Air Industries Group Strives to Stem Losses Ahead of Strategic Merger

Examining AIRI’s recent financial decline, ongoing litigation, and transformative merger to assess its near-term trajectory.

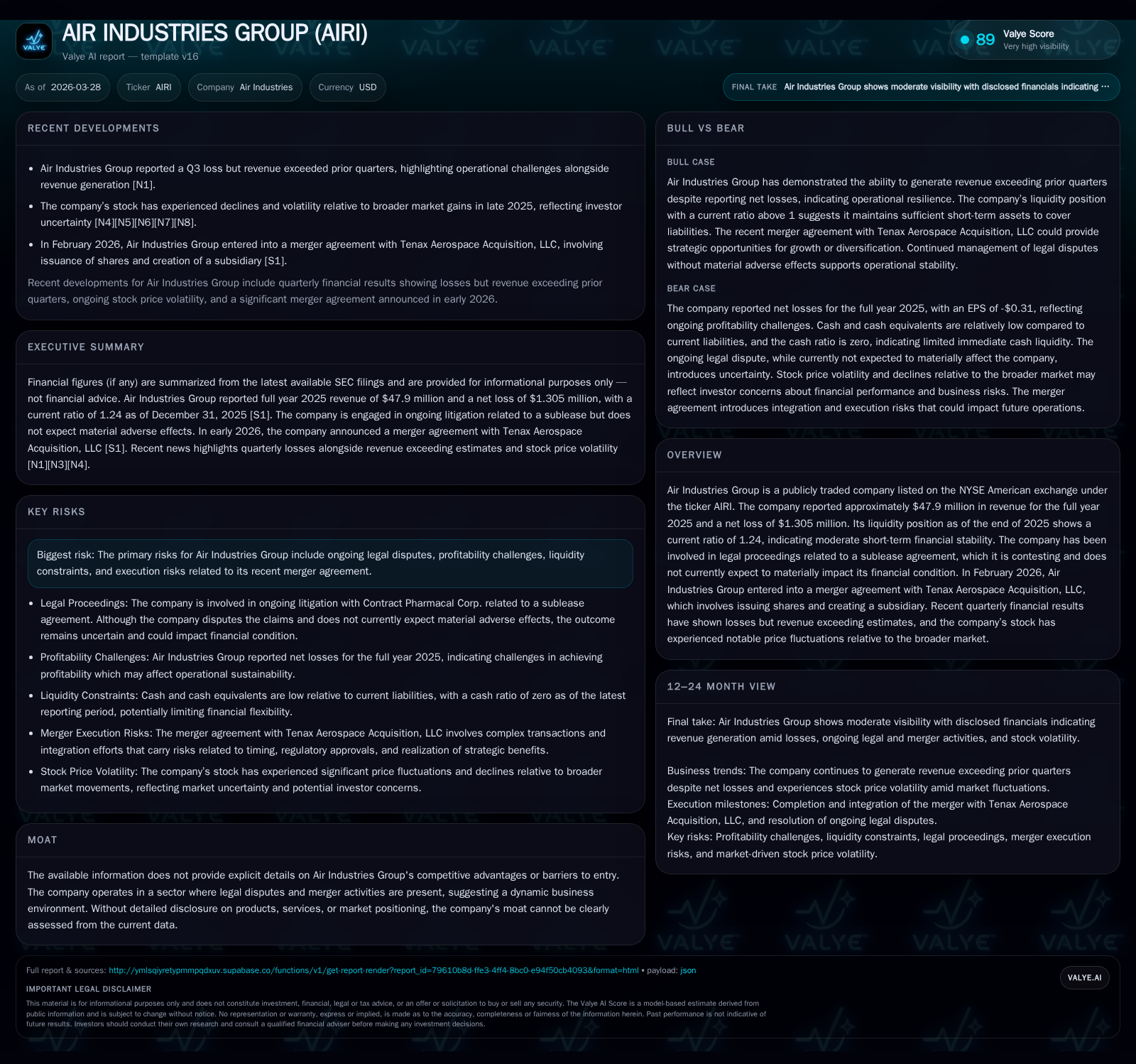

Air Industries Group reported a contraction in revenue with persistent net losses in 2025, alongside operating cash flow deterioration and increased capital expenditures signaling strained operational efficiency. Legal disputes over a sublease agreement continue but currently pose minimal material risk. The recently announced merger with Tenax Aerospace Acquisition involves a substantial share issuance reshaping the equity structure, presenting both strategic opportunities and execution risks. Monitoring merger closing conditions and operating performance inflection points will be critical for understanding AIRI’s potential turnaround.

Revenue Trajectory and Operating Dynamics: A Closer Look

Air Industries Group's top-line experienced a noticeable downturn in fiscal year 2025, posting $47.92 million in revenue compared to $55.11 million in the prior year—a decline of approximately 13% [F1]. Operating income mirrored this downward momentum, plunging from a narrow positive margin of $459,000 in 2024 to a slight operating loss of $338,000 in 2025—a steep YoY deterioration of roughly -174% [F1]. This swing highlights tightening operational margins amidst declining sales.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 48 | -1 | -1 | -338000 | -13.0% | +4.5% |

| 2024 | 55 | -1 | 0 | 459000 | +7.0% | +35.9% |

| 2023 | 52 | -2 | 5 | -295000 | -3.2% | -98.0% |

| 2022 | 53 | -1 | 0 | -194000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -6.8 |

| 2024 | -2 | -9.1 |

| 2023 | 3 | -14.0 |

| 2022 | -2 | -6.4 |

Source: SEC companyfacts cache [F1].

The oscillation between modest operating profits and losses over the past four years underscores structural pressures on AIRI’s business model or market environment. Though exact segment contributions are undisclosed, such volatility suggests challenges in cost control or product/service mix adaptation within their aerospace-related operations [S4].

Profitability Pressures and Cash Flow Trends Over Recent Years

Despite progressive narrowing of net losses from -$2.13 million in FY2023 to -$1.31 million in FY2025 [F1], profitability remains elusive for AIRI. The company recorded an approximate return on equity (ROE) of -6.8% for FY2025 given net income relative to $19.2 million equity base [F1].

Operating cash flow deteriorated substantially last year, shifting from positive $324,000 in FY2024 to negative $1.35 million in FY2025, reflecting operational stress and potentially working capital inefficiencies [F1]. Capital expenditures rose significantly by about 44%, reaching $3.32 million—suggesting ongoing investments perhaps aimed at modernization or capacity enhancement that have compressed free cash flow to an estimated -$4.67 million [F1]. This capex increase amid falling revenues reflects the tension between investing for growth and managing liquidity.

Legal Proceedings: Impact and Company Response

Beginning October 2018, AIRI has been engaged in litigation initiated by Contract Pharmacal Corp concerning a disputed sublease agreement related to former WMI subsidiary premises [S1][S5][S6][S7]. The plaintiff sought damages exceeding $1 million alleging delayed premises availability; however, the absence of a defined commencement date weakened their claim.

The courts denied multiple motions filed by Contract Pharmacal including attempts for summary judgment and complaint amendments, favoring AIRI’s position [S7]. The appellate process thus far has upheld these lower court rulings. Despite pending motions for reargument filed by Contract Pharmacal, management maintains confidence that these proceedings will not result in material adverse effects on financial condition or operations [S5][S6]. This suggests effective legal risk mitigation though the dispute remains unresolved.

Merger with Tenax Aerospace Acquisition: Strategic Rationale and Risks

In February 2026, AIRI entered into an Agreement and Plan of Merger with Tenax Aerospace Acquisition LLC whereby a wholly owned subsidiary will merge into Tenax—the latter becoming an AIRI subsidiary post-transaction [S25][S9][S10][S21]. Under terms described, AIRI will issue approximately 94.4 million new common shares as Merger Consideration to Tenax members representing roughly 95% ownership post-close versus incumbent shareholders’ residual ~5% [S9][S21].

The transaction includes standard termination rights protecting both parties against breaches, failure to obtain regulatory approvals—including Hart-Scott-Rodino clearance—stockholder voting failures on charter amendments (notably increasing authorized shares tenfold from 20m to 200m), or mutual consent withdrawal [S9][S25].

Shareholder approval is pivotal alongside regulatory scrutiny which could delay or derail closing beyond the September 30, 2026 deadline [S9][S23]. Additionally, provisions such as redemption rights at premiums and tender offers illustrate mechanisms designed to manage post-merger valuation uncertainties [S21][S22].

Capital Allocation Policy: Equity Structure and Liquidity

Recent filings display active capital structure rebalancing centered around accommodating the merger-induced share issuance [S9][S10][S12]. The pro forma increase in authorized shares signals flexible equity capacity but also implies dilution-related investor considerations.

AIR’s equity grew from approximately $15 million in FY2023 to $19.2 million by end-2025 despite ongoing losses indicating retained deficit absorption alongside paid-in capital growth [F1]. Liquidity metrics like the current ratio stood at a moderate 1.24 at year-end 2025 reflecting manageable short-term liability coverage yet signaling limited cushion against unforeseen stresses [F1].

No recent dividends have been declared since mid-decade; instead emphasis appears on conserving cash for strategic investments including the merger completion and capex commitments seen last year [F1].

Forward Outlook: Milestones and Execution Risks

Critical near-term milestones include obtaining regulatory reviews under antitrust laws, securing stockholder approval for charter amendments and share issuance mandates before the September 30, 2026 closing window expires [S8][S9]. Failure risks are mitigated contractually but present execution hurdles.

Monitoring operating income trends post-merger integration and free cash flow recovery will provide insight into whether strategic benefits materialize amid historically challenged profitability trends. Leadership changes adding Scott Glassman as Acting CEO in March may signal renewed strategic focus coinciding with demanding merger closure deadlines heightening governance pressure points [S3].

Execution risks also encompass continuing uncertainty from protracted sublease litigation although current outcomes favor AIRI's defenses minimizing material disruption [S5][S7], as well as complexities inherent in merging distinct aerospace entities including operational integration difficulties and customer retention risks [S8].

Overall, AIRI stands at an inflection point where legacy operational pressures must be overcome concurrently with significant corporate restructuring tied to the Tenax Aerospace Acquisition deal—a balance likely defining near- to medium-term viability.

This analysis is based solely on company filings and publicly available information as of March 28, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments