Bogota Financial Corp. Unlocks Growth Through Loan Portfolio Restructuring and Local Market Focus

Strategic loan underwriting and balance sheet initiatives have driven Bogota Financial's transition from losses to profitability in a competitively dense New Jersey market.

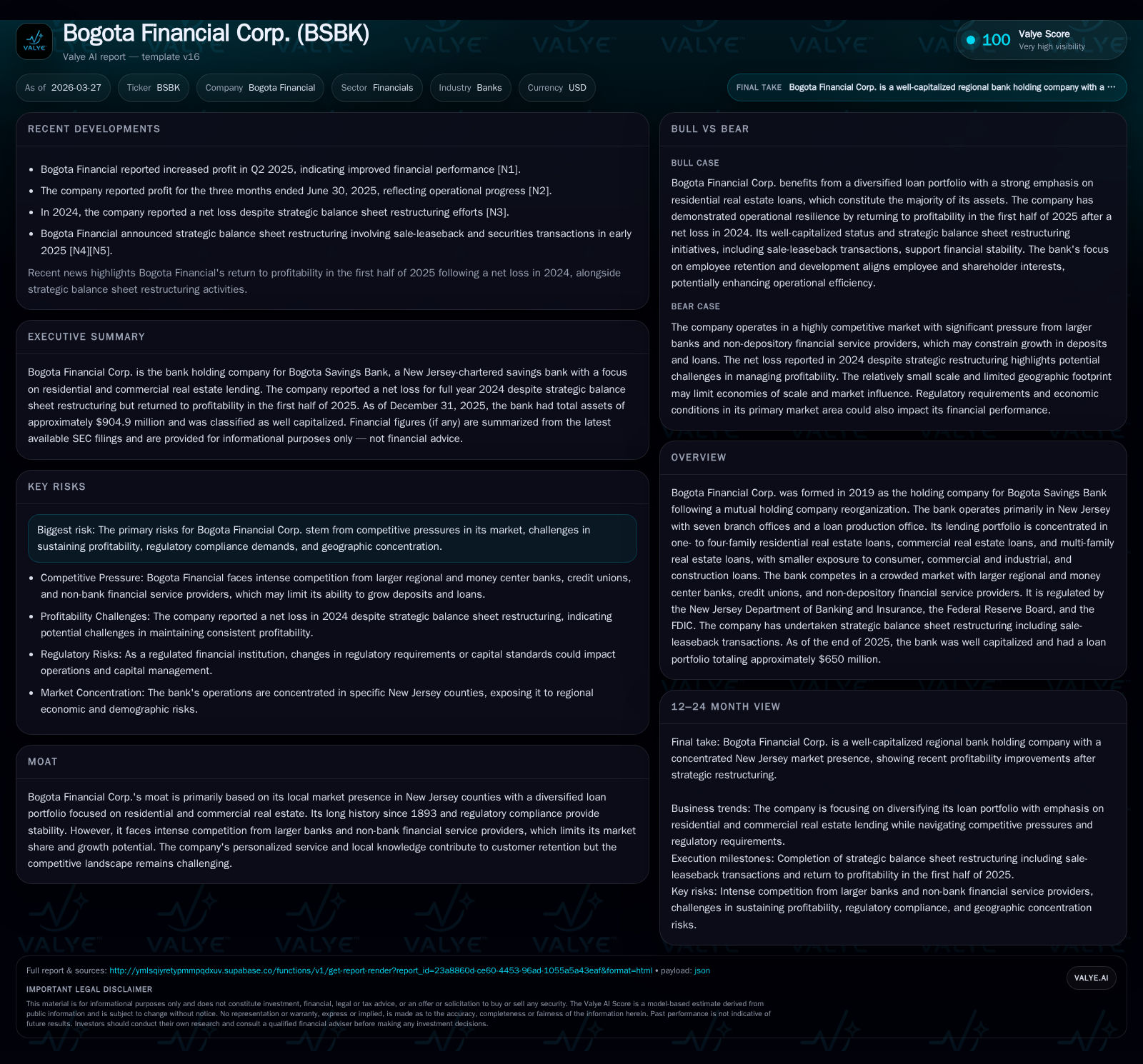

Bogota Financial Corp. reversed a net loss of $2.17 million in 2024 to a net income of $2.09 million in 2025, reflecting effective loan portfolio management and capital discipline. The bank concentrates on diversified real estate lending—residential, commercial, and multi-family—underpinned by rigorous underwriting safeguards such as debt service coverage ratios and loan-to-value limits. Despite formidable competition from larger regional banks and non-depository lenders in New Jersey, Bogota leverages its local history and personalized service to maintain a niche presence. The firm remains well capitalized, navigating regulatory frameworks prudently while optimizing liquidity through deposit pricing and strategic balance sheet management.

Historical Performance and Earnings Recovery

Bogota Financial Corp.'s recent financial performance showcases a pronounced turnaround between fiscal years 2024 and 2025. In FY2024, the company posted a net loss of approximately $2.17 million but rebounded strongly to achieve net income of $2.09 million in FY2025, representing a marked year-over-year improvement of over 196% based on SEC company facts data [F1]. This earnings recovery aligns closely with an operating cash flow swing from negative $2.56 million in FY2024 to positive $3.20 million in FY2025, underscoring enhanced operational efficiency and underlying business health.

Capital expenditure discipline has been pivotal: capex dropped an eye-catching 88% from nearly $595K to just above $70K year-over-year [F1]. This curtailed investment supports the generation of strong free cash flow nearing $3.13 million in FY2025, providing liquidity headroom vital for strategic flexibility.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 2 | 3 | 70368 | +196.3% |

| 2024 | -2 | -3 | 594787 | -437.8% |

| 2023 | 1 | 1 | 318035 | -90.7% |

| 2022 | 7 | 11 | 241474 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1 | 3 | 1.5 |

| 2024 | 2 | -3 | -1.6 |

| 2023 | 4 | 1 | 0.5 |

| 2022 | 10 | 11 | 4.9 |

Source: SEC companyfacts cache [F1].

Data reflect full-year results as per latest filing [F1].

Loan Portfolio Composition and Underwriting Discipline

The bank’s lending portfolio maintains a clear focus on real estate financing concentrated within the New Jersey market footprint covering seven branches and a loan production office. At December 31, 2025 the total loan portfolio stood at approximately $650 million composed predominantly of one- to four-family residential real estate loans totaling about $444 million (68%), alongside commercial real estate loans approximating $122 million (19%), multi-family real estate loans of $59 million (9%), construction loans around $22 million (3%), commercial and industrial loans at roughly $3.2 million (0.5%) and consumer loans under $120K (<0.01%) [S19], [S24].

Underwriting protocols are stringent with defined quantitative thresholds balancing risk and return:

One- to Four-Family Residential Loans: Origination adheres broadly to Fannie Mae/Freddie Mac guidelines with fixed or adjustable rates capped on periodic resets; maximum loan-to-value ratios reach up to 80% depending on borrower profile; private mortgage insurance is mandated for loans exceeding an 80% LTV threshold [S19], [S22].

Commercial Real Estate Loans: Fixed or adjustable interest rates indexed primarily to Federal Home Loan Bank advances plus margins; terms usually do not exceed ten years amortized over up to twenty-five years; LTV ceilings hold at ~70% for internally originated loans versus ~60% via brokers; minimum debt service coverage ratio (DSCR) required is at least 1.25x with continuing borrower financial statement updates monitored regularly; personal guarantees are routinely secured where applicable [S18], [S22].

Multi-Family Real Estate Loans: For apartment buildings with five or more units within the primary market area; fixed or adjustable-rate loans indexed similarly; DSCR floors are slightly relaxed at minimums of about 1.20x; LTV caps generally around 75% for originated loans and tighter at about 60% for brokered ones; borrowers maintain reserves covering three months operating expenses plus loan payments typically held liquid within the bank’s accounts [S4].

Construction Loans: Interest-only during construction phases varying between twelve to twenty-four months subject to municipal approvals; max LTV of up to 75% for finished appraised values or stricter limits such as ~50% for raw land acquisitions; disbursements aligned with inspection certifications minimize exposure; borrower creditworthiness including experience and cash flow projections weigh heavily in approval decisions [S7], [S12].

Commercial & Industrial Loans: Adjustable-rate lines of credit or term loans secured by collateral including accounts receivable or real estate liens; DSCR targets set no lower than 1.25x; generally no unsecured exposures granted here; collateral value coverage commonly near upper bound of ~70%; personal guarantees underpin repayment assurances [S8].

Adjustable-rate loans comprise a notable portion of both residential (about one-third) and commercial portfolios enabling some natural hedging against rising rates albeit limited by lifetime rate caps typically cumulative +5%. Management acknowledges potential delinquency risks tied to payment shock should interest rates escalate meaningfully though mitigated by robust underwriting standards and borrower reserves [S22], [S8].

Competitive Positioning in the New Jersey Banking Market

Bogota Financial Corp., as holding company for Bogota Savings Bank founded in 1893 with established presence across several New Jersey counties including Bergen and Morris Counties where it operates seven branches plus a production office provides localized banking services emphasizing personalized customer engagement.

Despite its long-standing community roots acting as part of its moat alongside regulatory compliance stability—the environment is fiercely competitive given the density of institutions including large national money center banks like JPMorgan Chase or Wells Fargo along with substantial regional players such as TD Bank or PNC Bank vying aggressively for customers across retail deposits and loan products.[F1],[S26] Credit unions and emergent fintech platforms also crowd this marketplace adding further pressure on pricing margins and customer acquisition costs.

With FDIC market share estimates underscoring modest penetration metrics below one percent regionally,[S26] Bogota relies on differentiation via community commitment aligned service responsiveness matched with technical lending expertise pertinent especially in real estate-related products where local understanding presides.[F1]

Nevertheless geographic concentration entails vulnerability should localized economic slowdowns or demographic shifts impinge lending dynamics or deposit gathering capacity amid rising alternative options offered digitally at scale.[F1],[S26]

Capital Structure Stability and Regulatory Compliance

Bogota Savings Bank remains well-capitalized under federal banking regulatory standards relying significantly on exceeding thresholds defined by Basel III community bank leverage frameworks—boasting tangible common equity near $141 million as per fiscal year-end data noted in filings.[F1],[S6] Its capital ratios consistently top benchmark minima such as Tier 1 risk-based capital above required levels (>8%) and overall leverage ratios comfortably surpassing prompt corrective action standards ensuring flexible capacity for growth initiatives subject to supervisory approval.[S6]

The bank’s adoption of the Community Bank Leverage Ratio framework simplifies compliance mechanics while affirming sound capitalization relative to assets held under management totaling under $10 billion qualifying Bogota within this community bank subset.[S10],[S13]

Such robust capitalization supports not only organic lending expansion but fortifies defenses against scenario-based shocks including stressed credit events or volatile funding conditions thus enhancing counterbalance against competitive encroachment requiring eventual scale advantages.[F1],[S6]

Liquidity Management and Balance Sheet Optimization

Primary funding sources constitute retail deposits predominantly domiciled locally inclusive of individual consumers businesses plus municipalities representing roughly 6.9% of total deposits equating over $45 million which offer relatively stable funding volumes albeit price sensitive amidst competitive rate offerings.[S4],[S5] The bank supplements deposit inflows with wholesale borrowings largely via Federal Home Loan Bank advances providing tactical variability especially given fluctuating seasonal demands.[S4]

Deposit pricing practices observe weekly comprehensive reviews maintaining competitiveness without frequently resorting to aggressive high-rate offerings that could erode net interest margins while special offers occasionally target specific product types optimizing funding duration mix without elevating cost base disproportionately.[S5]

Capital Allocation Strategy: Buybacks and Investment

Capital deployment discipline is evident via material contraction in capital expenditures narrowing near seventy thousand dollars annually reflective of maintenance-level outlays consistent with Bogota’s business model focused on branch banking rather than aggressive physical expansion.[F1]

Share repurchases totaled approximately $1.13 million in FY2025 downtrend versus prior years signaling continued engagement with shareholders balanced conservatively against liquidity preservation needs amid earnings normalization following prior losses.[F1],[S15],[S16]

Dividend payment information remains less transparent lacking clear explicit disclosures hinting at limited policy activity yet necessitating ongoing monitoring given regulatory constraints tied particularly to mutual holding company structures requiring Federal Reserve Board approvals impacting distribution flexibility.[S15],[S16]

Forward-Looking Outlook and Key Considerations

While formal forward guidance is absent from public disclosures notable strategic considerations crystallize around multiple vectors shaping future performance trajectories:

- Continued emphasis on expanding commercial and multi-family real estate loan originations aims at portfolio diversification improving yield profiles responsive partly to staged asset liability management strategies balancing fixed vs adjustable rate balances appropriately under current interest rate environments.[S20]

- Interest rate sensitivity embedded within adjustable-rate loan segments warrants vigilance given potential borrower payment stress if rates rise sharply requiring monitoring for early warning signs of delinquency.

- Competitive intensity fueled by technology-driven entrants alongside consolidation among regional banks may affect market share gains or retention capabilities.

- Regulatory environment maintains evolving cybersecurity compliance demands—with active board-level governance structures ensuring information security program rigor denoting proactive risk mitigation consonant with supervisory expectations critical amid growing cyber threats.[S1]

Investors should track quarterly earnings releases notably post Q1/26 inclusive metrics around loan growth rates credit quality trends capital adequacy adjustments dividend policy updates plus any material changes disclosed around competitive posture or regulatory developments substantially influencing operating conditions.

This analysis reflects information available through March 27, 2026 from company filings without speculative forward-looking projections lacking explicit corporate disclosure mandates or publicly available guidance documents.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments