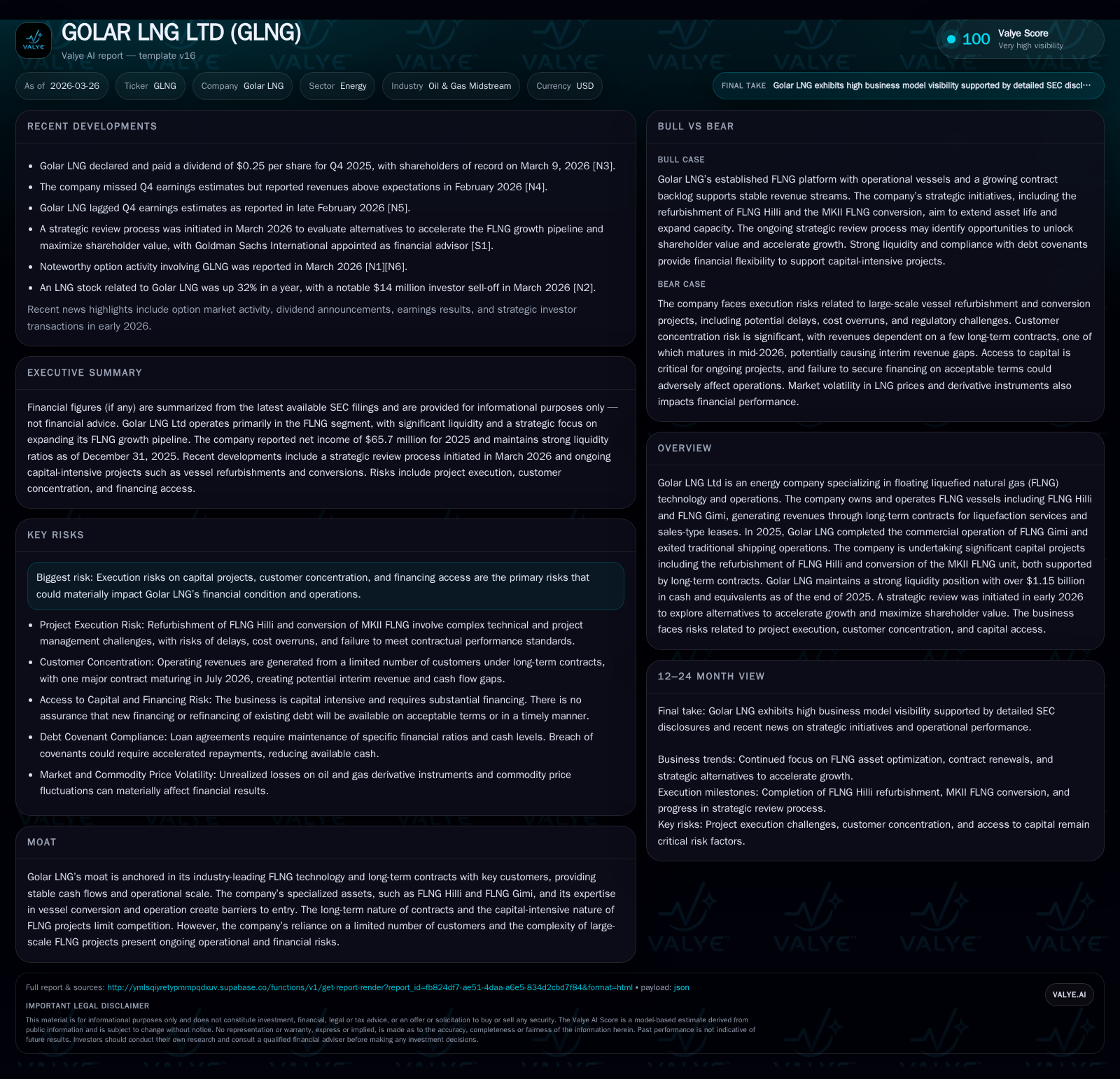

Golar LNG's Transition to FLNG Operations Sharpens Focus Amid Capital-Intensive Projects

Golar LNG shifts from traditional shipping to FLNG specialization, supported by long-term contracts and a strong liquidity base.

Golar LNG Ltd has reoriented its business model towards floating liquefied natural gas (FLNG) operations, completing the commissioning of FLNG Gimi in 2025 and exiting legacy shipping activities. The company’s historical revenue growth stems from expanding its FLNG fleet and securing long-term contracts with key customers. Future growth relies on successfully executing refurbishment and conversion projects—namely FLNG Hilli’s redeployment and the MKII FLNG conversion—while managing execution risks and customer concentration. Despite capital-intensive investments weighing on cash flow, Golar LNG maintains robust liquidity and has initiated a strategic review to explore avenues for accelerating its FLNG pipeline and enhancing shareholder value.

Historical Growth and Performance

Golar LNG has undergone a significant transformation over the past several years, pivoting away from legacy LNG shipping operations toward a focused platform centered on floating liquefied natural gas (FLNG) technology. The transition culminated in 2025 with the completion of commercial operations for the FLNG Gimi vessel and an official exit from traditional shipping businesses [S1]. This shift drove notable financial performance improvements: operating income nearly doubled year-over-year to approximately $100 million in 2025 from $62 million in 2024 (+60.4%) [F1], while net income grew by about 29% to $65.7 million [F1]. The scaling effects stem primarily from increased liquefaction service revenues linked to their specialized vessels.

Despite these earnings gains, cash flows have been volatile due to intensive capital projects underway. Net cash provided by operating activities increased substantially to roughly $471 million — up $152 million versus prior year — driven largely by improved pre-commercial operation receipts from FLNG Gimi [S6]. Conversely, investing outflows surged by approximately $400 million owing principally to project-related capital expenditures for vessel refurbishments and conversions, particularly for the MKII FLNG program [S6]. These factors combined have led to negative free cash flow given the heavy upfront investment nature of these complex offshore projects.

Historical performance (annual)

| FY | Net ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 66 | 100 | +29.2% |

| 2024 | 51 | 62 | +208.6% |

| 2023 | -47 | 16 | -105.9% |

| 2022 | 788 | 524 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 3.6 |

| 2024 | 2.5 |

| 2023 | -2.3 |

| 2022 | 31.5 |

Source: SEC companyfacts cache [F1].

*Top-line revenue details not explicitly reported for recent years but historically driven by liquefaction services under LTAs.

Drivers of Past Growth

The core drivers have included ramp-up of commercial activity at the newly commissioned FLNG Gimi which boasts approximately 2.7 million tonnes per annum nameplate capacity, along with steady production exceeding contracted volumes from FLNG Hilli under its long-term agreement (LTA). Both vessels benefit from contractual structures that provide stable, predictable remuneration either through tolling or sales-type lease arrangements [S12]. Incremental capacity utilization amendments have augmented base tolling fees as well.

Additional revenue comes through ship management fees on floating storage regasification units (FSRUs) operated for third parties though this segment has contracted following exit from direct shipping charters [S21,S22]. The company has also benefited from gains related to calibrated derivative instruments associated with their LTAs until maturity of those hedging programs by late 2024 [S22].

Future Growth Prospects

Looking forward, Golar LNG's growth trajectory hinges critically on several capital projects now underway:

FLNG Hilli Redeployment: Following LTA expiration mid-2026, Golar is executing a $350 million refurbishment aimed at extending operational life and initiating a new 20-year contract with Southern Energy S.A. (SESA) in Argentina, which promises stable long-term revenues contingent on technical delivery milestones being met [S4,S16,S24].

MKII FLNG Conversion: The company’s first application of its modified MKII design involves converting a donor vessel into an FLNG unit under another multi-decade contract with SESA valued above $1 billion in committed capital expenditures [S4,S16,S24]. This project represents both an opportunity to leverage proprietary technology at scale and a risk vector given the complexities inherent in such conversions.

Both ventures face typical execution risks including potential contractor delays, supply chain issues amid inflationary cost pressures, regulatory permit uncertainties, and strict performance covenants that could delay revenue recognition or increase cash requirements if disrupted [S4,S16].

Customer concentration is substantial; revenues emanate largely from a limited number of counterparties who hold long-term contracts but whose maturities cluster near term — such as the upcoming Hilli LTA expiry July 2026 — creating transitional gaps in cash flow until new deployment phases start generating earnings [S4]. This cyclical dependency accentuates operational risk.

Outside these flagship projects, Golar continues exploring additional growth opportunities leveraging its leadership in FLNG technology including potential FEED engineering studies for next-generation MKI/MKIII platforms [S21]. However, no definitive timelines or sanction decisions have been publicly disclosed.

Financial Forecasts and Milestones to Watch

While explicit formal guidance is absent as per current SEC filings [S1], critical milestones that will validate growth prospects include:

- Successful completion and redeployment of FLNG Hilli on schedule in late 2026/early 2027 into its new LTA,

- Progress updates on MKII FLNG conversion project leading up to expected start of operations around late-2027/early-2028,

- Maintaining contract uptime and production volumes for existing assets through transition periods,

- Outcomes from the strategic review process currently underway announced March 2026 aimed at accelerating growth pathways or unlocking shareholder value via alternative corporate actions [S16].

Market participants should monitor quarterly operational updates specific to production levels, cost tracking on conversion projects (including any overruns), adherence to delivery schedules, and any adjustments announced relating to contract renegotiations or financing arrangements.

Returns and Capital Allocation

Golar LNG demonstrates an improving profitability profile with FY25 net income reaching nearly $66 million ([F1]), resulting in an approximate return on equity around 3.6% given equity capital near $1.84 billion at year-end [F1]. Operating margins benefited as the fleet transitioned fully into liquid natural gas processing roles rather than lower-margin shipping segments.

Capital allocation remains conservative reflecting high ongoing investment demands: capital expenditures related predominantly to major vessel conversions remain material without recent comparable capex reductions yet recorded openly due to timing differences ([F1]).

Dividend payments have been reinstated since early 2023 at quarterly rates around $0.25 per share subject to board discretion reflecting earnings and liquidity considerations ([N6], [S16], [S13], [S14]). Buybacks have occurred opportunistically but remain modest relative to overall capitalization given balance sheet priorities.

Liquidity is robust: at December 31, 2025 cash plus short-term deposits exceed $1.15 billion supporting project spend obligations for at least the near term without immediate refinancing pressures [F1], [S5]. Debt maturities extend well into the future though scheduled repayments require ongoing compliance monitoring of financial covenants under loans secured primarily against high-value vessel assets [S8],[S9],[S10],[S23].

Industry Context Analysis (Non-Firm Sources)

The midstream oil & gas sector increasingly views floating LNG solutions as critical enablers of flexible natural gas monetization especially where fixed infrastructure investment is prohibitive. Golar’s focus positions it well within this niche but execution complexity is elevated relative to standard shipping fleets or onshore liquefaction plants due to intensified technology integration challenges offshore.

Long-duration contracts remain vital moat elements shielding operators like Golar from commodity price volatility though customer concentration risk intensifies downside vulnerability when fewer counterparties dominate revenues without extensive diversification.

Conclusion

Golar LNG Ltd stands at a pivotal juncture having transitioned strategically away from legacy shipping toward a technologically specialized platform centered on floating LNG liquefaction assets backed by long-term agreements with major energy customers. The company’s recent financial performance improvements reflect this shift with rising profitability supported by expanded operational scale following commissioning milestones.

Nevertheless, investors should remain attentive to several factors shaping future outcomes: successful timely execution of significant capital projects driving next phase growth; managing concentrated counterparty exposure; sustaining strong liquidity amidst high upfront capex commitments; and navigating evolving financial covenant constraints.

Management’s decision in early 2026 to initiate a comprehensive strategic review underlines recognition that unlocking full value may require transformative corporate actions responsive to market dynamics over coming quarters. This process aims explicitly at accelerating growth trajectories leveraging their differentiated proprietary technology portfolio.

Overall, Golar's story exemplifies the balance between pioneering advanced midstream solutions requiring heavy capital investment, operational discipline needed to manage project risks effectively, and strategic agility demanded by rapidly evolving global LNG markets.

Disclaimer: This analysis summarizes historical data derived from SEC filings ([F1],[S#]) and publicly available news sources ([N#]) as of March 26, 2026. It is intended solely for informational purposes without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments