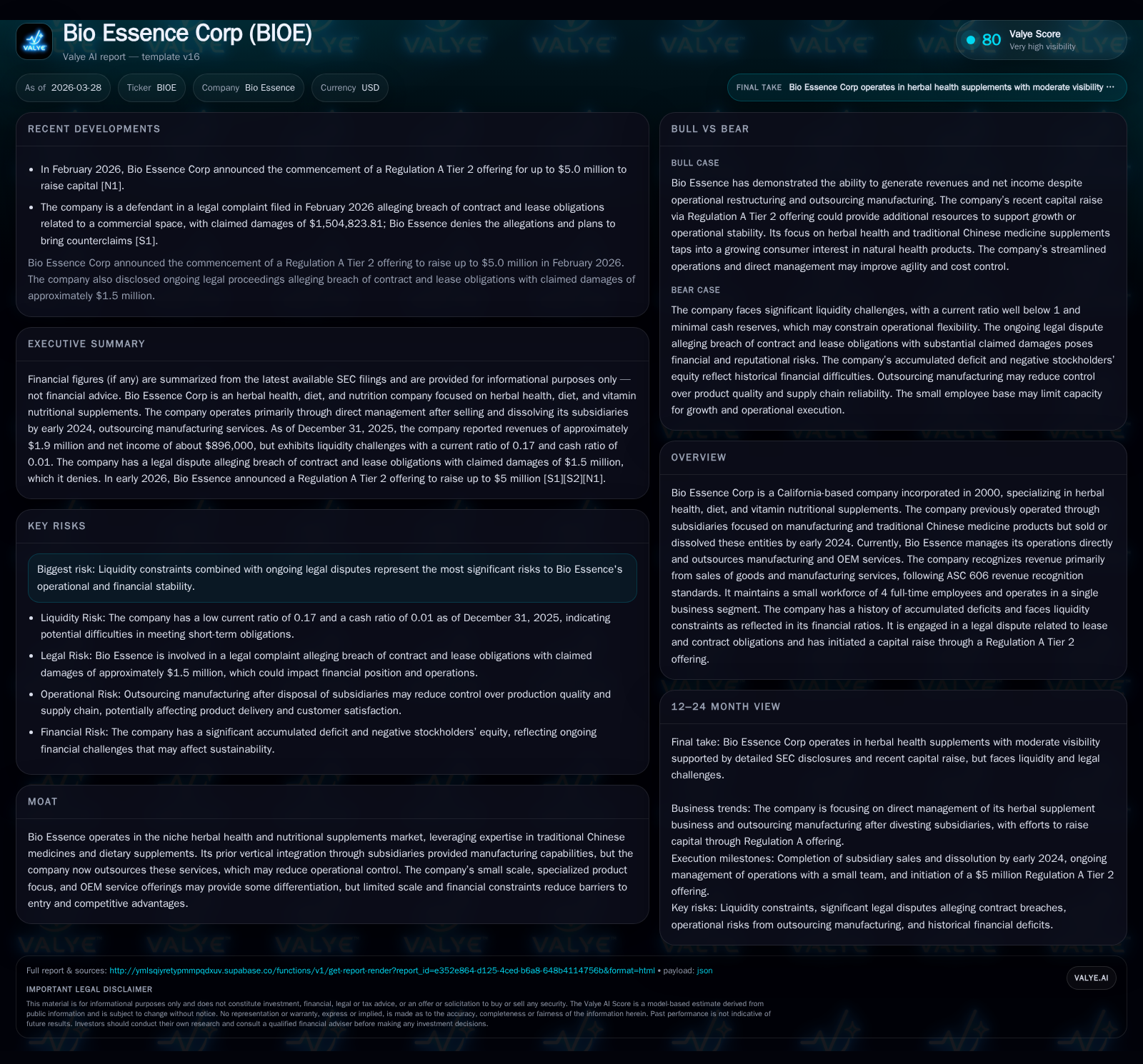

Bio Essence Corp's Revenue Surge and Operational Overhaul Amid Legal and Liquidity Challenges

Significant revenue growth in 2025 contrasts with ongoing financial strains and legal disputes, marking a pivotal transformation for Bio Essence.

Bio Essence Corp, a California-based herbal health supplement company, reversed years of losses in 2025, posting a nearly fivefold revenue increase to $1.9 million alongside a return to operating profitability. This recovery follows the divestiture of its subsidiaries and transition to an outsourced manufacturing model, reducing operational complexity but raising questions about scale and control. Despite this top-line growth, substantial liquidity constraints persist with a current ratio significantly below one, compounded by a $1.5 million legal claim linked to lease and contract breaches. The company’s ability to sustain growth amidst financial pressures and ongoing litigation will be critical to watch.

Company Overview and Historical Context

Founded in 2000 in California, Bio Essence Corp has established itself in the herbal health, diet, and vitamin nutritional supplements market. Following a change of control in 2016 by Jian Yang, the company expanded via subsidiaries focused on manufacturing (Bio Essence Pharmaceutical Inc.) and traditional Chinese medicine (Bio Essence Herbal Essentials Inc.). The dissolution of Fusion Naturals in late 2021 and the sale of BEP and BEH subsidiaries for $300,000 and $400,000 respectively marked a strategic pivot away from vertical integration [S1]. Currently, Bio Essence operates directly with four full-time employees overseeing sales while outsourcing manufacturing/OEM services.

Historical Financial Performance

Bio Essence’s revenues have fluctuated notably over recent years. After peaking near $986K in 2022, revenues declined sharply through 2023 ($551K) and bottomed out in 2024 ($324K), coinciding with the divestitures and restructuring [F1]. In contrast, FY2025 saw revenues surge to approximately $1.9 million — an increase of nearly +486% year-over-year [F1]. This upswing aligns with the shift to outsourced production following BEP's sale.

Operating income improved markedly from persistent losses (-$783K in 2022; -$459K in 2024) to a positive $900K in 2025 [F1]. Net income also turned positive at roughly $896K after multi-year deficits [F1]. Operating cash flow grew strongly from negative territory to about $1.57 million most recently [F1], while capital expenditures remained minimal post-divestiture [F1].

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1897566 | 896197 | 1569753 | 900011 | +485.8% | +168.5% |

| 2024 | 323940 | -1308796 | 623865 | -459438 | -41.3% | -34.7% |

| 2023 | 551506 | -971879 | -1025671 | -789050 | -44.1% | -20.0% |

| 2022 | 985757 | -809679 | -706824 | -782804 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -43.2 | |

| 2024 | 620251 | 44.1 |

| 2023 | -1029285 | 58.5 |

| 2022 | 25.0 |

Source: SEC companyfacts cache [F1].

Business Model and Segment Reporting

Bio Essence operates as a single reportable segment focusing on manufacture/OEM services and sales of health supplements rooted partly in traditional Chinese medicine [S13]. The company uses the ASC606 five-step revenue recognition framework recognizing revenues mostly at delivery net of discounts and returns [S4][S6][S9]. Post-2023 divestitures led to reliance on outsourced manufacturing partners rather than owned production facilities.

Customer concentration is significant; recent filings show two-to-four major customers accounting for up to around three-quarters of total sales volume [S16]. Vendor concentration is similarly high among manufacturers providing OEM services [S6].

Legal Challenges

In early 2026, Bio Essence faced a lawsuit from Stason Industrial Corporation alleging breaches related to lease payments and contract service failures. The complaint seeks damages near $1.5 million as of January 2026 [S1]. Bio Essence denies these allegations and plans counterclaims; however litigation risk adds pressure amid liquidity constraints.

Liquidity and Capital Structure

Despite improved profitability and cash flow generation in FY25, liquidity remains constrained. As of December 31, 2025, current liabilities ($2.44 million) substantially exceed current assets ($422k), resulting in a low current ratio near 0.17 [F1]. Significant components include operating lease liabilities exceeding $1 million plus large customer deposits classified as liabilities [F1][S11]. Shareholder loans remain elevated (~$885k), indicating reliance on internal financing sources.

Equity stood deeply negative at approximately -$2.07 million at FY25 end due to accumulated losses over prior years despite recent profits [F1]. There are no reported dividends or share buybacks given the need for capital preservation.

The company maintains conservative credit loss allowances with no bad debt reserves as of latest reporting dates [S7][S10], reflecting close monitoring despite customer concentration risks.

Outlook Considerations

The transition toward outsourcing manufacturing reduces fixed capital needs but may limit operational control over quality and supply reliability—key factors for premium herbal supplement products. Future growth will depend on diversifying both OEM vendors and customer base while managing ongoing litigation risks effectively.

Capital raising efforts remain unreported publicly but could be necessary given working capital pressures . Monitoring quarterly financials for sustained margin improvements amid scaling challenges will be essential.

Returns & Capital Allocation Summary

Return on equity remains negative at roughly -43% due primarily to historical cumulative deficits overshadowing recent earnings improvements [F1]. Positive operating cash flow suggests potential for free cash flow generation given negligible capital expenditures post-divestiture.

No evidence indicates shareholder distributions or repurchase activity as the company prioritizes liquidity management amid restructuring phases.

This analysis is based exclusively on SEC filings through early 2026 without speculative projections or forward-looking statements. Bio Essence’s strategic pivot marks a critical juncture balancing growth opportunities against operational risks within competitive nutraceutical markets.

Disclaimer: This report is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments