iAnthus Capital Holdings: Reshaping Its Multi-State Cannabis Footprint Amid Financial Pressures

iAnthus Capital faces ongoing losses and liquidity challenges while refocusing its cannabis operations on key U.S. states through portfolio optimization and debt management.

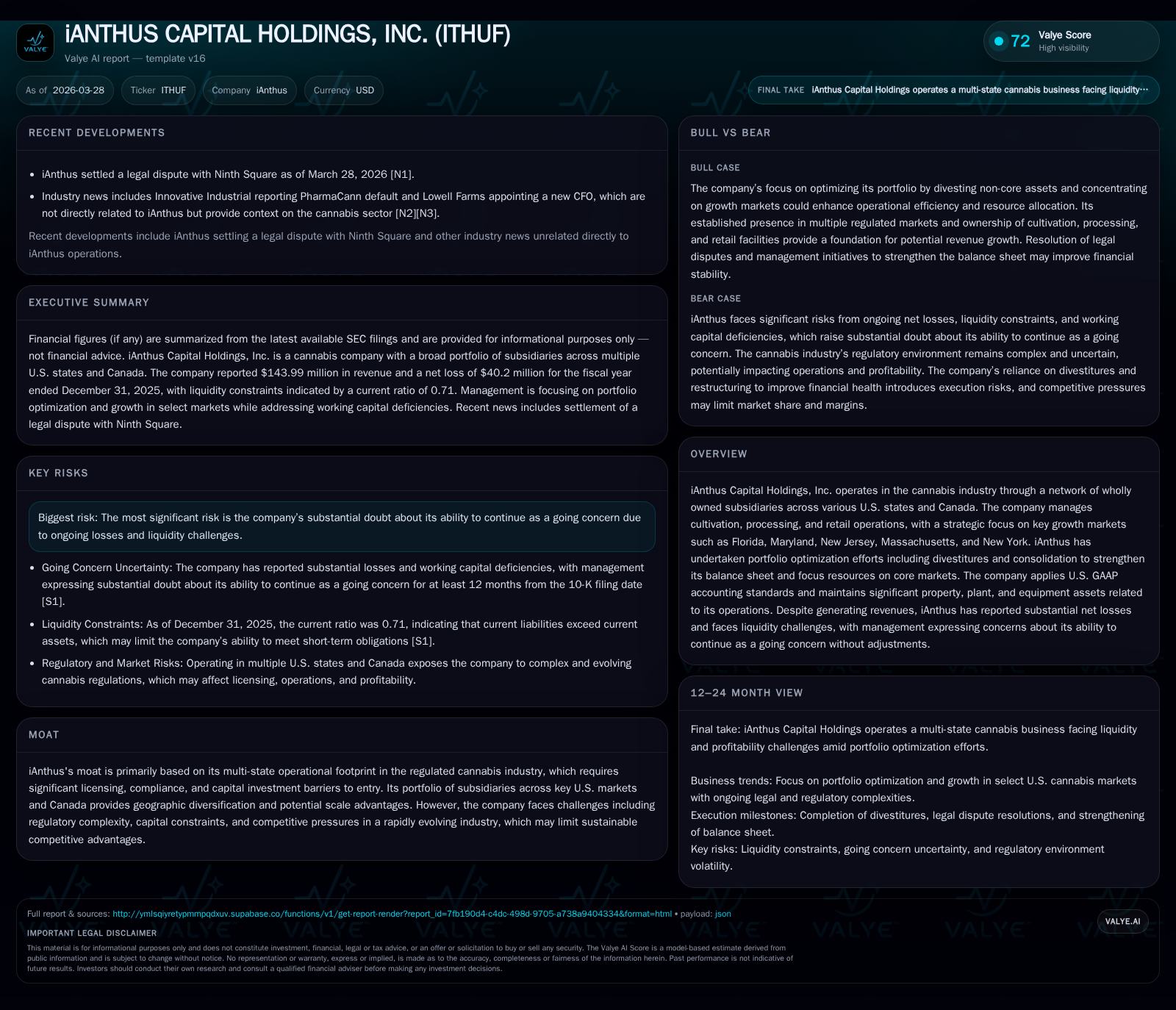

iAnthus Capital Holdings has experienced a revenue decline from $167.6 million in 2024 to $144.0 million in 2025, alongside operating losses nearly doubling year over year. The company is strategically divesting non-core assets and consolidating its footprint primarily within Eastern U.S. markets such as Florida, Maryland, New Jersey, Massachusetts, and New York. Despite modest positive operating cash flow, heavy capital expenditures and substantial debt obligations pose continuing liquidity pressures. Legal settlements and amendments to debt agreements aim to provide some stability, but management continues to express substantial doubt about going concern status.

Historical Trajectory: Revenue Fluctuations and Operating Losses

iAnthus Capital Holdings’ revenue declined from $167.6 million in fiscal year (FY) 2024 to $144.0 million in FY 2025—a contraction of approximately 14.1% [F1]. This aligns with the company’s strategy to optimize its portfolio by focusing on high-growth U.S. states while divesting less profitable or non-core markets [S1]. Operating losses worsened nearly twofold from -$8.5 million in FY 2024 to -$15.4 million in FY 2025 [F1], underscoring ongoing challenges with operational leverage during regulatory complexities and competitive pressures.

Net income losses similarly deepened significantly to -$40.2 million in FY 2025 from -$7.6 million the prior year [F1], reflecting elevated interest expenses and accretion costs tied to the company's complex debt structure.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 144 | -40 | 3 | -15 | -14.1% | -426.5% |

| 2024 | 168 | -8 | 13 | -9 | +5.2% | +90.0% |

| 2023 | 159 | -77 | 3 | -41 | -2.4% | +83.0% |

| 2022 | 163 | -449 | -19 | -112 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -21 | 39.0 |

| 2024 | 7 | 11.7 |

| 2023 | -1 | 124.3 |

| 2022 | -26 | -4089.5 |

Source: SEC companyfacts cache [F1].

Table: iAnthus Annual Financials Overview [F1]

Geographic Segmentation and Portfolio Streamlining

iAnthus operates primarily through two geographic segments: Eastern Region and Western Region [S4][S6]. The Eastern Region—covering Florida, Maryland, Massachusetts, New Jersey, New York, Illinois, and Pennsylvania—generated approximately $133.6 million in revenues during FY 2025, accounting for about 93% of total sales [S4][F1]. The Western Region, including Arizona operations, contracted significantly due to asset divestitures and operational downsizing [S4].

This segmentation reflects management’s focus on markets with greater growth potential while maintaining a limited retail presence in Arizona [S1]. Regulatory frameworks across these states impose distinct compliance requirements affecting cost structures and scalability.

Liquidity Stress and Capital Structure Insights

iAnthus’ liquidity position remains strained, evidenced by a current ratio of 0.71 at December 31, 2025—indicating current liabilities exceed current assets by roughly $19 million [F1]. Despite positive operating cash flow of $3.15 million for FY 2025—a decline from $12.54 million the previous year—the company’s working capital deficiency highlights ongoing cash flow pressures [F1].

Cash flow dynamics are further challenged by inventory carrying costs and valuation risks intrinsic to regulated cannabis operations [S26].

Debt Profile, Covenants, and Related-Party Financing Dynamics

iAnthus carries approximately $193 million of combined secured and unsecured debt as of December 31, 2025, including June Secured Debentures ($132 million), Additional Secured Debentures ($33 million), June Unsecured Debentures ($26 million), plus Senior Secured Bridge Notes ($8.5 million) [S9][F1]. Interest is frequently paid-in-kind (PIK), compounding principal balances over time rather than requiring immediate cash payments [S5][S8][S9].

Several major debenture holders are also significant equity shareholders classified as related parties (e.g., Gotham Green Funds, Senvest entities), adding complexity to governance and financing arrangements [S7][S9]. Debt agreements include restrictive covenants limiting the company's ability to incur additional debt, issue dividends, sell assets without consent, or undertake certain financing activities—factors constraining operational flexibility [S5][S7][S10]. Compliance with these covenants is maintained but remains tight given liquidity constraints.

Operational Cash Flow vs Capital Expenditures: Investment Priorities

iAnthus invested approximately $23.8 million in capital expenditures during FY 2025 compared with operating cash inflows of about $3.15 million—reflecting an aggressive expansion approach focused principally on cultivation capacity and licensing within the Eastern Region [F1][S4][S28]. These capital outlays support compliance with stringent state regulations requiring advanced infrastructure and security measures.

Forward Outlook: Growth Initiatives Amid Financial Challenges

Management intends to allocate proceeds from divestitures into growth-focused Eastern markets like Florida, Maryland, New Jersey, Massachusetts, and New York while concurrently reducing outstanding debt obligations [S1]. Although near-term positive cash flow generation is expected, the company continues to face risks including regulatory complexities, competitive pressures, macroeconomic uncertainties, and lingering litigation exposures [N1][S15][S16].

Milestones & Expectations

iAnthus recently settled a legal dispute with Ninth Square which removes one significant legal overhang [N1]. Management's stated milestones include continued portfolio optimization through divestitures outside core markets alongside targeted reinvestment into strategic states projected for growth potential [S1]. Monitoring progress against liquidity targets aligned with renegotiated debt terms will be essential given disclosed substantial doubt regarding going concern status for at least twelve months forward [S1].

Capital Allocation: Dividend Policy & Shareholder Returns

iAnthus has not declared dividends or repurchased shares amidst ongoing losses and liquidity constraints consistent with prudent preservation of cash resources post recent recapitalizations [F1][S18][S19]. Equity remains deeply negative at approximately -$103 million as of December 31, 2025 resulting in an approximate negative return on equity near -39%, reflecting historical accumulated deficits without sustainable profitability under present conditions [F1]. Capital deployment prioritizes organic growth investments balanced against debt servicing rather than shareholder distributions.

This analysis synthesizes publicly available SEC filings alongside news disclosures up to March 28, 2026 without speculation beyond cited facts or direct management commentary sources provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments