FB Bancorp’s Modest Profit Turnaround and Strategic Asset Sale Reshape Its Regional Banking Focus

FB Bancorp, through its bank subsidiary Fidelity Bank, navigates a modest profit recovery in 2025 alongside divestiture of mortgage assets.

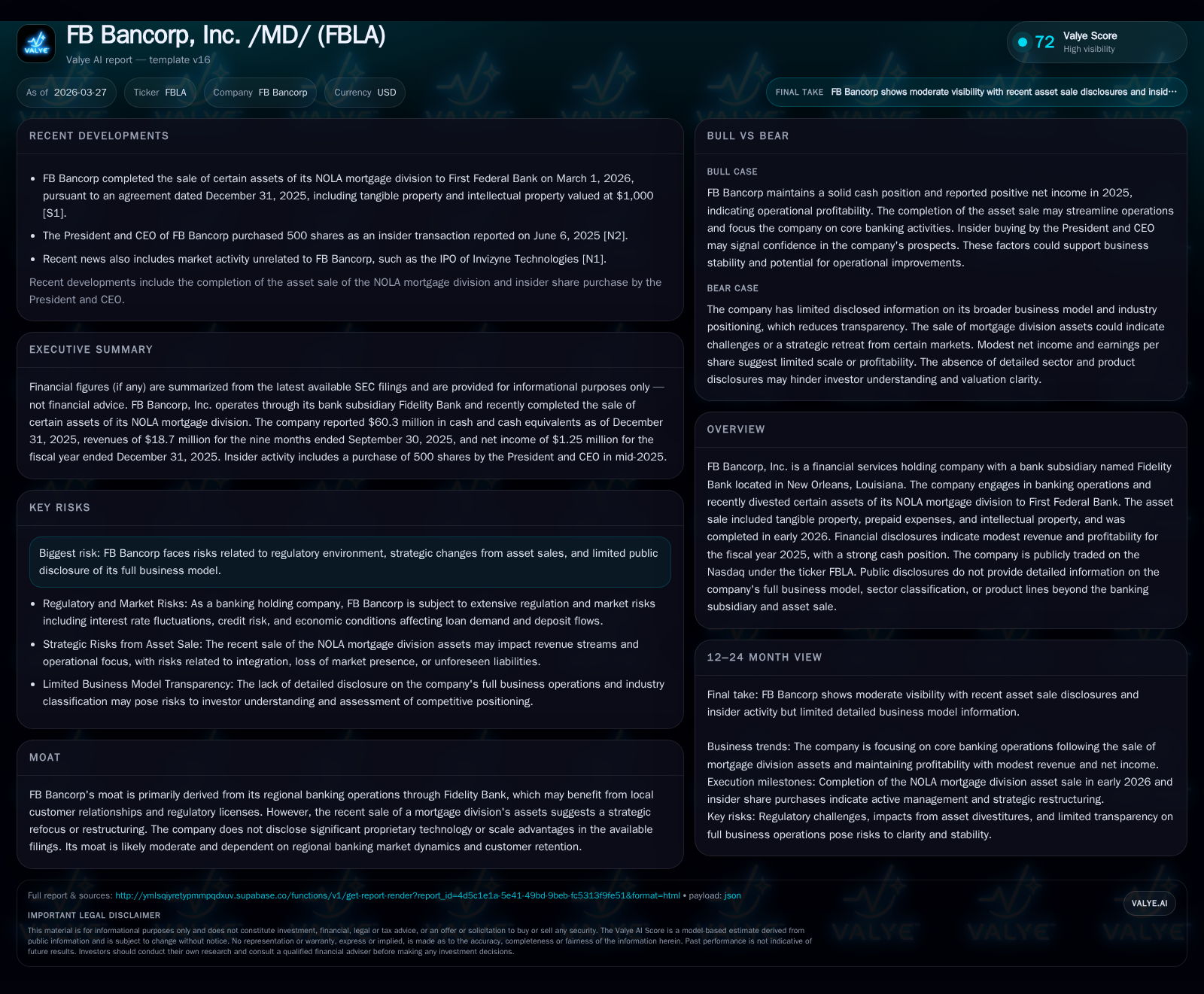

FB Bancorp, Inc., headquartered in New Orleans and operating through Fidelity Bank, delivered modest profitability in fiscal 2025 after a sizable net loss the year prior. The company divested certain assets of its NOLA mortgage division to First Federal Bank early in 2026, signaling a strategic refocus on core banking operations. While revenue growth was muted, positive trends in operating cash flow accompanied increasing capital expenditures. Despite a slight decline in equity, the firm authorized stock repurchases in late 2025 and early 2026, reflecting a shareholder return strategy amid restructuring efforts. Risks remain tied to regulatory constraints and the implications of ongoing asset sales.

Company Overview

FB Bancorp, Inc., listed on Nasdaq under FBLA, is a financial holding company primarily operating through its bank subsidiary Fidelity Bank based in New Orleans, Louisiana. The company’s business model centers on regional banking services—deposit taking, lending, and associated financial products—anchored in local customer relationships and regulatory frameworks specific to its footprint.

In early 2026, FB Bancorp completed a notable transaction involving the divestiture of various assets from its NOLA mortgage division to First Federal Bank of Lake City, Florida [S3][S10][S18]. This sale comprised tangible property, prepaid expenses, and intellectual property valued nominally at $1,000. This move signals a deliberate strategic shift away from mortgage origination or servicing activities towards concentrating resources on its core regional bank operations.

Historical Performance and Growth Drivers

The company’s recent historical financials reveal a turnaround from losses to profitability after challenging prior years. Reported net income for fiscal year 2025 stands at $1.25 million compared to a loss exceeding $6.2 million in fiscal 2024 [F1]. Revenue was recorded as $66.45 million for calendar year-end 2024; however, discrete top-line figures for fiscal year 2025 are not separately disclosed [F1].

Operating cash flow has improved markedly—from negative $3.98 million in FY24 to positive $2.76 million in FY25—demonstrating better fundamental cash generation capabilities despite ongoing investment outlays evidenced by increased capital expenditures rising about 27.5% year over year to $6.66 million [F1]. Yet free cash flow remains negative by around $3.9 million due to heavy capital spending linked possibly with technological enhancements or infrastructure improvements within the bank.

Equity declined modestly over the twelve months ending December 31, 2025, settling at approximately $314.45 million against $326.26 million at the prior year-end—a roughly 3.7% drop, perhaps reflecting share repurchases and retained earnings dynamics [F1]. The resulting approximate return on equity hovers near just 0.4%, consistent with subdued net income relative to substantial equity bases typical of banking institutions [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 1 | 3 | 7 | +120.2% |

| 2024 | -6 | -4 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -4 | 0.4 |

| 2024 | -9 | -1.9 |

Source: SEC companyfacts cache [F1].

Note: Latest disclosed revenue is for FY24; no comparable figure yet for FY25.

Strategic Moves and Future Outlook

The completion of the asset sale relating to NOLA mortgage operations represents a pivotal course adjustment for FB Bancorp [S3][S10][S18]. The deal's terms convey that First Federal Bank assumed ownership of physical assets as well as intellectual property tied to this division—a transfer that effectively offloads non-core elements.

This streamlining ostensibly allows Fidelity Bank to sharpen its focus on community banking services — lending primarily against commercial or consumer needs within its Louisiana base—and potentially improve operational efficiency.

Future growth hinges largely on strengthening these primary banking relationships as well as managing credit quality amid economic fluctuations impacting local borrowers . The absence of proprietary technology or scale economies disclosed suggests competitive advantage relies heavily on regional market presence rather than broader franchise reach or innovative platforms.

With respect to guidance or forecasted milestones directly communicated publicly or via regulatory filings since the latest annual report cutoff date: no explicit forward revenue or earnings targets are provided by management [N#]/[S#], leaving close monitoring necessary around subsequent quarterly disclosures regarding loan growth trajectory, deposit inflows, margin trends amid interest rate variability, and effective cost containment initiatives.

Capital Allocation and Shareholder Returns

FB Bancorp has actively engaged in stock repurchase programs authorized during late-2025 through early-2026 periods [S7][S8][S9][S16]. These repurchases accounted cumulatively for approximately up to 10% reductions in outstanding common shares each time, highlighting management’s inclination towards returning capital through buybacks alongside maintaining liquidity cushions.

Dividend policies are less transparent given limited public disclosure within examined periods — no significant dividend payouts were explicitly announced or detailed within recent filings.

Cash balances remain robust with about $60.3 million in cash and equivalents reported as of December 31, 2025—bolstering balance sheet flexibility even amid restructuring phases [F1]. Concurrently increasing capex indicates that portions of capital are being reinvested into operations rather than solely returned externally.

Risk Factors

Primary risks relate to regulatory frameworks governing regional banks including compliance costs and potential changes following policy shifts affecting capital requirements or lending standards [S4][S5]. Moreover, execution risk attached to the disposal of mortgage assets involves transition challenges such as customer retention loss or unforeseen operational disruptions impacting short-term performance.

Transparency constraints arise from limited detail regarding full business lines beyond Fidelity Bank and recent asset sales; investor understanding is thus dependent on periodic SEC disclosures absent broader strategic narrative clarity .

Conclusion

FB Bancorp manifests signs of incremental recovery and strategic recalibration post the sharp losses experienced earlier with its shift away from mortgage asset holdings via sales executed early in 2026. While financial metrics depict modest profitability scaling cautiously against an expansive equity base accompanied by sound liquidity levels and active share repurchasing activity, future results will hinge notably on steady execution within core regional banking domains compounded by macroeconomic conditions impacting loan demand and credit quality. Monitoring forthcoming periodic reports will be critical for updated insight into revenue progression and management’s articulation regarding long-term growth trajectories.

This analysis is based strictly on available public disclosures and data as referenced; it does not constitute investment advice nor an endorsement of any financial decisions regarding FB Bancorp, Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments