AEI Income & Growth Fund XXII’s Financial Turnaround and Unit Repurchase Strategy

AEI Income & Growth Fund XXII Ltd Partnership reversed prior operating losses through rental income growth and disciplined unit buybacks, enhancing distributions and liquidity.

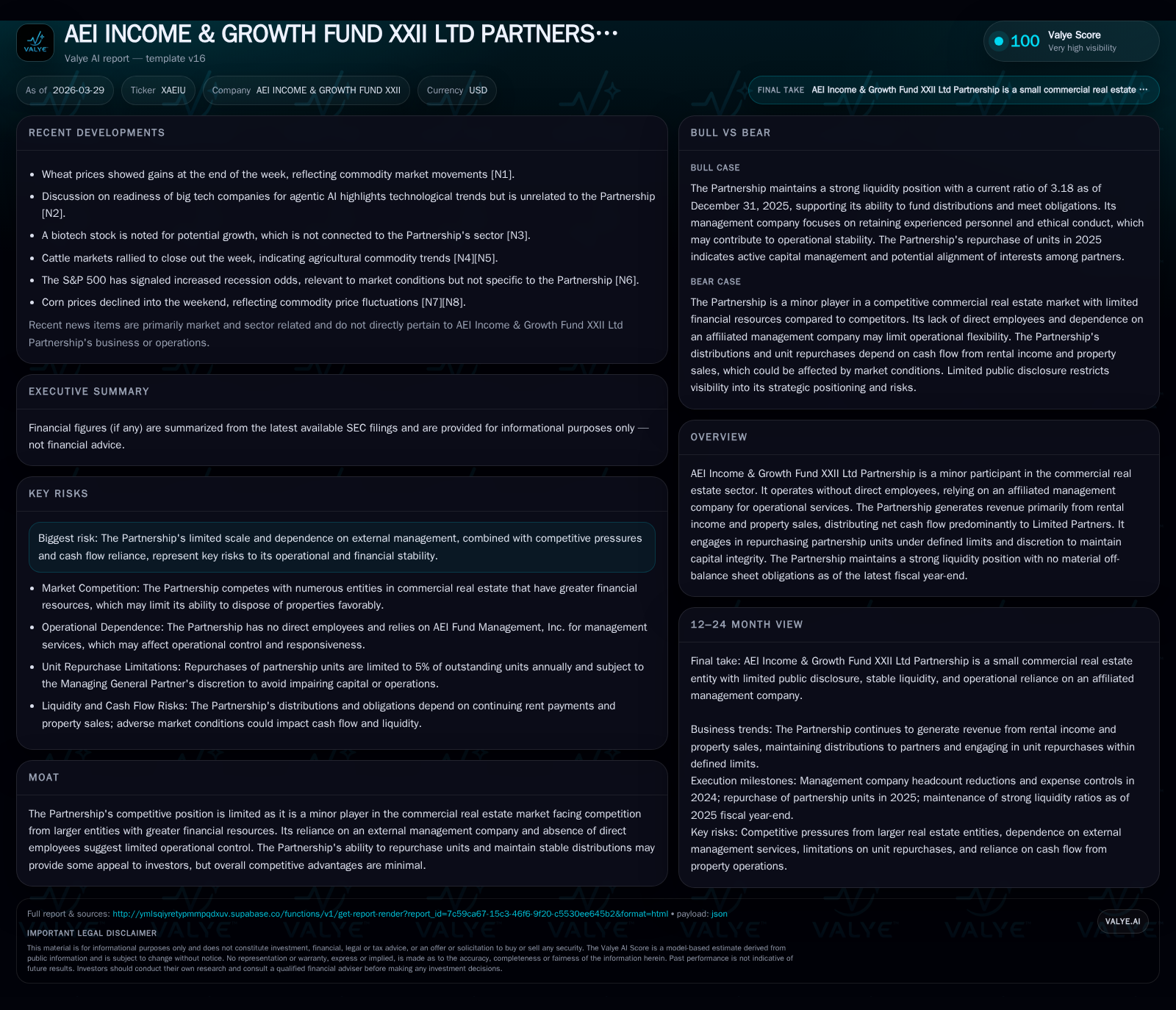

AEI Income & Growth Fund XXII has undergone a marked financial recovery after several years of fluctuating earnings. The partnership shifted from a loss-making position in 2024 to modest operating profitability in 2025, driven by stabilized rental income and gains from property sales. Strategic repurchases of partnership units, conducted within established limits, have increased ownership concentration for remaining partners while supporting consistent distribution growth. Liquidity remains robust, supported by strong cash balances and absence of off-balance sheet liabilities. However, AEI remains a minor player with limited competitive advantages due to scale and reliance on external management.

Financial Performance Evolution: A Shift from Losses to Gains

AEI Income & Growth Fund XXII’s recent financial reports reveal a significant turnaround following years of volatile operational results. Over fiscal years 2022 through 2025, revenue contracted slightly from $547K in 2023 to $417K in 2025—a decline of approximately 5.2% last year [F1]. Notably, operating income rebounded sharply from a negative $22.2K in 2024 to a positive $22.4K in 2025, representing over 200% improvement year-over-year [F1]. This swing reflects controlled operating expenses coupled with steady rental inflows.

More striking is the surge in net income, which rose from $16.5K in 2024 to $241.7K in 2025—an increase greater than twelvefold or +1363% YoY [F1]. This spike stems largely from recognized gains on property sales alongside ongoing rental revenues and prudent expense management detailed in MD&A disclosures [S1]. Simultaneously, operating cash flow showed moderate growth from $291K to $306K supporting liquidity resilience [F1].

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 417382 | 241738 | 306492 | 22419 | -5.2% | +1363.2% |

| 2024 | 440126 | 16521 | 291413 | -22240 | -19.5% | -68.1% |

| 2023 | 547015 | 51795 | 438994 | 46154 | +25.9% | -91.3% |

| 2022 | 434359 | 598495 | 469099 | 66119 |

Source: SEC companyfacts cache [F1].

This table underscores the dramatic shift from prior losses to net profitability anchored by solid rental performance and strategic sales.

Growth Drivers in Rental Income and Property Sales

The Partnership's revenue streams are anchored primarily in tenant rents supplemented by periodic property dispositions [S1,S2,S4]. While there were no recent acquisitions reported during quarterly periods ending March or September of 2025 [S4], proceeds from a notable property sale yielded approximately $925K gross cash with a net gain near $204K recognized mid-2025 [S18]. These funds bolstered working capital and provided liquidity for distributions and unit repurchases.

Rental income benefits from consistent rent payment timing across the portfolio; however, overall revenue was slightly down due to natural lease expirations or market conditions restricting increases [S1]. The absence of direct employees means day-to-day management relies entirely on AEI Fund Management Inc., which reduced staff headcount in prior year driving expense efficiencies but limiting operational control [S1,S14]. This structure inherently constrains scale benefits typically realized by larger real estate owners but keeps fixed costs manageable.

Unit Repurchases: Amplifying Limited Partners’ Stake

A key element contributing to shareholder value enhancement is the Partnership's disciplined unit repurchase program capped at purchasing no more than five percent of total outstanding units per calendar year [S1,S2,S6,S7,S10]. During calendar year 2025 alone, AEI repurchased over 720 units at aggregate cost just under $381K sourced from net property sale proceeds [S7]. These purchases originated from Limited Partners tendering units back to the Partnership often at discounted prices.

Unit buybacks serve multiple strategic purposes: reducing outstanding equity dilutes tax burdens per remaining partner and concentrates ownership stakes among dedicated investors; simultaneously enabling General Partners to derive incremental distributions tied proportionally to these repurchases totaling approximately $3.8K for GP holders last year [S7]. Prior years showed no similar buyback activity illustrating a new emphasis on recapturing equity internally rather than dilution via external sales [S7,S10].

This unit repurchase approach aligns governance incentives closely between General Partner managers and Limited Partners receptive to stable distribution incomes while maintaining balance sheet integrity.

Distributions: Consistency Despite Market Challenges

AEI maintained—and markedly expanded—distribution payouts throughout this recent turnaround phase. Total declared distributions soared from roughly $277K in fiscal year 2024 to about $1.28M in fiscal year 2025—a near fivefold increase consistent with enhanced cash flows available [S1,S7]. Following agreement terms allocations assign approximately 97% of Net Cash Flow distributions to Limited Partners versus a residual share of about three percent directed toward General Partners [S1,S7].

Such payout alignment retains investor confidence given the commitment to distribute operation-generated cash predominantly without reliance on external financing or asset liquidation beyond scheduled property sales [S7]. Quarterly distribution declarations are made prior to quarter-end with payments promptly following each quarter signaling maturity in cash flow allocation policies despite macroeconomic real estate uncertainties [S4].

Liquidity Management and Balance Sheet Strength

The Partnership reported over $470K held in cash and equivalents as of year-end December 31, 2025 supported by current assets mirroring this balance creating a healthy current ratio of approximately 3.18 that comfortably exceeds liquidity thresholds needed for ongoing obligations [F1,S3,S7]. Notably absent are material off-balance-sheet commitments or other contingent liabilities that could impair flexibility—a reassuring factor amidst broader sector volatility [S1,S3,S7].

Robust liquidity affords AEI flexibility when executing unit repurchase programs without compromising distribution commitments or operational budgets—a critical advantage given its small size relative to institutional peers.

Constraints and Competitive Position in Commercial Real Estate

AEI occupies an inherently constrained competitive niche as a minor participant within commercial real estate markets dominated by far larger entities wielding substantial financial capital and operational scale advantages [S1,S14]. Its total asset base pales compared to regional REITs or private equity platforms active with significant acquisition momentum.

Operationally reliant on an affiliated management company staffed with reduced headcount post-2024 implies limited direct control or responsiveness regarding property management or market repositioning efforts; this restricts proactive portfolio optimization potential typical among more vertically integrated landlords or developers [S1,S14]. Thus its moat is minimal—largely tethered to strategic buyback policies sustaining partner returns rather than appreciation potential derived from aggressive asset rotation or expansion.

Ongoing Risks Linked to Scale and Management Structure

Several underpinning risks stem directly from AEI’s structural characteristics: lack of employees raises dependency risk on one management firm; small scale amplifies exposure to market dislocations; constrained liquidity sources mean disruptions to rental roll or asset liquidation timing could sharply strain distribution sustainability [S1,S5].

While formal risk factor disclosures are limited given smaller reporting company status [S9], it remains critical investors appreciate sensitivity around net asset value fluctuations triggered by property market pricing shifts as well as counterparty credit quality affecting rent collections.

Future Outlook: What Investors Should Monitor

Absent explicit forward guidance or public milestone targets within filings or news notes [N#], focus should fall on observable metrics that inform ongoing financial health: cadence of agreed-upon unit repurchase exercises up to permitted caps provides signal on partner confidence levels; trends in tenant rent rolls especially if impacted by emerging economic headwinds referenced broadly across markets should be monitored for revenue continuity; any material changes in quarterly distribution declarations would indicate shifts either toward conservatism or optimism regarding sustainable free cash flow generation.

Analysis suggests macroeconomic uncertainties heighten real estate sector caution broadly including recession risks flagged externally this year potentially influencing tenant demand and capital access pathways that could echo into AEI’s small-scale model [N7]. Keeping tabs on management commentary around these variables will be crucial.

Disclaimer: This analysis is prepared solely for informational purposes using data extracted directly from filed regulatory documents ([F1],[S#]) and publicly available news ([N#]). It does not constitute investment advice or recommendations regarding any securities referenced herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments