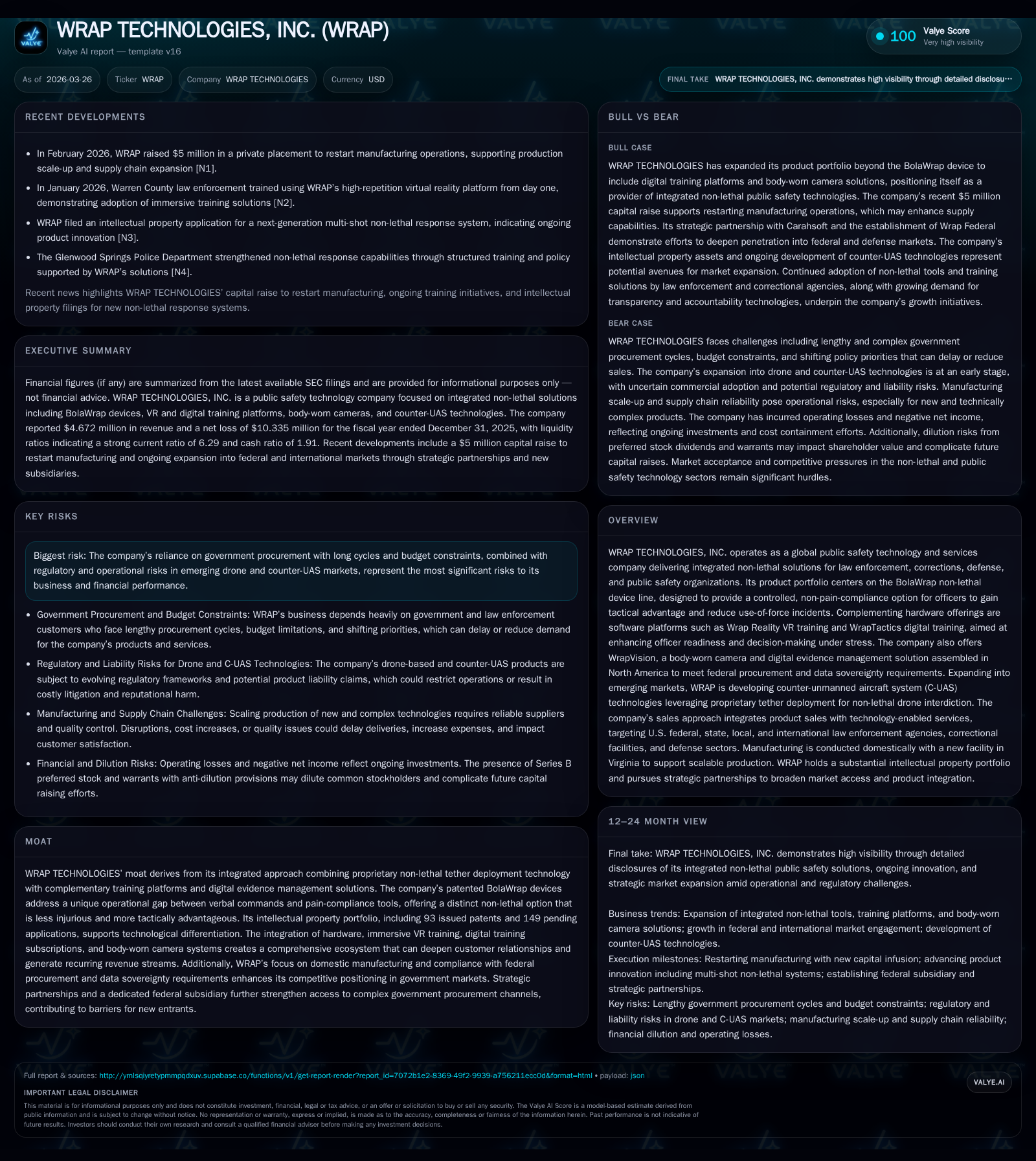

WRAP Technologies Expands Non-Lethal Public Safety Solutions with Emerging Federal and Counter-Drone Initiatives

The company shifts from a single-product focus to integrated non-lethal tools and training amid operational losses and evolving government procurement dynamics.

WRAP Technologies, Inc. has transitioned from primarily commercializing its BolaWrap non-lethal device to offering a diversified portfolio integrating hardware, software, and services for law enforcement and defense sectors. Despite modest revenue growth driven by technology-enabled services, net income remained negative in 2025, reflecting ongoing operating losses and investments in new product categories such as body-worn cameras and counter-unmanned aircraft systems (C-UAS). The company navigates challenges typical of government procurement cycles, budget constraints, competitive drone markets, and regulatory compliance. Its capital structure depends on equity raises, with cash reserves sufficient for near-term operations but cash flow negative amid restructuring efforts. Future growth relies on deeper agency adoption of integrated programs combining tools, training, and tactics.

Company Overview

WRAP Technologies, Inc. is a public safety technology company delivering integrated non-lethal solutions designed primarily for law enforcement globally. Its flagship product is the BolaWrap tether deployment device intended as a controlled alternative between verbal commands and painful compliance tools to reduce injuries during use-of-force encounters [S1][S4]. Since launching its initial product in late 2018, WRAP has expanded beyond hardware into complementary software and services including immersive VR training (Wrap Reality), digital tactical training platforms (WrapTactics), body-worn cameras (WrapVision), and emerging counter-unmanned aircraft systems (C-UAS) technologies under the MERLIN program [S1][S4][S10]. The company’s mission emphasizes safer enforcement outcomes by equipping officers with integrated tools, training, and tactics.

Historical Performance

WRAP's trailing four years reveal fluctuating but generally declining revenue following initial rapid growth:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5 | -10 | -10 | -13 | +3.7% | -75.9% |

| 2024 | 5 | -6 | -8 | -16 | -26.5% | +80.6% |

| 2023 | 6 | -30 | -17 | -19 | -23.8% | -71.5% |

| 2022 | 8 | -18 | -15 | -18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -10 | -89.9 |

| 2024 | 120000 | -8 | -2350.0 |

| 2023 | 58000 | -17 | -955.4 |

| 2022 | -15 | -65.1 |

Source: SEC companyfacts cache [F1].

Revenue contracted significantly since peaking above $8 million in FY2022 before stabilizing around $4.5-$4.7 million in FY2024-25 with modest growth from technology-enabled services [F1][S14]. The decline largely stems from decreased hardware sales amid shifting distribution strategies and returns totaling $0.53 million related to go-to-market adjustments in 2025 [S14]. Operating losses remain material but narrowed year-over-year by over $2 million due to cost containment measures focusing on personnel reductions, lower advertising spend, and sharply reduced R&D expenses—from $2.3 million in 2024 to just $56 thousand in 2025 [F1][S13][S14]. Despite these savings, profitability remains elusive.

Net income worsened again in 2025 largely due to a one-time impairment charge partially offsetting operational improvements [F1][S13]. Cash flow from operations deteriorated with growing net losses reaching a $10.3 million outflow compared to about $8 million prior year as inventory management tightened [F1][S24]. Capital expenditures remained modest at around $100k reflecting scaled-back development investment.

Business Model & Products

WRAP generates revenue via two primary streams:

- Product sales: BolaWrap devices, consumable cassettes, accessories, body-worn cameras assembled domestically for federal compliance, and VR hardware components.

- Technology-enabled services: Subscription-based WrapTactics tactical training software; digital evidence management; managed services including policy consulting; professional training delivered online or in-person.

Sales evolved from a channel-based model toward direct sales supported by strategic distributors covering all U.S states plus global distribution across sixty countries [S4][S7]. Key milestones include acquisition of NSENA (immersive VR training) in 2020 and Intrensic (body-worn cameras & evidence management) in mid-2023 expanding capabilities beyond BolaWrap devices into integrated ecosystems combining tools, data capture, and analytics for non-lethal operational effectiveness [S1][S4].

Training plays an important role pre- and post-sale to drive adoption within agencies where judicial or political stakeholders may influence purchase decisions [S7]. Some training is offered free as customer engagement while premium WrapTactics subscriptions add recurring revenue potential.

A notable strategic initiative is MERLIN C-UAS technology leveraging proprietary tether deployment for non-lethal drone interdiction targeting defense and infrastructure protection markets—a nascent area requiring regulatory approvals where competitive pressure is emerging [S10][S22].

To better serve the Federal segment including DoD and Homeland Security customers WRAP formed Wrap Federal subsidiary in late 2025 focusing on federal procurement vehicles compliant with Trade Agreements Act standards through partnerships such as Carahsoft Technology Corp., increasing accessibility within government channels [S1][S18][S7].

Geographic & Customer Concentration

In FY2025 Americas accounted for approximately $2.86 million of gross revenue while Europe/Middle East/Africa surged to $2.32 million from just $0.08 million previous year reflecting successful international expansion particularly through internationally oriented distributors; Asia-Pacific contributed a smaller fraction ($0.02 million) [F1,S5,S12]. Customer base remains concentrated: one distributor represented roughly 38% of total revenue with another about 10%, creating meaningful credit risk exposure balanced by contractual minimums allowing WRAP to shift channels if needed [F1,S5,S15,S23].

As revenue mix expands toward federal contracts via Wrap Federal along with new C-UAS products targeting defense end-markets the geographic mix may diversify but procurement cycles tend to be longer.

Growth Prospects & Outlook Analysis

WRAP's future growth hinges on:

- Deepening BolaWrap agency adoption converting pilots into full agency-wide standard issue promotes recurring cassette sales plus reinforces integration into use-of-force protocols enhancing stickiness across products/services.

- Expanding technology-enabled service revenue through WrapTactics subscriptions; managed services like policy consulting align with trends toward programmatic recurring revenue models prevalent in public safety tech.

- Penetrating U.S federal government entities leveraging Wrap Federal subsidiary under Carahsoft reseller agreements increases addressable market size though complex purchasing processes may delay revenues.

- Commercializing MERLIN counter-UAS program could unlock defense/HLS use cases; however development remains early subject to technical validation & regulatory certification risks amidst competition from well-funded incumbents impacting traction pace.

- Strengthening international distributor networks continues though geopolitical sensitivities concerning export controls & regulatory approvals persist especially around surveillance & non-lethal technologies.

Limitations include extended government sales cycles compounded by budget constraints amid shifting political priorities impacting public safety funding allocations as well as concerns around novel drone interdiction technologies given airspace safety considerations.

Monitoring contract awards from Department of Defense/Homeland Security alongside early-stage C-UAS pilot outcomes will be critical indicators—explicit guidance is not provided though management anticipates improving operating efficiencies supported by recent capital raises [F1,S6,S24].

Capital Allocation & Returns Analysis

The company operates at a loss with approximate ROE near -89.9% based on net loss relative to equity elevated due to accumulated losses offsetting paid-in capital infusion [F1]. No dividends have been declared or paid recently reflecting reinvestment priority typical of early-stage tech firms focused on growth.

Equity capital dominates funding sources: gross proceeds exceeded $10 million during FY2025 including private placements issuing common stock plus warrants concurrently improving balance sheet liquidity temporarily supporting runway under current outflows approximating above $10 million annually from operations alone [F1,S6,S25]. The company reclassified certain warrant liabilities into equity eliminating future non-cash volatility impacts enhancing financial statement stability post recent amendments [S6,S16].

CapEx spending remains minimal consistent with outsourcing manufacturing except capitalized intangible asset investments consistent with patent portfolio maintenance encompassing over ninety patents issued plus pending applications fortifying intellectual property moats surrounding tether deployment methods beyond core BolaWrap device line [F1,S8].

Management emphasizes prudent alignment of operating structure balancing sales/marketing throughput alongside controlling administrative costs while focusing R&D mainly on incremental innovation versus large-scale new product development given constrained liquidity during transition toward diversified portfolio strategy.

Risks & Challenges Summary

Key risks include:

- Dependence on government procurement exposes WRAP to long approval timelines subject to political budget shifts potentially delaying contract awards or reducing volumes diminishing revenue predictability.

- Emerging counter-drone marketplace features rapid technological evolution coupled with regulatory uncertainty posing commercialization timing risks amid competition from entrenched players backed by defense budgets.

- Body-worn camera solutions demand stringent data privacy/compliance adherence including Criminal Justice Information Services policies complicating rollout requiring ongoing cybersecurity investments potentially increasing costs.

- Customer concentration risk linked to few distributors highlights credit risk vulnerability though contractual terms permit channel adjustments if warranted.

- Potential litigation exposure related to intellectual property disputes or contractual disagreements could require costly settlements adversely affecting financials if materialized unexpectedly .

These factors underscore the importance of maintaining operational discipline combined with strategic execution leveraging unique integrated ecosystem offerings differentiating WRAP beyond single-product reliance.

Disclaimers: This analysis summarizes WRAP Technologies’ publicly available information without forecasting future performance or offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments