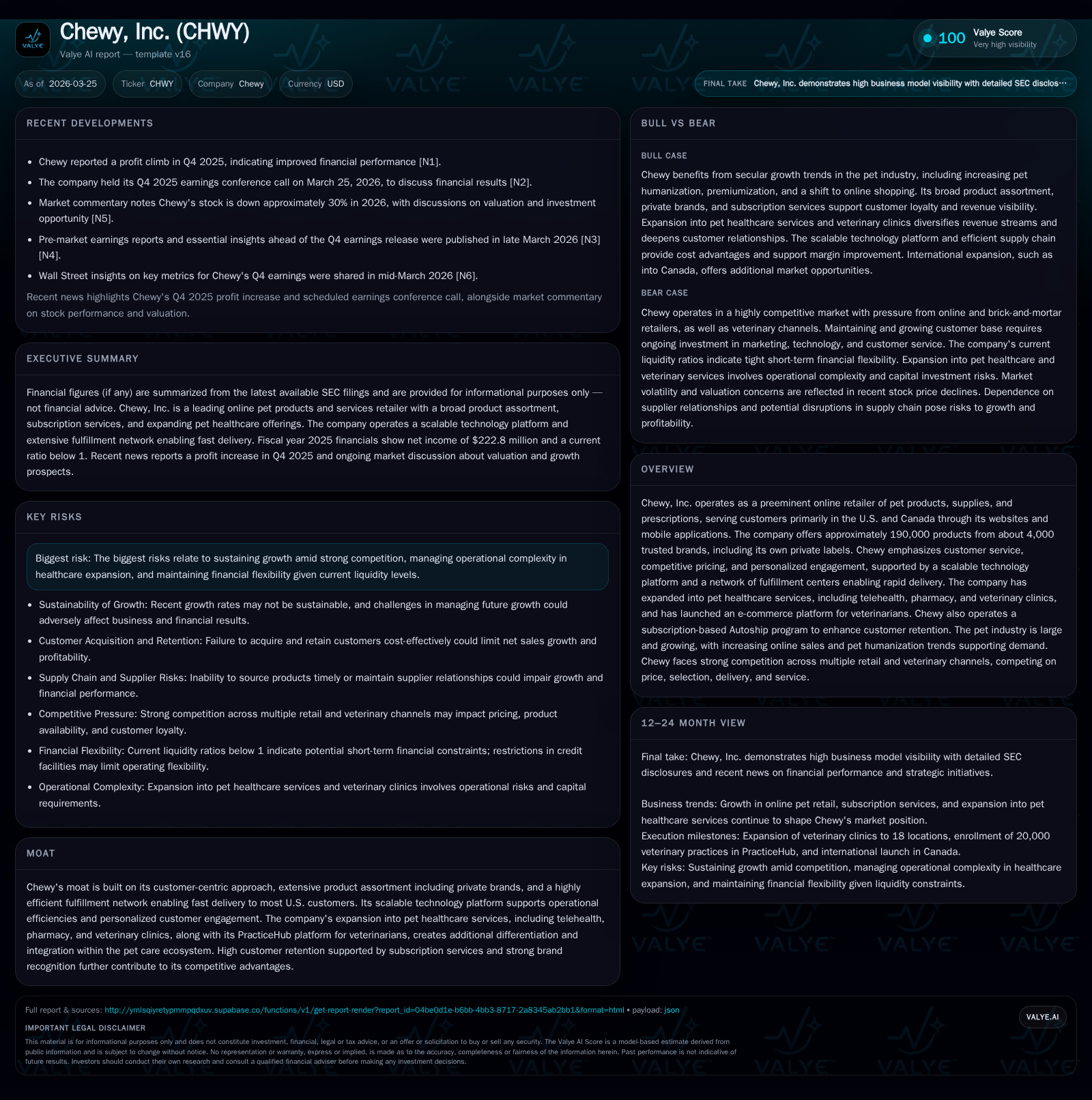

Chewy Inc.'s Strategic Evolution: From Rapid Growth to Healthcare Integration

Chewy has transformed from a fast-growing pet product e-tailer into an integrated pet healthcare platform, balancing growth ambitions with operational and competitive challenges.

Chewy, Inc. has demonstrated substantial operating income growth driven by its customer retention strategies and expanding product assortment, including private brands and subscription services like Autoship. Its strategic pivot towards pet healthcare—with telehealth, veterinary clinics, and proprietary technology platforms—aims to deepen customer engagement and ecosystem integration, albeit adding operational complexity. The scalable technology infrastructure facilitates margin improvement through automation and efficient fulfillment. However, competitive pressures from larger retailers and e-commerce specialists challenge Chewy’s unit economics. Capital allocation reflects disciplined investments in growth with robust free cash flow generation but modest liquidity headroom due to current liabilities exceeding current assets. Investors should closely monitor customer base expansion, margin evolution post-healthcare rollout, and fulfillment network scalability as indicators of sustainable growth.

Historic Growth Trajectory and Key Drivers

Chewy has exhibited a pronounced growth trajectory over the last four fiscal years with a marked inflection in profitability metrics by FY2025. Operating income climbed sharply to $254.3 million from $112.6 million the prior year—an increase of approximately 126% YoY [F1]. This rebound follows several years of relatively constrained or negative operating income figures such as FY2023 where operating income was negative $23.6 million.

Contrasting the increase in operating profit is a notable decline in net income which fell 43.3% to $222.8 million in FY2025 from $392.7 million in FY2024 [F1]. This divergence highlights ongoing investments impacting bottom-line results despite operational leverage.

Operating cash flow sustains an upward trend reaching $691.6 million in FY2025 (a 16% increase YoY), illustrating robust cash generation capabilities supporting reinvestment [F1]. Capital expenditures have been managed judiciously at $129 million for FY2025, down 10% YoY indicating efficient allocation aligned with scaling efforts.

A critical driver behind Chewy’s revenue stability is its Autoship subscription program which supports high retention rates among customers by automating recurring orders for pet supplies—a factor contributing to predictable revenue streams and enhanced customer lifetime value [S5][S13]. The company’s product assortment breadth—offering roughly 190,000 SKUs across approximately 4,000 brands inclusive of private label offerings—fosters up-selling opportunities that expand wallet share per customer over time.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 223 | 692 | 254 | 129 | -43.3% |

| 2024 | 393 | 596 | 113 | 144 | +892.3% |

| 2023 | 40 | 486 | -24 | 143 | -19.6% |

| 2022 | 49 | 350 | 56 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 263 | 562 | 44.7 |

| 2024 | 943 | 452 | 150.2 |

| 2023 | 343 | 7.8 | |

| 2022 | 23.0 |

Source: SEC companyfacts cache [F1].

Note: Capex figures prior to FY2022 partially omitted due to data limitations [F1].

Strategic Diversification into Pet Healthcare Services

Beginning with medication compounding capabilities launched in 2020 and telehealth services under “Connect with a Vet,” Chewy moved decisively beyond core retail offerings into pet healthcare [S10][S18]. The telehealth service expanded progressively; by end-2022 it was extended at no cost to all registered customers enhancing accessibility.

The introduction of "CarePlus" insurance and wellness plans starting in 2022 further diversified offerings across consumer price points [S10]. Expansion culminated in establishing physical veterinary clinics branded "Chewy Vet Care," which grew from eight clinics in FY2024 to eighteen by the end of FY2025 [S10]. These clinics provide routine care, urgent services, and surgeries powered by proprietary technology platforms that streamline both pet parent interaction and veterinary operations.

Complementing these initiatives was the launch of PracticeHub—an integrated e-commerce solution connecting veterinary practices directly to Chewy’s fulfillment network—bringing nearly half of U.S. vet clinics onto this platform by early 2026 [S4][S18]. This move embeds Chewy deeper into the pet care ecosystem fostering stickier relationships with professional partners beyond direct consumers.

This strategic shift aligns strongly with trends around 'pet humanization' where consumers prioritize comprehensive health solutions for pets analogous to family members [S1][S5]. Despite potential benefits including broader share of wallet and longer engagement cycles, healthcare service expansion introduces considerable operational complexity related to regulatory compliance across multiple jurisdictions as well as professional liability risks [S7][S16].

Technology Platform: Enabler of Scale and Margin Expansion

At Chewy’s core lies a scalable technology infrastructure designed expressly to support volume growth while reducing marginal costs per transaction [S4]. The fixed-cost intensity within their proprietary software platforms enables meaningful operating leverage as net sales grow.

Automation investments at fulfillment centers—including AI-driven forecasting, robotic picking/packing assistance, and optimized labor scheduling—have significantly boosted order accuracy and packing efficiency [S4][S18]. These improvements not only lower fulfillment costs but also uphold rapid delivery standards vital to customer satisfaction.

Additionally, customer service representatives are empowered through real-time access to detailed customer/pet profiles enabling personalized recommendations—a key differentiator supporting subscription retention via targeted Autoship engagement [S23].

The expansion of sponsored ads offerings provides vendors tailored marketing options on Chewy’s platform further monetizing traffic beyond core sales [S4]. Overall, these technology-led initiatives improve unit economics by lowering customer acquisition cost relative to lifetime revenue while reducing operational staff requirements per order processed.

Competitive Complexities in the Pet E-commerce Landscape

Competition remains intense featuring players spanning large traditional brick-and-mortar chains complemented by omnichannel digital strategies as well as specialty online-only retailers [S6]. Many competitors possess deeper financial resources enabling aggressive pricing tactics or elevated marketing spends potentially pressuring margins.

Chewy differentiates primarily through its depth of inventory—maintaining approximately four thousand brands including exclusive private labels—and acclaimed customer experience characterized by rapid shipping and expert support [S6][S13]. However, evolving competitive dynamics require constant innovation on marketing channels while controlling rising customer acquisition costs.

Prominent industry terms such as 'unit economics' are critical here: maintaining profitable contribution margins amid promotional pricing campaigns is a persistent execution challenge given the elasticity of pet product demand . Channel diversification including increased vendor participation via sponsored advertising contributes incremental revenue streams mitigating pure merchandise margin pressure.

Nonetheless, sustaining loyalty requires continual investment in personalization technologies and logistics enhancements given readily available alternatives from mass merchants’ online arms and emerging AI-powered retail platforms disrupting conventional consumer journeys.

Capital Allocation, Profitability, and Financial Health

Chewy exhibits commendable capital discipline balancing growth investments with shareholder returns amidst ongoing platform buildout. Free cash flow approximates $562 million for FY2025 calculated as operating cash flow minus capital expenditures ($691.6m - $129m), underscoring efficient cash conversion — an important metric given sizable operational scale [F1].

Return on equity stands near an impressive ~44.7%, reflecting effective leverage of invested capital driving profitability gains despite fluctuating net income margins attributable partly to reinvestment timing effects [F1].

Share repurchases totaled approximately $263 million during FY2025 demonstrating management’s intent to return capital albeit at levels considerably reduced from prior year ($943 million), consistent with moderated liquidity availability amid rising working capital demands [F1][S14]. Dividend payments remain absent aligned with reinvestment priorities stated in filings.

However, current ratio below unity at roughly 0.88 signals working capital tightness primarily due to current liabilities outpacing current assets necessitating diligent cash management especially as business segments expand operational complexity [F1][S14]. Ongoing capital commitments toward healthcare expansion warrant continuous monitoring against financial covenant restrictions embedded in credit facilities.

Outlook: What to Watch for in Chewy's Growth Path

Explicit forward guidance remains limited as per recent company communications around Q4/FY25 earnings release; thus analysis focuses on key performance indicators that will illuminate trajectory into mid-term:

- Expansion rate of active customers particularly penetration outside existing U.S./Canada footprint [N4][N10]

- Adoption trends within Autoship subscriptions influencing churn-adjusted sales visibility [N1]

- Margins post scaling of veterinary clinical services reflecting ability to manage healthcare integration costs effectively [N3]

- Fulfillment center automation impact on cost per order amidst volume fluctuations measuring operating leverage realized [N5]

- Uptake trajectory for PracticeHub among veterinary partners signaling ecosystem entrenchment potential

- Vendor monetization via sponsored ad product suite tracking relative contribution incrementality versus total sales effort expended.

Investors should be alert for signs of balance between growing top-line coverage versus margin dilution risks inherent with healthcare vertical expansion coupled with robust controls on fulfillment expense inflation.

Risks and Operational Challenges Ahead

Principal risks derive from intensifying competition exerting downward pricing pressure combined with rising operating complexity stemming from healthcare services diversity introducing regulatory compliance burdens alongside malpractice exposure potential [S7][S16].

Supply chain vulnerabilities including supplier disruptions or loss of key brand relationships expose Chewy’s assortment strategy affecting inventory availability or preferential pricing terms threatening customer satisfaction levels [S22].

Additionally present are cybersecurity threats inherent with extensive reliance on digital platforms exacerbated by evolving regulatory frameworks around data privacy requiring costly compliance adaptations or potential penalties if breached [S9][S17][S20].

Liquidity constraints reflected by sub-1 current ratio amplify risk around funding unforeseen contingencies or sustaining expansion cadence without excessive borrowing reliance risking covenant violations under revolving credit terms detailed [S14].

Mitigation stems principally from ongoing technology investments fostering operational resilience paired with disciplined capital deployment ensuring flexibility for strategic response.

This report synthesizes publicly available SEC filings alongside recent market disclosures without speculative forecasts or investment recommendations. It aims solely to provide institutional-quality insight into Chewy Inc.’s evolving business model dynamics within the expanding pet industry landscape.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments