Marex Group plc: Powering Client Solutions and Financial Returns in 2025

Marex delivered robust revenue and net income growth in 2025, fueled by strategic acquisitions and comprehensive liquidity services.

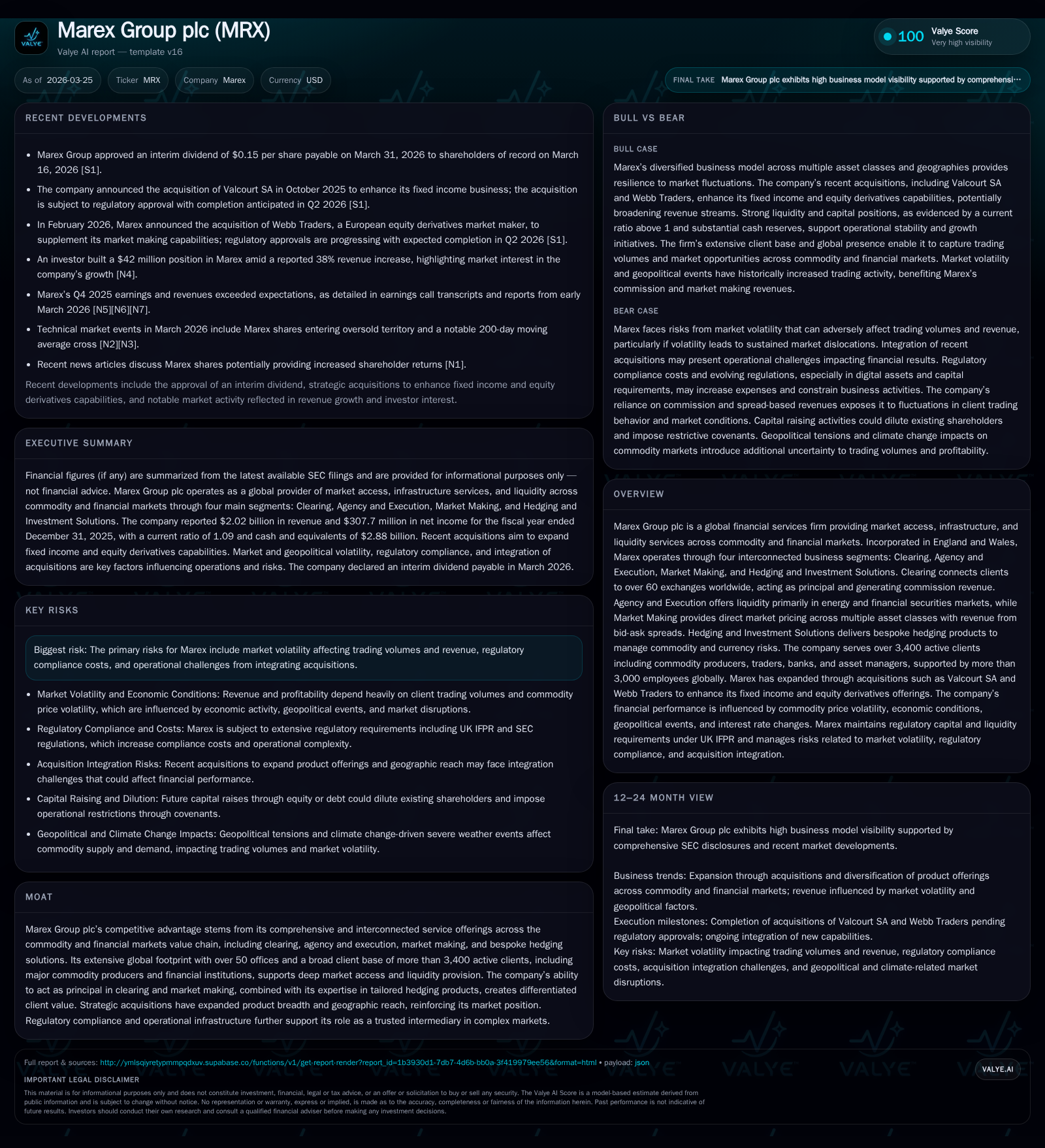

Marex Group plc posted a strong financial performance in 2025, with revenue rising 26.9% year-over-year to $2.024 billion and net income increasing 41.1% to $308 million [F1]. This growth was driven by the synergy of its four interconnected business segments—Clearing, Agency & Execution, Market Making, and Hedging & Investment Solutions—alongside strategic acquisitions such as Valcourt SA and Webb Traders [S1][S14][N2]. The company maintained a healthy liquidity position with over $1 billion headroom, supported by its senior notes and revolving credit facilities [S4][S6]. Marex continued disciplined capital allocation, paying dividends and executing share buybacks while managing leverage within regulatory covenants [F1][S11]. Going forward, monitoring client volume trends, integration success of acquisitions, and regulatory developments will be critical for sustaining growth and profitability [N1][S22][S23].

Revenue and Profit Leap: A Closer Look at 2025 Performance

Marex Group plc demonstrated a dynamic acceleration in financial results during fiscal year 2025. Total revenue soared by 26.9%, reaching $2.024 billion compared to the prior year’s $1.5947 billion [F1]. This impressive top-line expansion was complemented by a 41.1% increase in net income to $308 million from $218 million in 2024, underscoring improved profitability amidst expanding activities. Operating cash flow declined from $1.16 billion to about $667 million due primarily to increased stock borrowing/lending activities rather than diminished core operations [S10], indicating prudent working capital management adapting to greater trading volumes.

The jump in revenues was chiefly attributable to commission gains from Clearing—anchored by principal risk-taking—and improved bid-ask spreads realized within Market Making activities. Additionally, Agency & Execution volumes reflected heightened energy and financial securities transaction flows, while bespoke Hedging & Investment Solutions grew through enhanced client engagement across commodities and currencies [N2][F1]. This diversified revenue base showcases Marex’s ability to capture value across multiple interlinked facets of market access and liquidity services.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 2.0 | 308 | +26.9% | +41.1% |

| 2024 | 1.6 | 218 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 42 | 39.7 |

| 2024 | 64 | 22.3 |

Source: SEC companyfacts cache [F1].

*Operating cash flow decrease related to working capital changes rather than operational weakness.

Interconnected Services Driving Growth Across Commodity and Financial Markets

Marex’s integrated service delivery spans four primary operating segments: Clearing, Agency & Execution, Market Making, and Hedging & Investment Solutions [S1]. Clearing facilitates direct access to over sixty global exchanges, acting as the infrastructural bridge between clients and marketplaces—providing principal clearing on behalf of customers generates commission revenues foundational to scale.

Agency & Execution delivers deep liquidity pools within energy sectors (notably European gas/power markets) plus global financial securities including equities, credit instruments, foreign exchange, and rates products. This segment leverages extensive market intelligence tailored for each product domain—a marker of expertise that clients increasingly demand for efficient price discovery.

Market Making operates principally on spread income between buying and selling prices across metals, agricultural commodities, energy products, and financial securities without carrying substantial proprietary positions, reflecting disciplined principal risk management strategies common among liquidity providers seeking steady returns amid volatile markets.

Hedging & Investment Solutions complement these transactional services by creating bespoke derivative contracts enabling producers and consumers of commodities to manage exchange rate and price exposure dynamically over varied time horizons—embedding client-specific risk profiles into structured pricing models [S28][N2]. This customization solidifies long-term client relationships beyond mere execution.

Strategic Acquisitions Strengthening Market Presence and Product Breadth

Targeted acquisitions during late 2025 and early 2026 complement existing competencies while accelerating entry into adjacent domains. The October 22, 2025 agreement for Valcourt SA enhances Marex’s fixed income distribution capabilities aligning with diversification objectives amidst evolving client demand patterns [S14]. Completion is expected early Q2 2026 pending regulatory approvals.

Similarly, the February acquisition of Webb Traders bolsters Marex’s European equity derivatives market-making capacity while integrating equity-linked structured products internally—boosting profit margins through effective hedging assimilation [N2][S23]. These moves indicate deliberate orchestration of asset-class expansion coupled with geographic scale.

Integration complexity represents an operational risk requiring vigilant management given distinct regulatory regimes across jurisdictions as well as technology platform harmonization needs.

Liquidity Position, Capital Structure, and Debt Management

Marex maintains committed unsecured revolving credit facilities totaling approximately $380 million maturing mid-2026—including the Marex RCF ($150 million maturity June 2026) and MCMI RCF ($230 million maturity April 2026)—with typical non-financial covenants plus leverage limits such as total leverage ratio below three times debt-to-EBITDA equivalent levels [S4][S5].

Senior notes issued since late 2024 total roughly $1.38 billion bearing fixed interest rates near mid-5% range with maturities clustered in late-2028/2029 rated BBB- by major agencies [S4][S6]. These notes carry no traditional financial maintenance covenants enhancing financing optionality but embed customary call/redemption features.

Regulatory capital ratios remain comfortably above minimum thresholds at approximately 230%, supported by a risk-adjusted capital framework promoting resilience amid economic stresses common within regulated investment firms [S6][S24]. Cash balances exceed $2.88 billion as of December 31, 2025 evidencing prudent margin obligation preparedness for clearing activities [F1].

Capital Allocation Strategy: Dividends, Buybacks, Returns on Equity

Dividend payouts declined to $42 million from $63.8 million reflecting measured distribution amid increased acquisition spending and investment needs [F1][S11]. Concurrently share repurchases rose materially from about $20 million to $44 million supporting EPS accretion ambitions.

Adjusted return on equity approximated an attractive near-31.5% level using net income over average equity calculation despite incremental goodwill balances from acquisitions [F1][S13][S15].

Investing cash outflows surged mainly due to acquisition-related payments escalating investing uses nearly eightfold relative to prior year at approximately $264 million versus $35 million previously reflecting strategic growth initiatives supported via capital markets programs outlined above [S10].

Regulatory Environment and Risk Management Implications

Operating under multifaceted global regulatory frameworks—including FCA U.K., CFTC/SEC U.S., AMF France among others—requires sustained investment into compliance infrastructure amid heightened scrutiny of capital adequacy rules under IFPR regime plus extensive reporting demands impacting operational cost structures notably in finance and legal functions [S22][N2].

Market volatility acts as both growth driver via turnover spikes especially within Agency & Execution plus Market Making segments but also raises liquidity demands through margin calls complicating Clearing operations alongside increased counterparty risks warranting tight credit controls under IFRS expected credit loss models [S22][S24][N2].

Acquisition integration adds operational complexity; concurrent expansion heightens cybersecurity vigilance needs intrinsic to safeguarding sensitive trading infrastructure facing emerging digital asset regulatory uncertainties.

Investor Considerations Going Forward

Key metrics include sustaining client base expansion beyond current ~3,400 active accounts servicing commodity producers through institutional investors along with trading volume trends across energy derivatives crucial for Agency & Execution segment health [N3][N7].

Regulatory capital ratios merit ongoing monitoring alongside leverage metrics relative to credit facility conditions ensuring covenant compliance enabling funding access supporting acquisition appetite.

Completion of pending acquisitions like Valcourt SA early Q2 should deliver tangible earnings contributions by midyear reports alongside measurable synergy realization validating investment returns [S14][N2]. Competitive pricing environment shifts among peers will test Marex’s ability to maintain market-making spreads amid evolving electronic trade venue dynamics.

In summary, Marex Group plc’s integrated platform serving diverse segments within financial services is positioned strongly after delivering substantial top-line growth combined with enhanced profitability supported by opportunistic acquisitions balanced against disciplined capital deployment ensuring robustness amid evolving regulatory landscapes.

This report is based entirely on information publicly available as of March 25, 2026. It does not constitute investment advice or recommendations regarding securities or other investments related to Marex Group plc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments