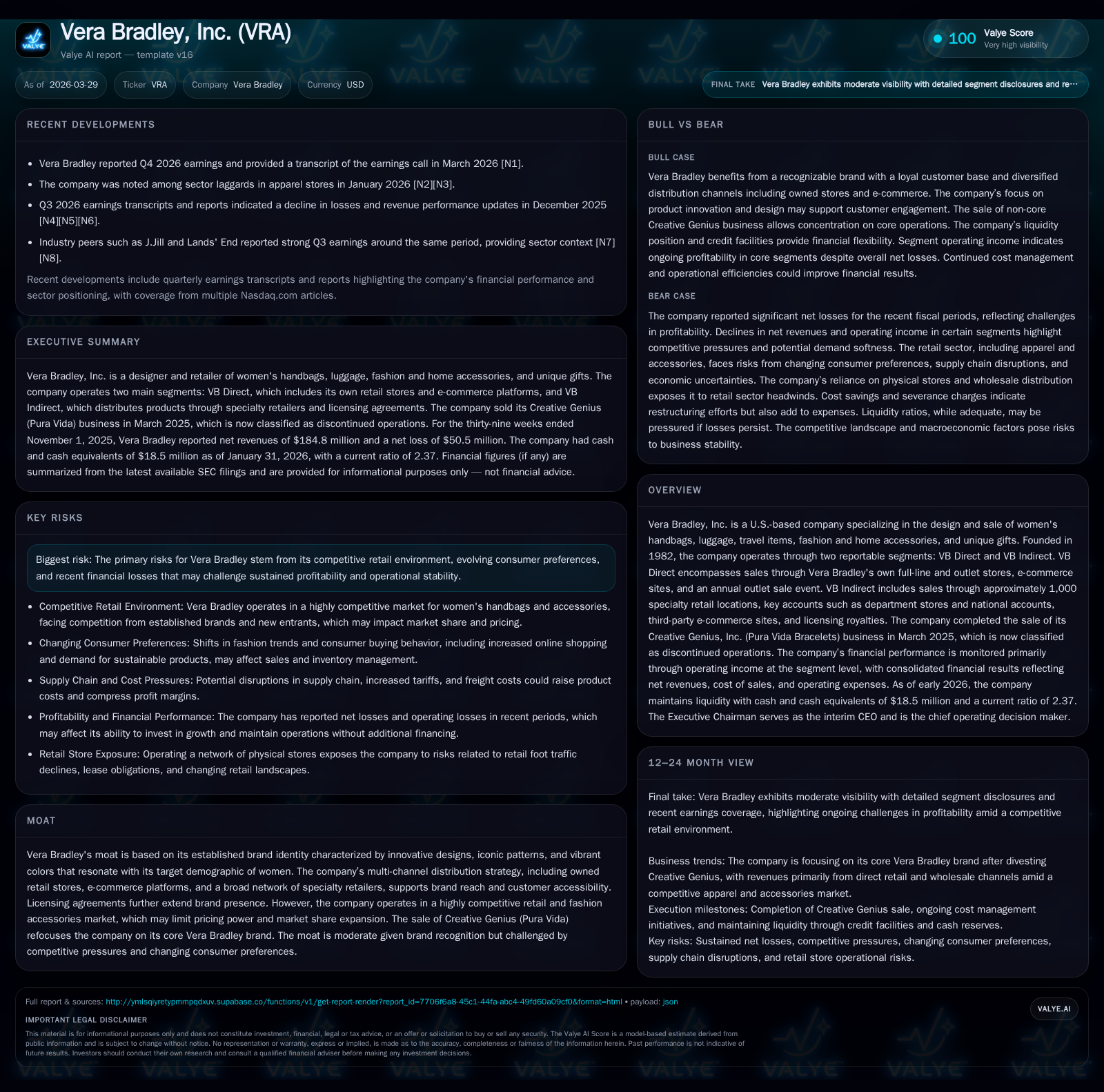

Vera Bradley Rebounds with Brand Focus Despite Operating Losses and Tight Margins

Following the divestiture of Pura Vida, Vera Bradley concentrates on core brand revitalization amidst operational challenges.

Vera Bradley, Inc., a women's accessories designer, exited its Pura Vida business in early 2025 to focus on its namesake brand marketed through two segments: VB Direct and VB Indirect. The company reported significant revenue contraction versus prior peaks and mounting operating losses extending into fiscal 2026, despite a modest net income turnaround due primarily to discontinued operations effects. Its capital structure remains manageable, supported by liquidity from $18.5 million cash and a substantial revolving credit facility, though cash flow remains negative. Cost-saving initiatives and store rationalizations are efforts underway as the company navigates a competitive retail landscape and evolving consumer preferences.

Company Overview

Vera Bradley, Inc. operates as a designer and marketer of women's handbags, luggage, travel items, fashion and home accessories, as well as unique gifts. Founded in 1982, it has evolved its distribution into two main segments: VB Direct—which includes own full-line stores, outlet stores, e-commerce platforms, and an annual outlet event; and VB Indirect—comprising approximately 1,000 specialty retail locations across the U.S., department stores, national accounts, third-party e-commerce sites, and licensing royalties. The company’s strategic pivot was marked by the March 2025 divestiture of Creative Genius (Pura Vida Bracelets), categorizing that business as discontinued operations henceforth [S1][S20].

Historical Growth & Performance

Historically, Vera Bradley experienced significant top-line fluctuations. Revenues peaked around $154.1 million in fiscal year 2016 before notable downtrends followed by volatility—with FY2019 revenue recorded at about $118.2 million [F1]. The most recent annual figures available show continuing operational stress: FY2026 revenue details for continuing operations were not explicitly disclosed post-divestiture but segmental breakdown indicates shrinking net revenues with notable pressure on both direct channel sales and indirect distribution [S7][S13][F1].

Operating income has mirrored this pressure closely. From a positive operating income of roughly $10.4 million in FY2024 to consecutive losses exceeding $42 million in FY2025 and narrowing to approximately $31.9 million loss in FY2026 illustrates the steep challenges the company faces to restore profitability [F1]. Despite these operating setbacks, net income turned slightly positive in FY2026 to $2.7 million from a sizable loss of nearly $62.2 million the prior year—a recovery largely attributed to discontinued operation gains post-Pura Vida sale alongside tax effects rather than core operating improvements [F1].

Cash flow generation remains weak. Operating cash flow was negative near $14.1 million in FY2025 improving marginally to about minus $10 million in FY2026 amid continuing capital investments totaling about $3.3 million for fiscal year ending January 31, 2026 [F1]. This resulted in free cash flow deficits exceeding $13 million recently.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 3 | -10 | -32 | 3 | +104.3% |

| 2025 | -62 | -14 | -42 | 10 | -893.4% |

| 2024 | 8 | 48 | 10 | 4 | +113.1% |

| 2023 | -60 | -13 | -95 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 0 | -13 | 2.0 |

| 2025 | 22 | -24 | -34.8 |

| 2024 | 2 | 44 | 3.0 |

| 2023 | 18 | -22 | -23.8 |

Source: SEC companyfacts cache [F1].

Table: Select annual financial performance highlights (amounts approximate).

Future Growth Prospects & Challenges

The company seeks growth through revitalization of its core Vera Bradley brand post-Pura Vida exit by doubling down on distinctive product designs characterized by vibrant patterns appealing mainly to women customers [N1][S20]. Multi-channel distribution remains central with a blend of owned stores (31 full-line & 86 outlets at latest count), direct e-commerce efforts including international web presence, complemented by broad wholesale relationships covering specialty retailers and department stores across the U.S.[S7][S20].

However, growth is capped by intense competition within the retail fashion accessories market—a space marked by numerous brands vying for customer attention alongside fast-evolving demand patterns influenced by pandemic recovery dynamics and digital retail shifts [N1][S14]. Pricing power is limited given customer sensitivity and availability of substitutes.

Additionally, supply chain disruptions, freight cost inflation related to tariffs or logistics complexities pose margin pressure risks [S14][N1]. Vera Bradley itself reports ongoing cost-saving initiatives spanning store efficiencies, marketing spend moderation, IT contract negotiations, logistics optimizations, as well as corporate payroll rationalizations—some initiated pre-2025 but accelerated more recently—to preserve margin discipline [S9][S22]. The transition also involves store footprint adjustments given some impairment charges recognized over recent periods linked to underperforming physical locations [S25].

Forecasts & Milestones

Explicit forward guidance or milestone disclosures have not been provided beyond strategic commitments documented in SEC filings and recent earnings commentary [N1][S3][S11]. Key indicators to monitor include:

- Segment revenue turnaround particularly within VB Direct e-commerce growth trajectory,

- Stabilization or reduction of operating losses,

- Progress on cost reduction programs delivering sustainable SG&A savings,

- Inventory management effectiveness given historical markdown risks.

Management changes noted with appointment of Ian Bickley as CEO since June 2025 indicate leadership focus sharpened on executing transformation plans under tighter operating discipline [N1][S3].

Returns & Capital Allocation

Return metrics remain subdued with an approximate return on equity of around 2% based on the latest net income relative to shareholder equity counts near $131.6 million at end-FY26 [F1]. Capital allocation during the last few years includes share repurchase activities amounting to over $21 million in FY25 but no buybacks executed yet within FY26 despite authorization for up to $30 million under the current plan established late calendar year 2024 [S8][S28][F1]. Dividends have not been referenced indicating a likely focus on deleveraging and liquidity preservation.

Liquidity remains supportive with cash balances around $18.5 million complemented by an asset-based revolving credit facility providing up to $75 million capacity ($65 million available at end-FY25) secured primarily against assets including inventory and receivables with maturity set for May 2028 [S4][S12][F1]. Debt covenants such as minimum fixed charge coverage ratios apply but currently compliance appears intact with borrowings modest at approximately $10 million as of late calendar year 2025 filings [S4][S12][F1].

Industry Context (Analysis)

Retail apparel and accessories brands face an accelerating shift toward omnichannel experiences compounded with economic headwinds impacting discretionary spending patterns since global macro uncertainties persist . Consumer palettes are increasingly driven by convenience factors like direct online access while valuing brand authenticity amid sustainability considerations.

Within this environment, Vera Bradley’s ability to leverage its iconic colorful pattern designs remains valuable but must be continually refreshed alongside sharp execution of inventory controls to avoid markdown erosion—a common pitfall evident among mid-tier brands struggling with merchandise glut or obsolescence issues during rapid trend resets.

Conclusion

Vera Bradley is navigating a complex reset phase following strategic narrowing on its core brand after shedding non-core assets like Pura Vida Bracelets. Despite healthy brand recognition rooted in unique aesthetics targeting female consumers across multi-channel formats, the company endures operational losses though somewhat moderated compared to sharp deterioration seen prior years. Continued investment discipline via cost savings is enabling a leaner structure even if free cash flow generation stays negative amid modest capex plans. Maintaining liquidity flexibility combined with effective multi-pronged growth initiatives will be critical levers moving forward amid pronounced competition and shifting consumer demand trends.

This report is intended for informational purposes only and does not constitute investment advice or a recommendation regarding any security or strategy.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments