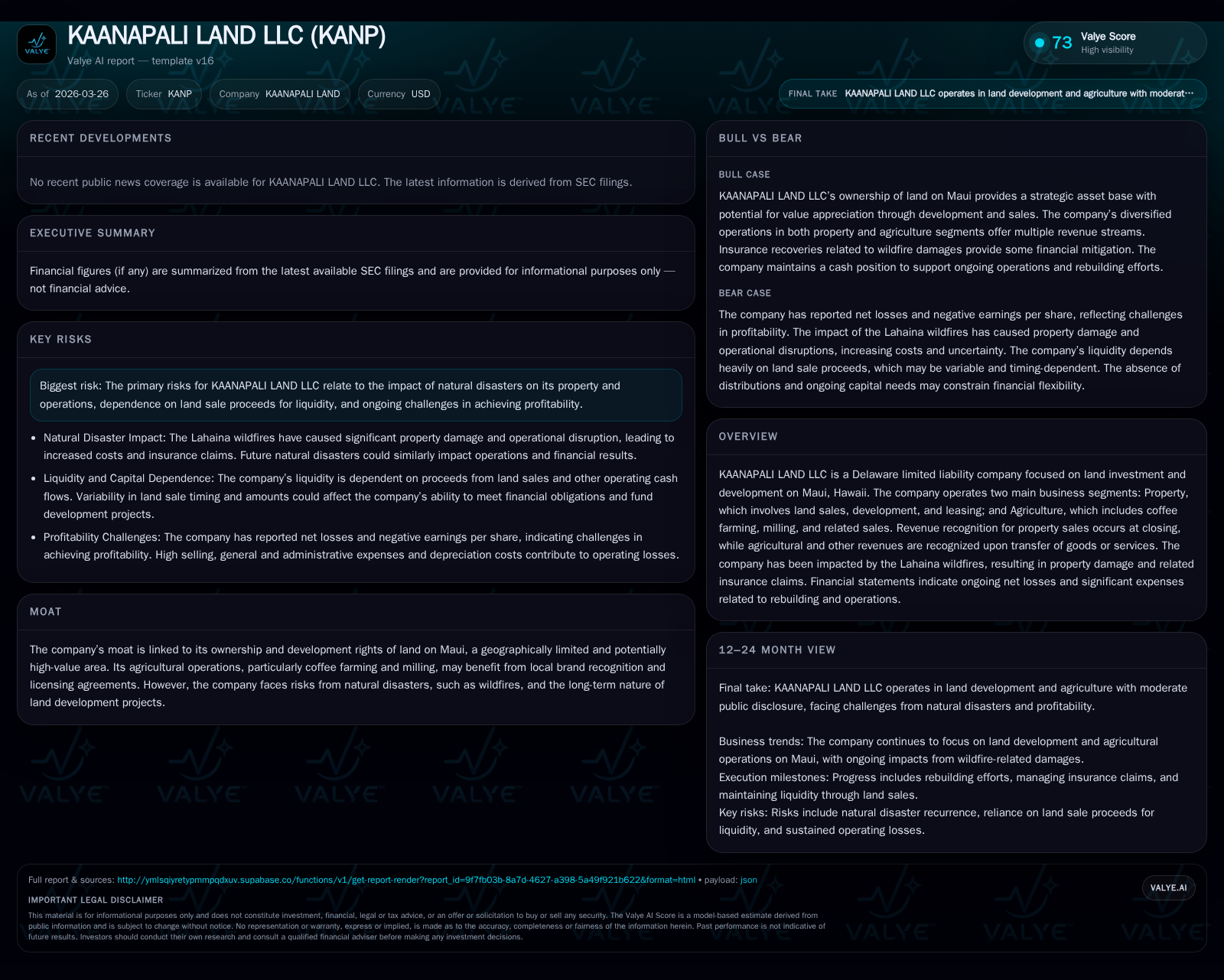

KAANAPALI LAND LLC: Recovering from Wildfires and Shaping Maui’s Growth Potential

The company faces the dual challenge of rebuilding after Lahaina wildfires while advancing long-term land development and agricultural operations.

KAANAPALI LAND LLC’s recent financials reflect the continuing impact of external shocks including wildfire damage and a slowing Maui real estate market. After a -15.7% revenue decline in 2025 and sustained operating losses, the company is focused on recovering asset value and restarting development on its constrained Maui land holdings. Agricultural operations offer diversification but limited near-term cash flow support. Cash reserves stand at approximately $15.8 million, with liquidity closely tied to timing of land sales and insurance recoveries. Key risks remain regulatory delays, natural hazard recurrence, and market absorption pace.

Historical Performance: Declines Amid External Shocks and Development Timelines

KAANAPALI LAND LLC's revenue trajectory over the past four fiscal years reveals significant volatility reflective of the unique challenges facing Maui’s land development sector. After peaking at $9.22 million in 2022, revenues declined sharply to $5.25 million in 2023 before further dropping to $1.95 million in 2024 and down another 15.7% to $1.65 million in 2025 [F1]. This downward trend mainly tracks the slowdown in property transactions following the Lahaina wildfires which disrupted both supply-side readiness and buyer appetite.

Operating income mirrored this drama: positive albeit modest earnings of $515K in 2022 turned into a breakeven scenario in 2023 ($50K), then shifted materially into losses of -$7.54 million (2024) and -$5.38 million (2025). Although operating losses eased somewhat last year by nearly 29%, persistent negative margins highlight challenging cost structures exacerbated by wildfire recovery efforts [F1].

Similarly, net income swung from a profit peak of $3.71 million (2023) toward widening losses of -$1.09 million (2024) and further deepening to -$3.73 million (2025), underscoring ongoing cash burn and expense pressure during this rebuilding phase [F1]. Operating cash flow exhibited an even steeper descent—from positive $8.15 million (2023) down to negative $2.77 million (2024) then nearly doubling that outflow to -$5.92 million last year—which reflects deferrals or challenges in converting land assets into sale proceeds promptly [F1]. Capital expenditures peaked mid-period at nearly $3 million (2024) before being proactively curtailed by over 47% in 2025 amid heightened financial discipline [F1].

Overall equity showed relative stability despite earnings volatility—hovering near $80–83 million—indicating a robust asset base that supports longer-term recovery ambitions provided operational hurdles can be managed effectively [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -4 | -6 | -5 | -15.7% | -241.5% |

| 2024 | 2 | -1 | -3 | -8 | -62.9% | -129.4% |

| 2023 | 5 | 4 | 8 | 0 | -43.0% | +30.1% |

| 2022 | 9 | 3 | 3 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -4.8 |

| 2024 | -6 | -1.3 |

| 2023 | 6 | 4.4 |

| 2022 | 3 | 3.6 |

Source: SEC companyfacts cache [F1].

Revenue recognition occurs upon closing for property sales; agriculture recognizes sales upon customer transfer [S4].

Wildfire Impact: Operational Disruptions and Asset Impairments on Mullawa's Lands

The Lahaina wildfires represent an acute operational shock for KAANAPALI LAND LLC’s property portfolio as well as its agricultural assets—specifically the company’s coffee mill infrastructure—which suffered significant physical damages [S1][S4]. This event initiated asset impairment reviews mandated under GAAP, accounting for potential reductions in recoverable carrying values of impacted real estate holdings.

Direct consequences have included escalating expenses related to rebuilding efforts such as replacement equipment procurement for the coffee processing facilities alongside engineering and planning costs intended to restore productive capacity [S4]. The push-pull between replacing damaged assets versus conserving cash has led to revised capital expenditure budgeting with a noticeable pullback from prior years’ levels.

Meanwhile, insurance claim processes are ongoing with coverage yet uncertain, adding complexity to cash flow forecasting given that proceeds will play a pivotal role in funding restoration without heavily relying on external financing mechanisms at least in the short term [S1][S4]. The wildfire’s residual effect also extends into marketability concerns for affected property assets as prospective buyers weigh risk premiums tied to natural hazard exposure.

Development Pipeline and Agriculture: Navigating Entitlements, Market Demand, and Brand Value

On the development front, KAANAPALI LAND continues advancing its strategic Kaanapali 2020 project along with other initiatives spanning Puukolii Village Mauka lands targeting an urban growth footprint recognized by Maui County’s General Plan updates since 2012 [S1]. Realization of these projects hinges on successful navigation of complex entitlement processes including:

- State-level land-use reclassification shifting parcels from agricultural designation toward urban classification,

- Obtaining corresponding County community plans amendments,

- Securing precise zoning alignments within the Maui County General Plan framework.

The pace of these approvals injects uncertainty into cash flow timelines since delayed rezoning or additional government mandates can stall vertical construction starts or parcel offerings.

Complementing land development is KAANAPALI LAND’s agricultural operation focusing on coffee farming, milling, and marketing through local brand licensing which provides an alternative revenue stream though currently limited relative scale compared to core property sales business [F1][S1]. Coffee crop cycles introduce seasonality into agricultural revenues with current production practices emphasizing sustainable inventory valuation using average cost methods—a pertinent factor given capital intensive nature of farming inputs such as labor, fertilization, irrigation, fuel, plus depreciation associated with farm equipment [S4].

Although agriculture diversifies income sources slightly mitigating sole reliance on real estate market conditions, it does not materially offset swings from development segment given scale differences.

Liquidity and Capital Structure: Managing Cash Flows Under Sales-Dependent Funding

Liquidity management remains critical for KAANAPALI LAND considering that its primary source of significant cash inflow derives from net proceeds of land parcel sales completed during the fiscal period [S1]. Cash & equivalents stood at approximately $15.8 million as of December 31, 2025—a decrease from around $21 million earlier that year—financing working capital needs including wildfire-related reconstruction expenditures as well as ongoing regulatory compliance costs encompassing environmental remediation obligations and engineering projects associated with site drainage and utilities upgrades [F1][S4][S19].

The company maintains prudent visibility over its liquidity runway but recognizes it is influenced by factors outside immediate control:

- Timing uncertainties around closing dates for property sales,

- Potential delays or partial settlements relating to insurance claims from wildfire damages,

- Credit risk exposure notably concerning a receivable linked to Newport Hospital Corporation (NHC). This particular account has been fully reserved ($~1M), due to arbitration proceedings alleging wrongful delay claims stemming from Infrastructure Improvement Agreement disputes impacting site developments originally planned for healthcare-related use on KLMC-administered parcels held by KAANAPALI LAND subsidiaries [S8][S21][S26].

Absent sufficient liquidity replenish from these avenues over time horizons required by obligations could necessitate engagement with alternate financing sources although no definitive arrangements have been disclosed so far [S4][S10].

Financial Returns and Capital Allocation: Persistent Losses vs. Asset Base Strength

Examining returns through available data yields an approximate return on equity (ROE) figure near negative 4.8%, calculated using reported net income relative to shareholders’ equity near $77 million at fiscal year-end 2025 [F1]. The persistent losses underscore elevated expense levels amid restructuring phases post-disaster.

Free cash flow also underscores strain with a calculated deficit close to $7.5 million after accounting for operating cash outflows (-$5.92M) netting against reduced capex outlays ($1.58M) during the same period—a pattern reflective of intensifying liquidity demands typical when balancing asset restoration while awaiting transactional inflows from gradual real estate sales cycles [F1].

Given these dynamics alongside stated company policy suspending dividend distributions indefinitely due to capital reinvestment priorities—a clear signal that shareholder returns remain subordinated to operational stabilization—and no share repurchase activity noted recently, capital allocation discipline appears firmly committed towards preserving enterprise value rather than near-term yield generation [S1][F1].

Forward-Looking Risks and Opportunities: Regulatory Dynamics and Natural Hazard Mitigations

The broader Hawaiian development environment presents both opportunities tethered tightly to island growth parameters as well as notable risk premiums discounted by market participants considering:

- Protracted permit approval windows driven by state and county agency rigor particularly concerning urban growth boundary expansions coupled with environmental impact assessments,

- Risk inflation via increased construction material costs compounded recently by global supply chain disruptions,

- Labor market constraints within Maui limiting availability skilled trades requisite for timely project delivery,

- External macro influences such as travel industry fluctuations impacting tourism which indirectly bear on local economic strength underpinning real estate demand,

- Continued vulnerability exposure stemming from natural hazards like wildfires requiring enhanced mitigation strategies embedded early within project designs aligned with updated county resilience standards [S28][S29].

Navigating these facets compels recognition that development activities command inherent premium compensation reflecting complexity beyond typical greenfield suburban projects prevalent elsewhere nationwide.

What to Watch: Critical Upcoming Approvals, Insurance Recoveries, and Market Absorption Rates

Looking forward entails close monitoring of:

- Progress milestones related specifically to rezoning applications relevant to flagship development parcels including Kaanapali Coffee Farms mauka sectors;

- Resolution timelines surrounding insurance claim settlements which will dictate available funding duration for reconstruction efforts absent new financing injections;

- Market appetite gauges capturing post-wildfire absorption rates for land parcels signaling recovery trajectory within Maui real estate markets given geographic constraints.

These indicators will provide granular insight into how effectively KAANAPALI LAND can translate geographic advantage within Hawai‘i’s island ecosystem into renewed value creation amidst lingering headwinds posed by prior environmental catastrophes alongside normative real estate cyclical pressures.

This analysis presents purely factual observations based strictly on publicly available SEC filings through early 2026 and company archival data snapshots; it does not constitute investment advice or endorsement nor project specific financial outcomes beyond stated disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments