BayFirst Financial Corp: Local Banking with Sharpened Focus and Capital Challenges

BayFirst has retreated to its Florida community banking roots amid financial strains and portfolio restructuring.

BayFirst Financial Corp has deepened its commitment to community banking within the Tampa Bay/Sarasota area after exiting nationwide SBA 7(a) and residential mortgage lending businesses. Despite steady operating cash flows, the company faced a sharp net income decline in 2025, posting a $22.9 million loss primarily due to restructuring and credit costs. Capital adequacy remains a focus, with the bank maintaining regulatory well-capitalized status but confronting liquidity management challenges amid increased time deposits and subordinated debt adjustments. Operational cost controls and focused lending strategies toward healthcare and minority-owned business segments define its near-term priorities.

Earnings Erosion Despite Community Banking Strength

BayFirst’s financial performance in the fiscal year ending December 31, 2025 shows significant deterioration relative to prior years, driven primarily by operational restructures and increased credit loss provisions linked to strategic shifts. The company reported a net loss of $22.9 million compared to net income of $12.6 million in FY2024—a nearly 282% year-over-year decline [F1]. Despite this, operating cash flow remained strong at approximately $285 million, down about 27% from prior year levels reflecting curtailed loan sales and discontinuation of nationwide SBA and mortgage lending activities [F1][S1].

This divergence between cash generation and profitability highlights BayFirst's reliance on consistent interest margin from community loans alongside provisioning policies during portfolio transitions. The bank serves consumers, small-to-medium businesses, and professionals primarily within Florida’s Tampa Bay/Sarasota region through personalized community banking channels offering deposit accounts, consumer loans, commercial loans, real estate loans, and lending programs focused on healthcare entities and minority businesses [S1].

BayFirst Financial Corp Historical Financial Snapshot (FY2022-FY2025)

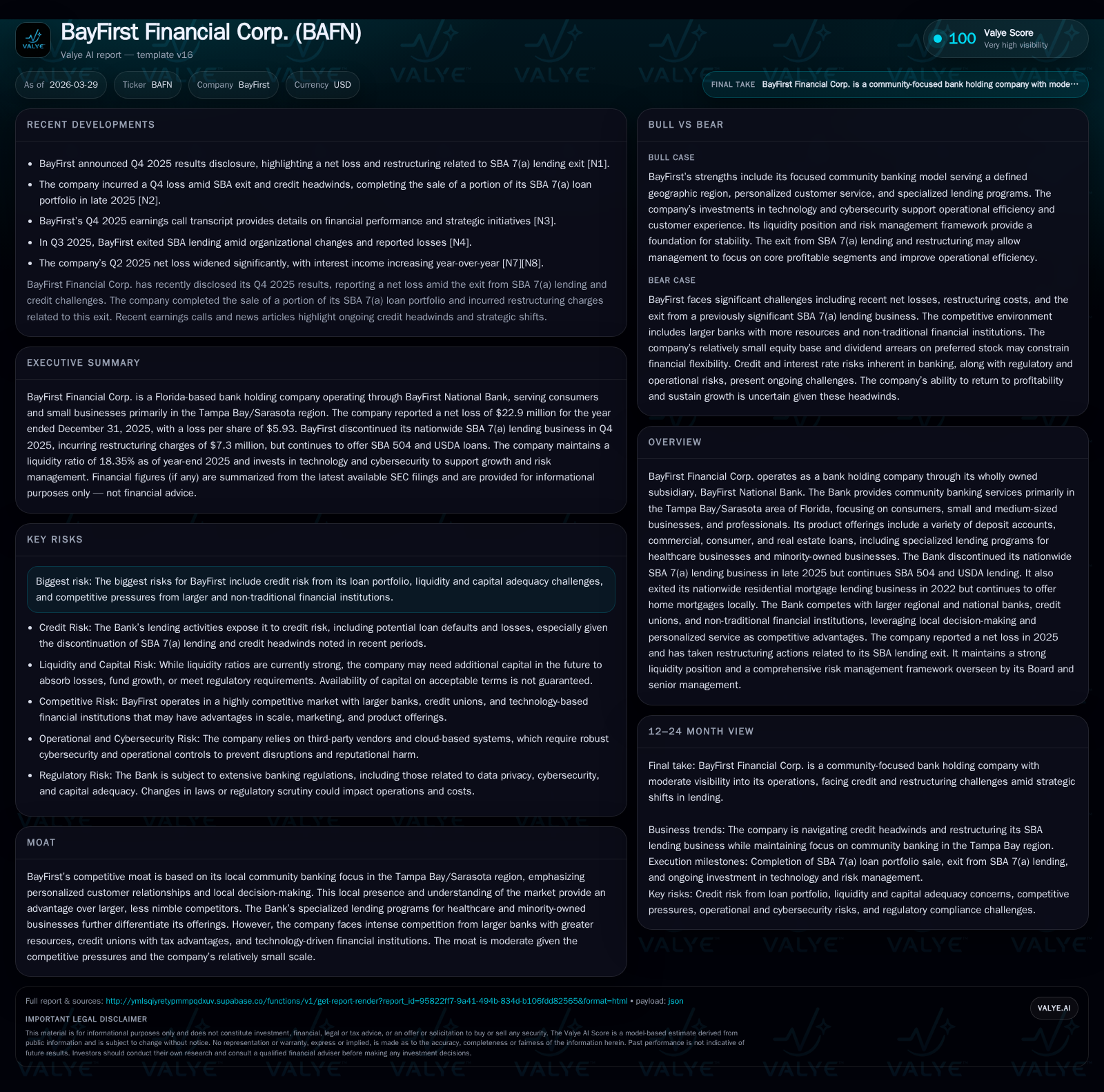

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -23 | 285 | 0 | -282.0% |

| 2024 | 13 | 391 | 2 | +121.0% |

| 2023 | 6 | 455 | 8 | +1733.8% |

| 2022 | 0 | 440 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 663000 | 335000 | 285 |

| 2024 | 1323000 | 0 | 389 |

| 2023 | 1313000 | 13000 | 447 |

| 2022 | 1287000 | 49000 | 432 |

Source: SEC companyfacts cache [F1].

Table: Multi-year trends illustrate volatile bottom-line performance contrasted with robust operational cash flows and sharply reduced capital expenditures.

Historical Growth and Lending Portfolio Evolution

BayFirst historically grew through targeted origination of traditional community banking loans and government-backed programs such as SBA and USDA loans nationwide [S1]. Strategic shifts led to discontinuing SBA 7(a) lending nationally in Q3 FY2025 while retaining SBA CDC/504 loans; it exited nationwide residential mortgage lending after FY2022 [N1][S1]. These moves aim to reduce operational complexity and concentrate efforts on the Tampa Bay/Sarasota region.

Loan portfolio composition includes government guaranteed loans ($54 million), commercial real estate, consumer loans including auto financing, home equity products, as well as specialized healthcare provider lending programs [S6][S19]. No single industry exceeds regulatory concentration thresholds (10%), reflecting deliberate diversification [S6]. However, nonperforming assets rose from about $19 million in FY2024 to over $26.5 million by end-2025, increasing credit risk exposure despite an allowance for credit losses of approximately $671 thousand covering off-balance sheet exposures alone [S21][S12].

Refocusing on Tampa Bay/Sarasota: Strategic Retrenchment

The company operates out of its main office plus eleven additional centers across Pinellas, Hillsborough, Sarasota, Manatee, and Pasco counties—the core Tampa Bay/Sarasota market area [S1][N1]. BayFirst emphasizes local decision-making with products tailored for consumers rebuilding banking access (e.g., "Essential Checking") and business accounts targeting minority-owned enterprises seeking growth capital [S19].

While this localized approach fosters customer loyalty relative to larger banks’ standardized offerings, it also exposes BayFirst to competitive pressures from fintech lenders and credit unions within these markets alongside regulatory complexities that challenge scale advantages enjoyed by larger institutions [S1].

Capital Position and Liquidity: Navigating Heightened Strains

BayFirst's liquidity ratio improved markedly to about 18.35% at December-end FY2025 from roughly 9.17% the prior year—reflecting deliberate increases in liquid assets including cash approximating $207 million per SEC filings corroborated by XBRL data [F1][S4]. However, this higher liquidity exists alongside rising contractual obligations totaling over $431 million spanning operating leases, long-term borrowings including subordinated notes ($6 million principal), and time deposits which increased more than $92 million year-over-year [S4][S12][F1].

Subordinated Notes mature June-2031 with an amendment deferring interest payments through June-30, 2026; these carry fixed then floating rates tied to SOFR plus a spread—potentially affecting refinancing flexibility if market conditions worsen [S7][S18]. Regulatory capital ratios position BayFirst above "well-capitalized" thresholds under Basel III standards; total capital ratio is around ~10%, Tier-1 capital exceeds minimums near ~8%, common equity Tier-1 near ~8.9% [S17][S23]. Shareholders’ equity declined from $110.9M in FY24 to $87.6M in FY25 due largely to losses but remains supportive of ongoing operations [F1][S23].

Operational Adjustments and Cost Management in Early CY26

Cost containment accelerated with elimination of Chief Accounting Officer role as part of workforce reductions reported February 13, indicating overhead tightening amid earnings pressure [S3]. Capital expenditures dropped significantly by about ~82% year-over-year from $1.69M in FY24 down to just $300k in FY25—consistent with retrenchment strategy focusing on liquidity preservation over expansion investments [F1].

Dividends, Buybacks, and Shareholder Returns Amid Pressure

Capital return has been curtailed: dividends paid declined roughly by half—from about $1.3M annually pre-FY25 down to ~$663k for FY25 [F1]. Stock repurchases were minimal ($335k) before the repurchase program was terminated effective October-quarter end of FY25 per board action [N1][F1], reflecting prioritization of liquidity over shareholder distributions.

Credit Risk and Competitive Pressures

Credit risk remains a critical concern given growing nonperforming assets now representing approximately ~2.68% of total loans held for investment excluding government guaranteed loans—a rise signaling some asset quality stress amid transitions [S21]. Conservative underwriting policies govern loan approvals emphasizing borrower financial strength, collateral evaluation, diversification strategies across loan types including real estate collateral guidelines and governmental loan program standards for SBA/USDA products [S13][S14].

Competition arises from larger Florida-based banks leveraging technology scale advantages alongside tax-favored credit unions competing on pricing within key deposit segments—imposing pressure on BayFirst’s market share within its regional footprint [S1][N1]. Regulatory compliance demands add further operational complexity for smaller regional banks.

Key Milestones Impacting Outlook

Upcoming milestones include progression of SBA loan portfolio sale transactions contingent on SBA approval processes; any delays or failures could materially affect liquidity or earnings projections [N1][S2]. Maintaining or improving regulatory capital ratios despite earnings volatility will be essential for future growth options or potential expansion initiatives.

Monitoring stabilization or reduction of nonperforming asset levels will provide insight into effectiveness of credit risk management through this transition phase.

Disclaimer: This analysis is based solely on publicly available disclosures as of early 2026 regarding BayFirst Financial Corp’s financial condition and strategic developments; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments