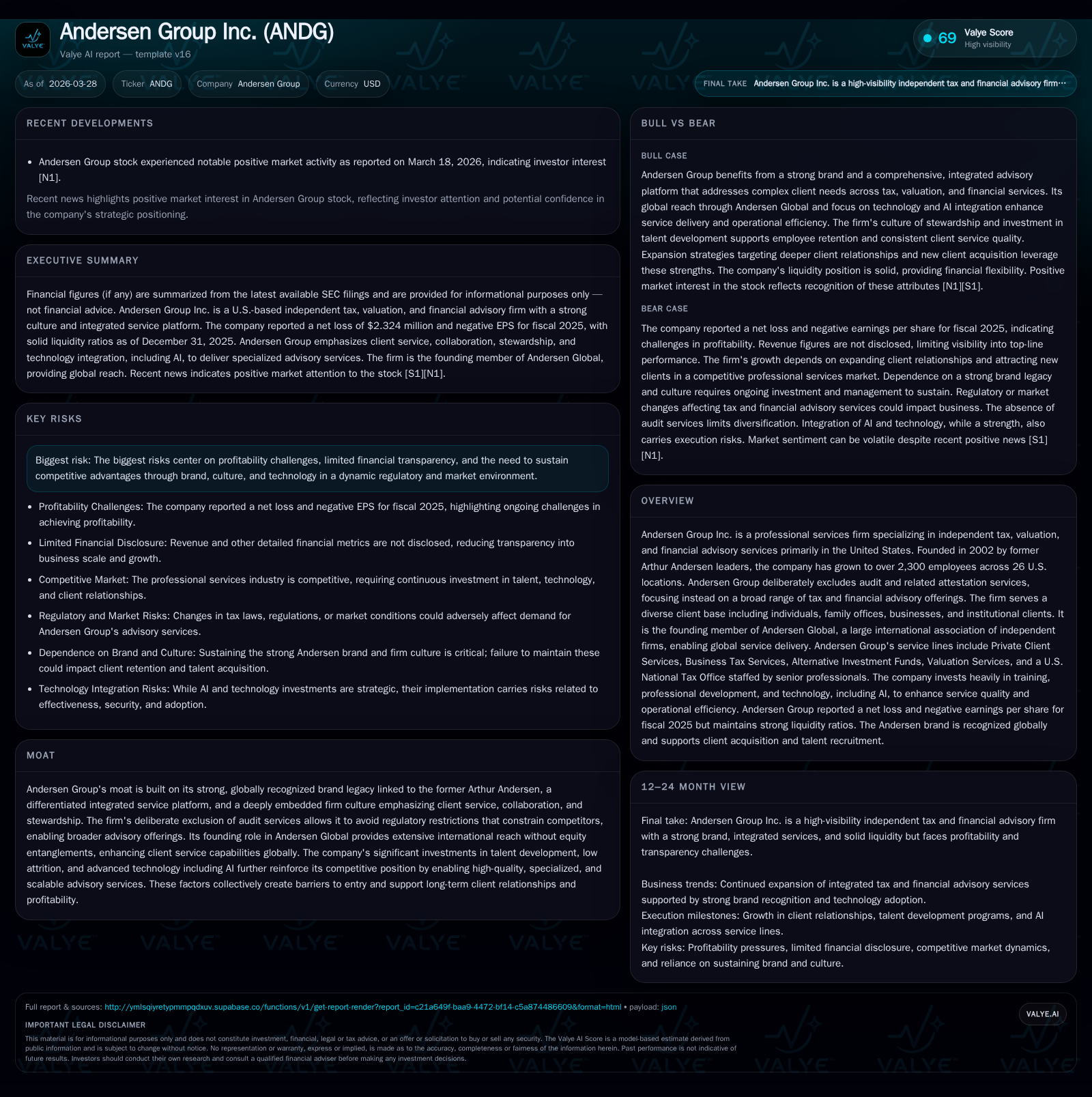

Andersen Group Inc.: Brand Legacy Fuels Tax and Advisory Services

Leveraging the Arthur Andersen heritage and focused advisory platform, Andersen Group pursues growth through integrated service lines and global expansion.

Founded by former Arthur Andersen leaders in 2002, Andersen Group Inc. has cultivated a distinct identity in tax, valuation, and financial advisory services while deliberately excluding audit offerings. The firm’s strong brand legacy supports broad client relationships and underpins its rapid growth to over 2,300 employees across 26 U.S. locations. Despite solid revenue expansion driven by specialized service lines and global affiliations via Andersen Global, profitability remains challenged with operating losses reported in the latest fiscal year. Looking ahead, Andersen aims to deepen its integrated services, extend international footprint through acquisitions, and harness technology advancements amid intensifying competition and regulatory complexity.

Legacy and Evolution: From Arthur Andersen Roots to Independent Success

Founded in 2002 by former leaders of Arthur Andersen, Andersen Group Inc. engineered a deliberate departure from its predecessor by wholly excluding audit and related attestation services. This exclusion sidesteps the strict regulatory constraints that bind traditional accounting firms and permits greater flexibility to offer multidimensional tax and financial advisory services. The firm's foundational culture emphasizes client service excellence, collaboration among multidisciplinary teams, and stewardship — values inherited yet refined post-Arthur Andersen collapse. This cultural fabric and globally recognized name afford it a moat difficult for market entrants to replicate.

Recent Fiscal Performance: Growth Patterns and Profitability Challenges

Between fiscal years ending December 31, 2024 and 2025, Andersen Group expanded revenue from approximately $731.6 million to $838.7 million — a strong increase reflecting both organic growth and strategic expansions [F1]. However, operating income swung into loss territory at negative $135.3 million for 2025 compared with prior profitability ([F1]). Net income approached breakeven at -$2.3 million as restructuring costs including issuance of new profits interest units weighed heavily ([F1]). The firm nevertheless maintained strong liquidity with cash & equivalents at $250.3 million and a current ratio of 2.1x providing operational stability ([F1]). Cash flow from operations less capital expenditures produced free cash flow near $174 million underscoring effective working capital management despite earnings pressures.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Fiscal 2025 operating income reflects restructuring charges impacting comparability.

Service Lines Powering Client Relationships and Market Reach

Andersen's differentiated business model comprises five core service lines tailored to complex client demands:

- Private Client Services: Comprehensive wealth management including multigenerational estate planning, charitable giving strategies, and trust administration.

- Business Tax Services: Scalable tax consulting and compliance offerings addressing corporate planning and regulatory reporting obligations.

- Alternative Investment Funds: Specialized advisory for hedge funds, private equity vehicles, family offices, venture capital funds, REITs focusing on intricate tax implications.

- Valuation Services: Independent valuations critical for tax compliance, financial reporting mandates, and regulatory adherence.

- U.S. National Tax Office: Senior professionals delivering national-level tax strategy support.

This constellation of offerings leverages specialized technical expertise combined with practical advice delivered typically through direct senior Managing Director involvement ([S12][S16]). Their multidisciplinary approach integrates backgrounds in law, economics, accountancy, and consulting — crucial for tackling nuanced tax challenges shaping deep recurring engagements.

Global Footprint Driven by Andersen Global and Cross-Border Synergies

While Andersen Group’s operations remain U.S.-centric with 26 domestic offices housing over 2,300 employees ([S9]), their membership in Andersen Global extends access to an expansive international network exceeding 300 independent member firms across more than 180 countries ([S9]). This network effect fosters collaborative cross-border partnerships without incurring equity losses or the baggage of audit compliance hurdles common among Big Four competitors ([S6]). It allows seamless multinational servicing for clients facing increasingly globalized tax landscapes.

Growth Outlook: Opportunities Amid Regulatory and Competitive Headwinds

Strategically poised for international expansion via acquisition agreements pending closure in Q2 2026 across Africa, Latin America, and Canada ([S19]), Andersen targets augmenting its geographic diversity alongside its historically robust U.S. base ([N1]). Concurrently, it plans to broaden consulting services leveraging the revered Andersen Consulting brand asset ([S13]). This dual approach intends to capture new markets while deepening existing client relationships through enhanced service scope.

Nonetheless numerous headwinds endure: escalated regulatory compliance pressures particularly regarding privacy laws (e.g., CCPA/GDPR) and anti-bribery statutes (e.g., FCPA) demand sustained resource allocation ([S7],[S21]); burgeoning adoption of AI technologies introduces competitive disruption risks contingent on timely deployment and staff adaptation ([S18],[S26]); litigation exposure linked to errors or omissions necessitates vigilant risk management despite current insurance coverage ([S4],[S5],[S8]); talent retention remains vital given industry-wide competition for qualified professionals ([S6],[S7]). These factors impose constraints that could temper margin recovery despite revenue growth ambitions.

Capital Allocation Review: Balancing Investment, Cash Flow, and Returns

The company exhibits prudent capital discipline characterized by strong free cash flow generation (~$174 million) underpinned by operational cash collections exceeding capital expenditures ([F1]). Cash reserves near $250 million bolster balance sheet flexibility ([F1]), enabling continued investments in talent development, technology enhancements including AI tools adoption programs ([N1]), as well as funding selective acquisitions consistent with strategic expansion goals ([S15],[S28]).

Persistent net losses contribute to modest return on equity estimated at roughly 1.7%, illustrating profitability constraints tied partly to restructuring expenses incurred during growth phases ([F1]). No current dividend distributions are declared; instead retained earnings appear prioritized toward reinvestment initiatives supporting medium-term scalability.

Risks on the Horizon: Litigation, Talent Retention, and Technological Disruption

The professional services domain inherently encompasses risk exposures stemming from potential claims related to errors or omissions spanning intellectual property disputes to data privacy breaches ([S4],[S5]). Although no material adverse outcomes are presently anticipated from ongoing legal proceedings ([S4]), defense costs as well as management distraction pose tangible threats.

Employee turnover risk is mitigated somewhat by strong firm culture but remains a focal point given dependence on skilled professionals whose exit could impair client delivery capability ([S6],[S26]). Compliance burdens grow with multi-jurisdictional regulations covering FCPA/anti-bribery statutes alongside stringent data security frameworks deploying significant compliance expenditures ([S7],[S21]). Failure to adapt rapidly to AI-driven industry shifts may erode competitive positioning as rivals leverage automation more effectively ([S18],[S26]).

Internal control issues highlighted by identified material weaknesses necessitate ongoing remediation efforts critical for sustained reporting reliability affecting investor confidence ([S1],[S27]).

What to Watch: Key Milestones and Metrics for Future Performance

Upcoming milestones include Q2 2026 closure of international firm acquisitions that will materially influence revenue mix alongside integration success metrics ([N1],[S19]). Observers should monitor sustained client retention rates currently near 70% over three years indicating sticky revenue streams underpinned by trusted relationships ([S6],[S23]).

Progress on internal controls remediation measured through auditor assessments will signal improved governance controls essential for operational stability ([F1],[S27]). Adoption curves of proprietary AI tools across service lines exemplify innovation capability that could unlock productivity gains or alternatively reveal execution risks amid digital transformation efforts.

Analysts should also track margin trends relative to competitive pricing pressures within tax advisory markets alongside headcount expansion reflecting talent acquisition success amid a tight labor market.

This analysis synthesizes publicly filed financial documents alongside recent news articles without offering investment advice or forecasts beyond disclosed company guidance where explicitly stated. Readers should consider inherent uncertainties including those referenced herein before making interpretations or decisions regarding Andersen Group Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments