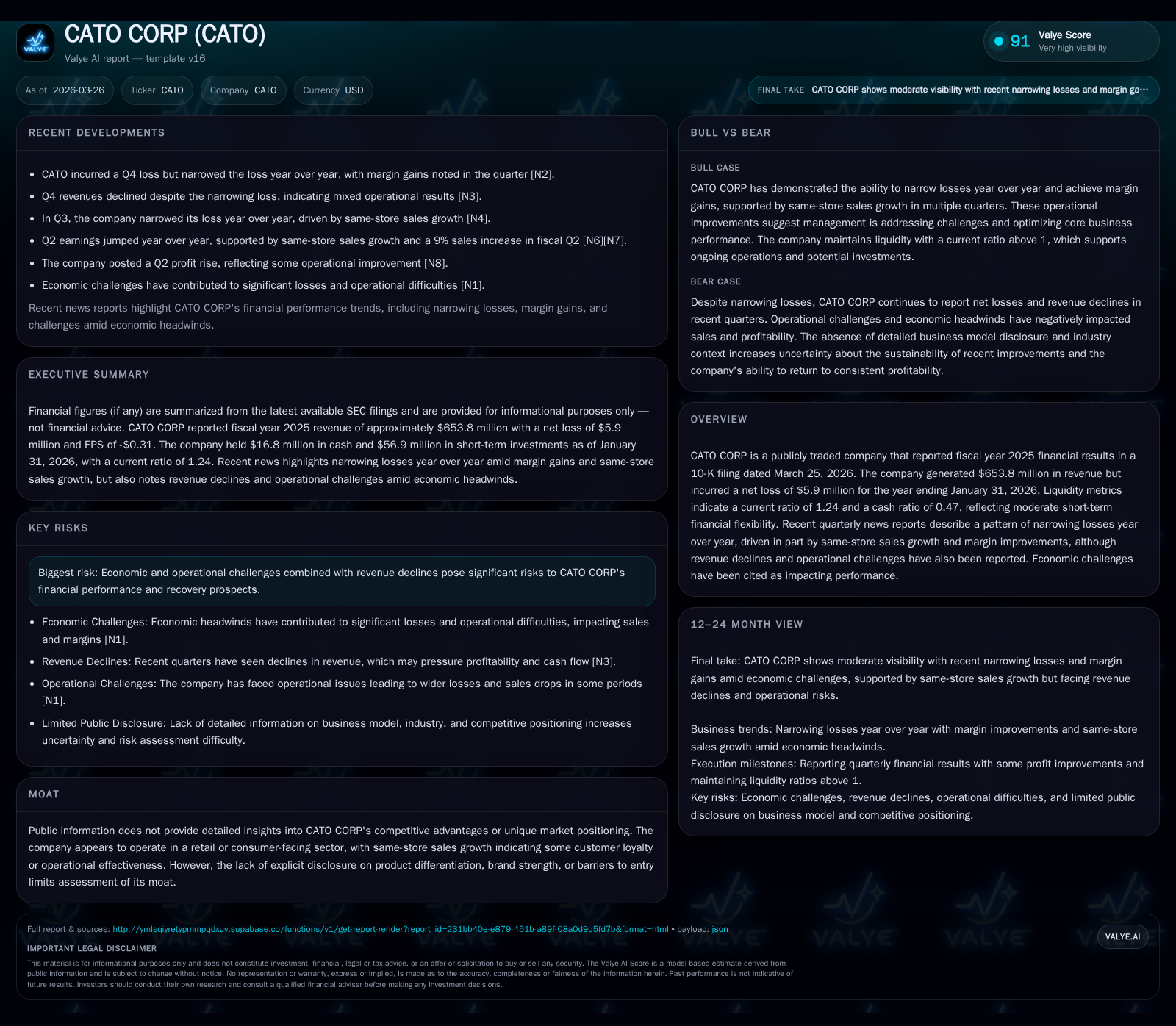

The Cato Corporation concluded fiscal year 2025 with $653.8 million in revenue, slightly up from the prior year, yet it sustained a net loss of $5.9 million. This result contrasts with wider losses experienced in recent years but reflects ongoing financial challenges including supply chain disruptions and elevated sourcing costs. While same-store sales improvements and margin gains provide some operational leverage, cash flow remains negative and capital expenditures have been curtailed. Monitoring shifts in consumer demand and supply dynamics will be vital for future performance.

Company Overview

Founded in 1946, The Cato Corporation is a retail fashion specialty company operating primarily in the southeastern United States with over 1,000 stores under various banners including Cato, Cato Fashions, It’s Fashion, and Versona [S1]. Its business model centers on offering coordinated apparel assortments at value-driven price points targeting junior/missy and plus sizes alongside general family fashion [S1]. The majority of merchandise is private label sourced globally, especially from Southeast Asia and Egypt [S1]. This model exposes Cato to international sourcing risks intensified by geopolitical tensions and global supply chain disruptions.

Historical Performance

Cato’s revenue trajectory has been volatile over the past four fiscal years. After peaking near $759 million in FY2022, revenues declined sharply to $649.8 million in FY2024 before modestly rebounding to $653.8 million in FY2025 [F1]. The revenue YoY moderation masks underlying pressures such as reduced store traffic and inventory challenges amid economic headwinds.

Operating income has languished in negative territory since FY2023 except for a small profit in FY2022, though the operating loss narrowed notably in FY2025 to -$12.7 million from -$26.4 million the prior year [F1]. Net losses mirrored this improvement from -$18 million to just under -$6 million over the same period [F1].

Further financial strain appears evident in operating cash flows that turned negative again at roughly -$1.46 million after positive CFO in FY2023 and strong positive cash generation in FY2022 [F1]. Capital expenditures were aggressively slashed by more than half from $7.87 million in FY2024 to about $3.76 million in FY2025 indicating a conservative approach to reinvestment during uncertain conditions [F1]. Notably, dividends were halted after more than a decade of steady payouts — zero dividends were declared or paid during FY2025 compared with over $10 million the year prior [F1]. Buyback activity also slowed markedly.

Historical Financial Summary

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 654 | -6 | -1 | -13 | +0.6% | +67.3% |

| 2024 | 650 | -18 | -20 | -26 | -8.2% | +24.6% |

| 2023 | 708 | -24 | 0 | -14 | -6.7% | -82655.2% |

| 2022 | 759 | 0 | 13 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 0 | 1 | -5 |

| 2024 | 11 | 4 | -28 |

| 2023 | 14 | 3 | -12 |

| 2022 | 14 | 15 | -6 |

Source: SEC companyfacts cache [F1].

Revenue declines started before pandemic recovery phases but improved operational efficiencies helped trim losses.

Business Strategy and Operations

Cato’s strategy focuses on differentiating its store experience via friendly service, appealing merchandise presentation, and affordable pricing aimed at value-conscious consumers [S1]. Coordination of colors and styles simplifies outfit selection — a retail tactic aimed at boosting basket size and customer satisfaction.

Their inventory heavily relies on vendor-produced private label goods meeting Cato’s specific design requirements [S1]. This reliance on third-party manufacturers abroad creates exposure to disruptions caused by tariffs, political instability, or shipping delays especially in key sourcing regions such as Southeast Asia and Egypt where recent geopolitical conflicts have increased costs [S1]. The company emphasizes cost control while striving to maintain fresh trendy assortments aligning with seasonality.

Recent Developments & News Highlights

Recent Q4 reports show narrowing losses driven partly by improved margins despite some revenue softness reflected across reporting periods ending January 31, 2026 [N1][N3]. Management highlighted ongoing economic challenges impacting consumer spending but cited operational steps producing same-store sales growth within core store fleets [N2]. Supply chain headwinds including extended freight routes due to Middle East hostilities have escalated ocean transportation costs leading to temporary delays [S1]. Domestic logistics constraints such as port congestion and driver shortages have further complicated timely goods receipt.

Risk Factors

- Supply Chain Vulnerabilities: Heavy dependence on overseas manufacturing exposes the company to tariff fluctuations, regulatory changes, geopolitical conflict risks, and elevated cost structures tied to shipping disruptions primarily through critical maritime trade corridors like the Suez Canal path rerouted around Cape of Good Hope amidst recent conflicts [S1].

- Economic Sensitivity: Consumer discretionary spending has been pressured by macroeconomic uncertainty which could dampen retail sales volumes further.

- Operational Strains: Negative cash flows reflect difficulties balancing working capital needs amid declining or stagnant top-line growth.

- Competitive Pressures: The absence of clear moat disclosures limits visibility into competitive advantages suggesting potential vulnerability against larger department stores or fast-fashion chains.

Future Growth Prospects & What To Watch

Looking ahead into fiscal years post-2025, improvement lines hinge on sustaining positive same-store sales trends while effectively managing escalating sourcing expenses and avoiding stockouts or markdowns due to supply volatility [N1][N2]. Progress toward streamlined operations that enhance gross margins would be critical for moving back toward profitability.

Given the current adverse cash flow position combined with limited reinvestment capacity seen via subdued capex levels indicates management's cautious stance on expansion or modernization initiatives for now [F1][S1]. Monitoring inventory turnover rates alongside gross margin trends will offer insight into response effectiveness against supply chain stressors.

Watch for any capital allocation shifts such as resumption of dividends or buybacks which could signal confidence returning or conversely further cuts signaling resource preservation mode given persistent market uncertainties.

Capital Allocation & Returns Analysis

Return on equity remains negative estimated around -3.8% based on latest net income relative to equity levels underscoring ongoing profitability challenges [F1]. Liquidity ratios stand at moderate levels with current ratio near 1.24 indicating working capital balance but cash ratio lower at approximately .47 reflects limited quick liquidity cushion [F1].

Over recent years, Cato pared down dividends fully ceasing distribution last fiscal year and trimmed share repurchase volumes significantly — suggestive of prioritizing liquidity amid tightening external conditions [F1][S7–S12]. Capital expenditures halved reflecting both cautious investment appetite and potential efforts towards cost containment rather than aggressive growth capex commitments.

Conclusion

The Cato Corporation evidences a retailer navigating marginal revenue stability paired with persistent losses weighed down by external supply chain shocks and macroeconomic impediments even as operational efficiency initiatives help shrink deficits year-over-year.

Its long history coupled with targeted value merchandising continues generating customer engagement within its regional footprint though large-scale structural challenges persist regarding supplier dependencies and cost pressures amid competitive retail dynamics.

Going forward, sustained improvement will require deft balancing between inventory management excellence, margin discipline, prudent capital deployment, and nimble response to evolving geopolitical trade risks – factors crucial for any apparel retailer reliant on global sourcing under today's complex environment.

This analysis was prepared solely for informational purposes based on publicly available data as of March 26, 2026 without any form of investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments