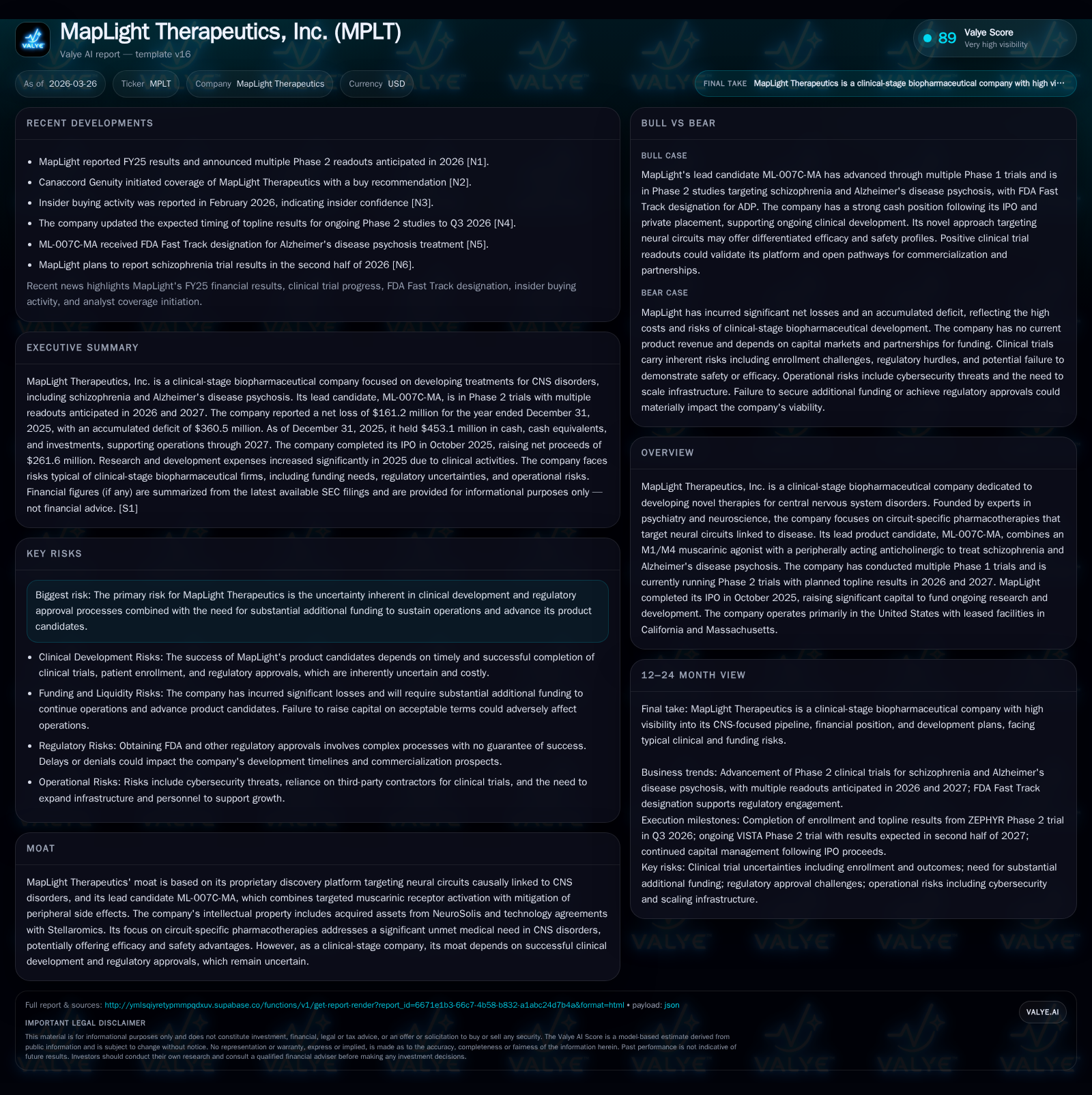

MapLight Therapeutics Advances Circuit-Specific CNS Pharmacotherapies With Strong Capital Foundation

MapLight is progressing through pivotal clinical stages of its lead CNS therapy backed by a well-capitalized balance sheet following its recent IPO.

MapLight Therapeutics operates at the intersection of neuroscience and pharmacology with a proprietary circuit-specific drug discovery platform addressing central nervous system disorders. Having completed multiple Phase 1 trials for its lead candidate ML-007C-MA and advancing Phase 2 studies, the company has established a robust financial position through its October 2025 IPO. Pre-revenue with significant operating losses typical of clinical-stage biotechs, MapLight's capital resources enable sustained R&D investment and clinical development over the near term. Upcoming Phase 2 data readouts in 2026–2027 represent critical milestones that will shape future valuation and strategic options amid ongoing regulatory and funding risks.

Founded on Circuit-Specific Innovation: Historical Growth and Investment Trends

MapLight Therapeutics has embraced a rigorous translational neuroscience approach, developing targeted pharmacotherapies that modulate neural circuits specifically implicated in central nervous system disorders such as schizophrenia and Alzheimer's disease psychosis. This circuit-centric model differentiates it from conventional approaches that broadly target neurotransmitter systems without spatial specificity. Since inception, the company's financial performance reflects significant investments in research and development (R&D), driving deep losses typical for clinical-stage biopharma entities.

According to the fiscal year-end 2025 disclosures, MapLight reported an operating loss of approximately $169 million and a net loss of about $161 million ([F1]). These losses largely stem from advancing ML-007C-MA through multiple phase clinical trials, supported by extensive laboratory infrastructure requiring capital expenses primarily related to leasehold improvements amortized over the terms of their long-term facility leases ([S10],[S12]). Notably, lab equipment with an estimated useful life of three years underpins experimental activities. The company attributes these sizable operating losses to expenses needed for progressing its lead candidate from phase 1 completion into mid-stage clinical evaluation.

The company's investment pattern shows steady increases in R&D spend, augmented by personnel costs, outsourcing to contract research organizations (CROs), clinical trial materials manufacturing, and trial execution costs. Additionally, facility-related expenses have incrementally risen due to expansions in leased research space in California and Massachusetts ([S7],[S10],[S12]), supporting complex CNS pharmacology work requiring advanced instrumentation and trial logistics.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Table summarizes MapLight's latest annual financial performance as of year-end 2025 ([F1]).

IPO and Capital Structure: Building a Strong Financial Base for Development

In October 2025, MapLight successfully completed its initial public offering (IPO), selling nearly 17 million shares at $17 per share for gross proceeds of $288.4 million. After underwriting discounts and expenses, net proceeds approximated $261.6 million. Concurrently, a private placement added roughly $7.5 million net. Upon IPO consummation, all outstanding redeemable convertible preferred stock converted into common shares eliminating prior preference structures ([S6],[S8]).

These capital injections dramatically enhanced liquidity with cash, cash equivalents, and investments climbing above $450 million by December 31, 2025. Current assets stood at about $325 million against current liabilities near $16 million—yielding an impressive current ratio exceeding 20x—a highly favorable liquidity position providing significant runway for ongoing multi-phase trial commitments ([F1],[S5],[S8]).

The capital structure transition from convertible preferred stock towards equity common stock enhances financial flexibility critical for supporting multi-year biopharmaceutical development cycles requiring iterative trial designs paired with costly R&D activities. The freshly bolstered balance sheet functions as an equity financing vehicle underpinning MapLight’s extended clinical efforts.

Clinical Progress and Upcoming Catalysts: What to Watch in 2026–2027

MapLight’s lead clinical asset ML-007C-MA combines M1/M4 muscarinic receptor agonism with a peripherally restricted anticholinergic component designed to selectively engage CNS targets while minimizing systemic side effects—a differentiated mechanism within neuropsychiatric therapeutics. Phase 1 trials completed successfully enabling progression into Phase 2 trials focusing on schizophrenia and Alzheimer's disease psychosis indications.

The company is currently conducting multiple Phase 2 trials with topline data releases anticipated throughout 2026 and into early 2027 ([N1],[S1]). These readouts will be pivotal catalysts for validating muscarinic receptor specificity efficacy signals alongside safety profiles within defined patient populations using sophisticated biomarker endpoints.

Navigating Operational Expenses: The R&D Spend Behind CNS Drug Development

Operational expenses predominantly consist of research & development expenditure reflecting the high fixed cost nature associated with CNS drug discovery that requires specialized laboratory equipment, dedicated trial clinics, biomarker assay platforms along with substantial outsourcing arrangements.

Leasehold improvements contributing to property and equipment assets are amortized based on lease terms ranging up to fifteen years but typically shorter depending on spaces dedicated to clinical or laboratory applications ([S10],[S12]). Lease costs aggregated approximately $1.67 million during fiscal year ending December 31, 2025 spread across primary facilities located in Redwood City CA and Burlington MA—specialized areas essential for advanced neuropharmacological assays and tailored CNS trials ([S7]).

Incremental rises in R&D expenses reflect ongoing patient enrollment activities aligned with operational leverage dynamics inherent within small-to-mid-sized biotech firms moving assets through costly translational pipelines.

Assessing Liquidity, Cash Flows, and Burn Rate in a Pre-Revenue Company

As anticipated across clinical-stage biopharmas developing novel therapies without commercial products yet available for sale, MapLight exhibits persistent negative free cash flow driven by continuous investments mostly funded through equity raises rather than operating revenue streams.

Year-end 2025 cash flows reveal operating cash outflows near $139 million combined with consistent modest capital expenditure underlining intense resource dedication towards executing phase gated development plans ([F1],[S8]). Given approximately $47 million cash & equivalents plus substantial liquid investments representing safe harbor Treasury securities along with money market funds valued over $260 million collectively contribute to high liquidity buffers ensuring operational continuity beyond immediate clinical milestones ([S19],[S20]).

Although exposure to investment price volatility exists due to fair value accounting treatment primarily around Level-2 instruments like corporate debt securities or commercial paper holdings,the portfolio composition emphasizes preservation given near-term funding requirements.

Capital Allocation Strategy: Balancing R&D Investment Amidst Clinical Development Priorities

Consistent with industry norms at this stage MapLight neither declared dividends nor executed share repurchase programs as reinvestment into development programs takes priority amid milestone-driven capital deployment strategy ([S18]). Capital allocation policies reflect disciplined prioritization towards advancing internal pipeline progressions including expensive mid-stage clinical trials matched by governance oversight directing usage towards high expected return scientific investments rather than short-term return distributions.

This approach mitigates dilution risks by staging expenditures aligned with pivotal data readouts while conserving sufficient resource reserves should additional financing rounds be required for phase transitions or expanded indications.

Risk Profile: Regulatory Uncertainty and Funding Dependencies

Regulatory pathways for CNS therapeutics remain challenging due to heterogeneous patient populations coupled with complex efficacy endpoint design considerations; accordingly MapLight faces significant risk of trial attrition or regulatory delays which could materially impact timelines or program viability ([S4],[S11],[N1]).

Moreover ongoing reliance on capital raises introduces dilution concerns if additional funding rounds occur under unfavorable market conditions ([N2]). Cybersecurity governance plays an important operational role given sensitive patient trial data managed across platforms; oversight rests with audit committees ensuring mitigation against breaches potentially disrupting operations or causing reputational harm ([S1]).

Potential legal proceedings presently do not materially impact operations but remain inherent risk factors usual for firms engaging multiple third-party contracts across jurisdictions.

Strategic Partnerships Supporting Platform Differentiation

While specific details were limited in available filings regarding intellectual property acquisitions or license agreements such as Stellaromics or NeuroSolis assets cited in external summaries , MapLight's proprietary circuit-specific platform remains central to its competitive positioning.

This report is intended solely for informational purposes reflecting analysis based on publicly available filings dated up to March 26, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments