SIM Acquisition Corp. I's SPAC Model and Financial Constraints Ahead of Business Combination Deadline

SIM Acquisition Corp. I operates as a blank check company with no revenues or operating history, navigating intense competition and structural risks to complete its initial business combination before liquidation triggers.

SIM Acquisition Corp. I, a Cayman Islands-incorporated SPAC, maintains limited assets and a challenging capital structure as it seeks to finalize an initial business combination under substantial time pressure. Historical financials reflect operating losses and negative operating cash flow, while substantial risks—such as competitive deal sourcing, regulatory hurdles, and potential shareholder dilution—cast uncertainty on the timeline and terms of its business combination. Its capital allocation primarily involves servicing working capital needs through sponsor loans, with little room for dividends or buybacks, underscoring the precarious position typical of a pre-merger blank check vehicle.

Company Overview

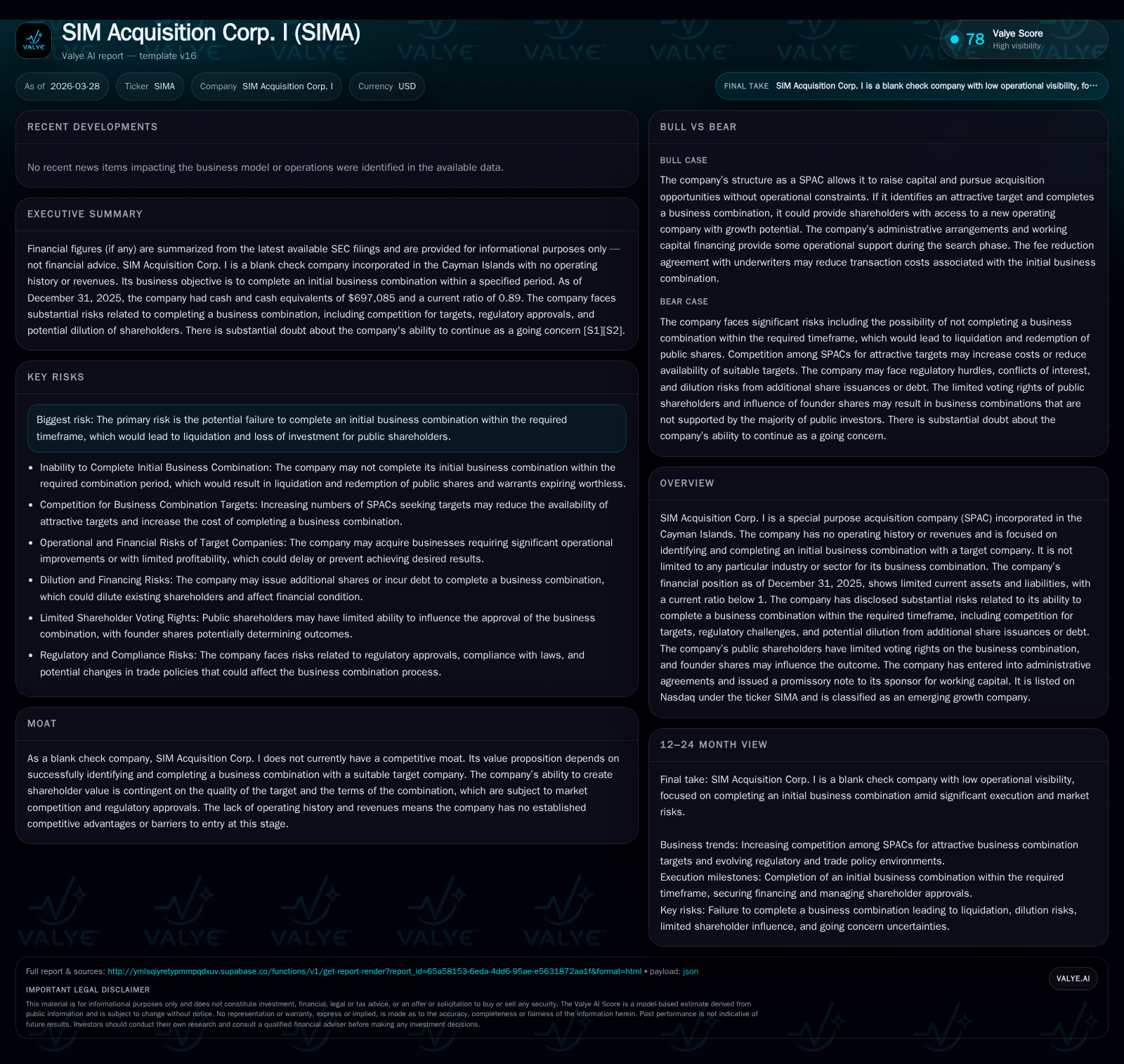

SIM Acquisition Corp. I (SIMA) is a typical special purpose acquisition company (SPAC) incorporated in the Cayman Islands. It operates as a blank check company with no revenue-generating operations since inception. Its core objective is to identify and complete an initial business combination with a private target company within its legally mandated Combination Period [S1][S4][S11]. The SPAC has no sectoral or geographical focus restrictions when selecting suitable targets.

Historical Financial Performance

Financially, SIM Acquisition Corp. I's profile conforms to the typical pre-merger SPAC template: minimal current assets deployed primarily in trust accounts, negative operating income from ongoing administrative costs, and no substantive operating cash flow [F1]. At fiscal year-end December 31, 2025, current assets stood at $270K against current liabilities of $305K, resulting in a current ratio of 0.89 — below the conventional safety threshold indicative of tight short-term liquidity [F1].

The operating loss expanded markedly approximately 75%, from -$575K in 2024 to -$1.01 million in 2025, reflecting increased expenses likely related to ongoing search efforts and administrative overheads involved in identifying merger candidates [F1]. However, net income rose substantially by about 85% year-over-year from ~$4.75 million in 2024 to ~$8.79 million in 2025, suggestive of non-operating gains (possibly interest income from trust funds or other one-time items) that offset operating deficits [F1]. Operating cash flows remain persistently negative (-$632K for FY2025), although improving sequentially by roughly 25%, consistent with the limited revenue model but controlled cash burn in administrative functions [F1].

Equity remains deeply negative at nearly -$10.9 million as of end-2025 due to cumulative operating losses characteristic of entities without established businesses [F1]. This deficit underscores the inherently speculative nature of such vehicles prior to completing their core transformative event.

Financial Summary Table

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 9 | -631658 | -1005841 | +85.2% |

| 2024 | 5 | -843935 | -575708 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -80.8 |

| 2024 | -48.1 |

Source: SEC companyfacts cache [F1].

*Note: Revenue not applicable due to non-operational status; Current assets/liabilities data not disclosed for 2024.

Future Growth Prospects and Strategic Challenges

SIM Acquisition Corp. I’s future hinges entirely on successful identification and execution of an attractive initial business combination before expiration of the Combination Period mandated under its governing documents (commonly around two years from IPO). Failure results in mandatory liquidation and redemption of public shareholder shares at approximately the original offering price [S1][S4][S11][S15].

Key growth drivers are therefore purely dependent on target market dynamics: availability of viable private companies willing to merge via SPAC route; ability to secure financing on acceptable terms including PIPEs or debt instruments; and management’s ability to negotiate favorable transaction terms while managing public shareholder sentiment [S1][S6][S10]. The company has explicitly acknowledged intensified competition from an increasing number of SPACs pursuing similar targets—an environment likely reducing deal flow and raising acquisition prices [S1][S11][S27]. Public shareholders’ redemption rights create further uncertainty by potentially shrinking available capital post-redemption for target funding [S16][S29].

Regulatory scrutiny also poses hurdles—increased compliance costs under Sarbanes-Oxley regulations and possible delays or denials due to foreign investment challenges or governance issues can materially impact timing and viability [S6][S10][S19]. Moreover, founder shares (Class B Ordinary Shares) hold voting leverage over the initial Business Combination approval process which may not align fully with broader public investor interests [S1][S16][S29].

The company has recently entered into an administrative services agreement tied to office space and support arrangements costing roughly $20K monthly and has accepted a $1.5 million promissory note bearing 12% interest from its sponsor intended for working capital needs ahead of completing a business combination [S22][S25], reflecting constrained resources.

Forecasts / Milestones / What To Watch For

While explicit guidance is not provided in available filings, key milestones reside around:

- Completion of an initial business combination prior to July 11, 2026 (or earlier per charter expiration provisions) [S28]

- Publication of definitive proxy materials relating to any proposed business combination subjecting shareholders to voting or redemption choices [N/A]

- Potential amendments extending Combination Period if authorized by shareholders or other instrument holders—subject to increased advisory costs and potential dilution risks [S26][S27]

- Fundraising events (PIPE investments) accompanying any announced merger which impact eventual capital structure post-close.

Market participants should watch for transaction announcements or withdrawal notifications alongside updates regarding litigations or regulatory approvals impacting deal progress.

Capital Allocation & Returns

As common among nascent SPACs without operating businesses, SIM Acquisition Corp. I has no dividend program nor historical stock repurchase initiatives due to lack of free cash flow generation [F1][S13]. Capital allocation centers around managing administrative expenses financed minimally through sponsor loans rather than operational revenue streams.

The equity base reflects cumulative retained losses yielding an approximate negative return on equity calculated around -81% using reported net income relative to equity at December 31, 2025 [F1]. This metric affirms that until a value-creating business combination occurs, shareholder returns are driven by speculation rather than fundamental income metrics.

Sponsor economics derive mainly from founder shares acquired nominally (~$0.004 per share) which could translate into sizable profits upon successful merger completion even if public shares experience downside pressure [S24]. This misalignment constitutes principal risk for public investors who may face dilution alongside restricted voting rights compared to sponsor interests.

Industry Context (Analysis)

The SPAC market has morphed significantly since its peak enthusiasm periods seen several years ago. Enhanced SEC scrutiny on disclosure standards coupled with shifts in investor sentiment have slowed issuance pace considerably—raising barriers for SPAC sponsors needing compelling narratives beyond generic acquisition mandates.

Competition for quality targets has escalated markedly; often necessitating sponsors demonstrate sector expertise or access strategic pipelines otherwise unavailable broadly—a challenge SIM Acquisition Corp I confronts given its non-sector-specific mandate.

Redemption risk—where significant portions of public investors opt out upon announcement—remains acute in today’s market environment characterized by lower valuations and heightened risk aversion relative to boom times.

Regulatory landscape changes especially concerning foreign investment reviews continue weighing on cross-border deal prospects impacting many SPACs with international acquisition ambitions.

Conclusion

SIM Acquisition Corp. I embodies the quintessential zero-history SPAC confronting intensified competition for deals amid financial constraints reflected in modest working capital funded by sponsor loans rather than operational cash flows. Its current financial position reveals tight liquidity parameters compounded by elevated operational loss levels typical pre-combination but highlighting vulnerability if deal execution slips near deadlines.

Stakeholders must monitor upcoming deadlines critically alongside strategic disclosures concerning potential business combinations while cognizant that redemptions coupled with limited shareholder protections may narrow feasible transaction options considerably.

This analysis is based solely on disclosed financial statements and SEC filings up through March 28, 2026. It does not constitute investment advice but aims to elucidate SIM Acquisition Corp. I’s present financial standing, strategic outlook, material risks, and governance nuances reflective of blank check companies preparing for transformative merger events.

Disclaimer: This document is for informational purposes only and does not constitute an offer or solicitation to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments